Alphabet’s Q2 Review: Search Is Still King

And Google Cloud likely clawed back market share in Q2

At The Pragmatic Optimist, we help hundreds of investors navigate the evolving AI innovation landscape, identify rock-solid businesses with strong growth trajectories and operational grit, and make long-term investments in the space with proven alpha generating returns.

Become a paid subscriber today

«The 2-minute version»

Google just demolished its Q2 earnings (in a good way, I mean), where it not only busted the “AI Kills Search” narrative but also clocked in a sequential acceleration in Google Cloud from a record number of $250-1B deals.

The way we see it, investors continue to underestimate the monetization opportunity with AI Overviews, especially given Google’s ad ecosystem infrastructure.

Meanwhile, Google Cloud is not backing away from the cloud wars, with expanding operating leverage, as it sees a record number of enterprises building with Gemini and Gemini-powered agents.

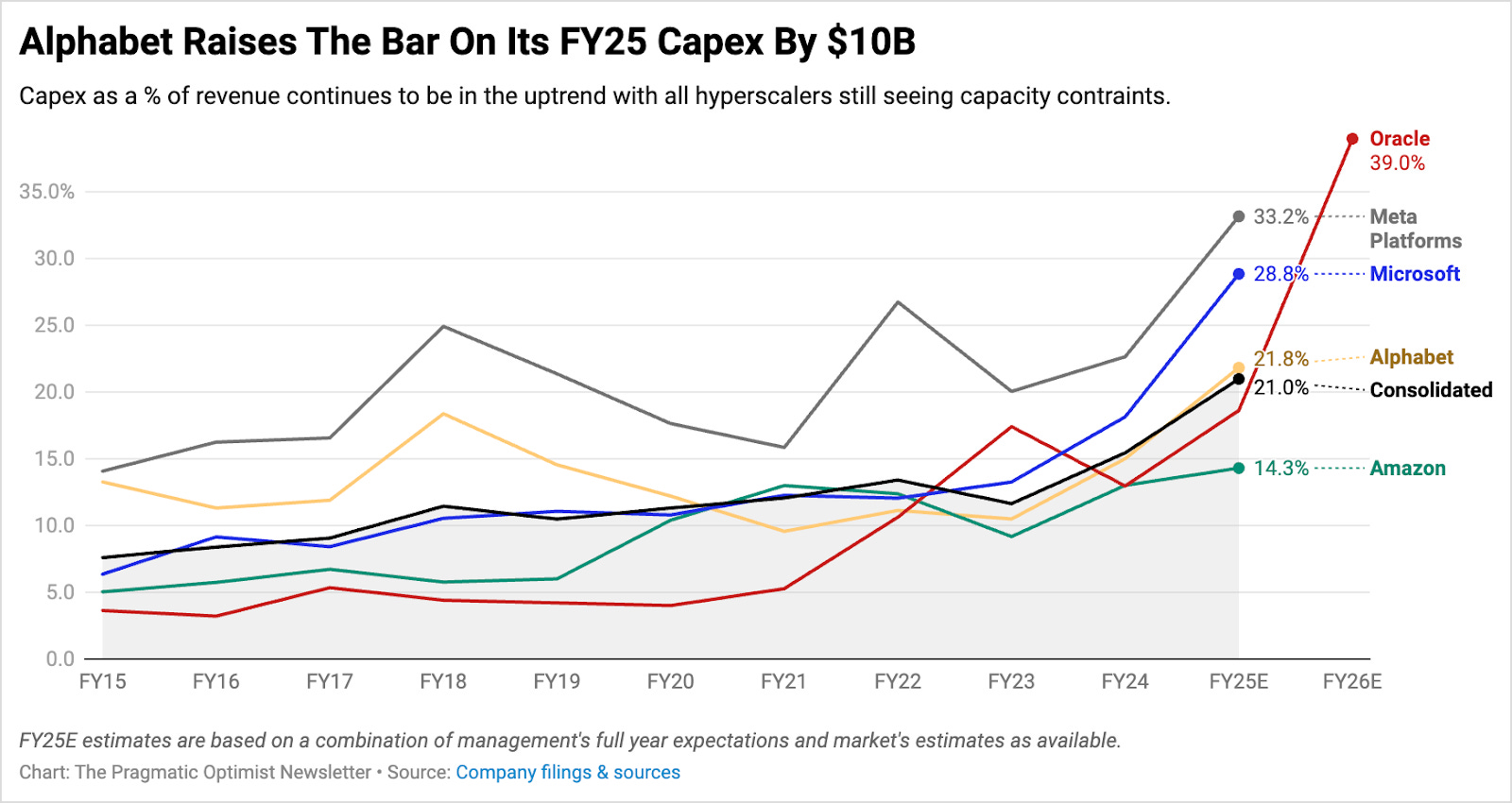

In all of this, capacity remains constrained. In order to ensure that it doesn’t fall behind on the AI arms race, Alphabet just raised its capex projections to $85B, up from its previous guidance of $75B.

However, the additional $10B on the capex bill comes with depreciation expenses that are expected to further accelerate in Q3.

👉With free cash flow taking a beating as a result and revenue yet to catch up with capex, don’t forget to check out our updated price target on the stock, which can be found on the AI Stock Tracker.

Note, at the beginning of the year, we had picked Microsoft as the best-positioned hyperscaler. While that has been a correct call so far, are we going to see a change in leadership in H2? We will find out next week when all the remaining hyperscalers report.

So, stay tuned for updated price targets on the AI Stock Rec Tracker and our conviction ratings on the Scoring Model that we will launch next week.

🎥Let’s Set The Stage

At the start of the year, when we had published our first hyperscaler research for FY25, we had identified that Microsoft MSFT 0.00%↑ was likely the best positioned among all to drive alpha during the year.

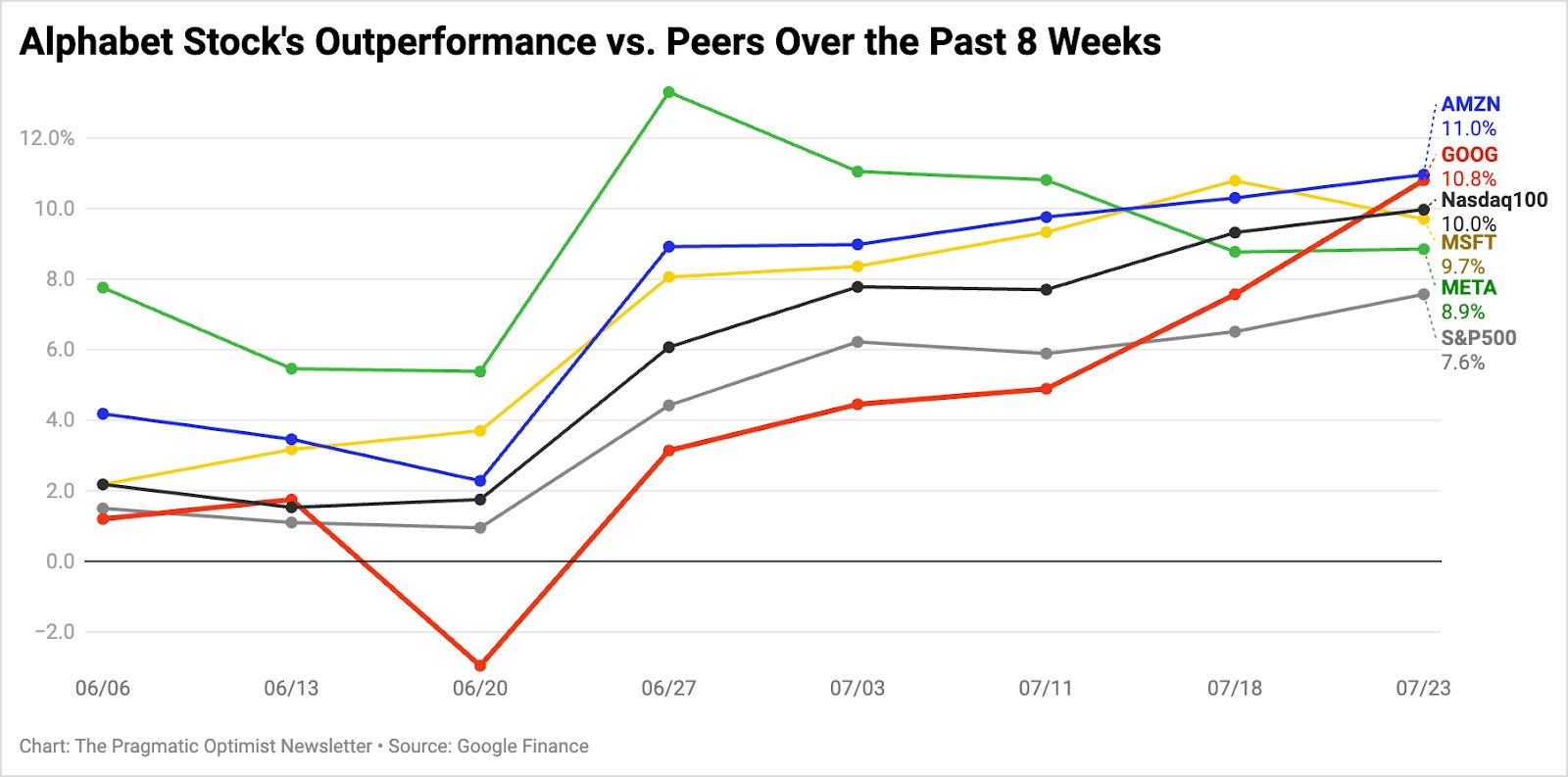

Last quarter, when we updated our research in May, Microsoft was indeed the best-performing hyperscaler at the time, outperforming the S&P 500 as well as its hyperscaler peers, namely Amazon AMZN 0.00%↑, Alphabet GOOG 0.00%↑ and Meta META 0.00%↑.

While we remained bullish on Microsoft, we also informed our investors in the May post that we had initiated a large position in Alphabet, as we believed that it was just too cheap to ignore.

At the time, Alphabet was deeply caught in the “AI-Kills-Search” narrative, and investors continued to ignore its infrastructure side, where the company has been positioning itself as the indispensable layer that developers, enterprises, and agents will all build upon.

Guess what? Since June this year, Alphabet started outperforming the hyperscaler complex. 🚀

Yesterday, the company kicked off the Q2 earnings season for hyperscalers, with the remaining three slated to report next week. In case you are not caught up with the headlines yet, Alphabet just demolished its Q2 earnings.

In a very good way, I mean.

Revenues and earnings came in ahead of expectations. Search, which was the most IMPORTANT metric and had the most BEARISH narrative associated, accelerated sequentially. Not only that, Google Cloud also crushed estimates, accelerating from the previous quarter at 32% YoY growth. Amid booming customer demand, which is evident by token usage already doubling since their I/O conference in May, management raised their capex guidance to $85B.

In all of this, one thing is clear.

That is, Sundar Pichai, CEO of Alphabet, is not backing away from the AI arms race.

With what we claimed was a “standout quarter”, we are in fact watching the rearchitecture of the internet, as Alphabet quietly embeds itself into the decision layer of modern life and enterprise workflows.

So, with that said, let’s dive into the earnings report by busting the “AI-Kills-Search” myth that has been prolonging in the markets for far too long.

Busting Alphabet’s “AI Kills Search” Headwind

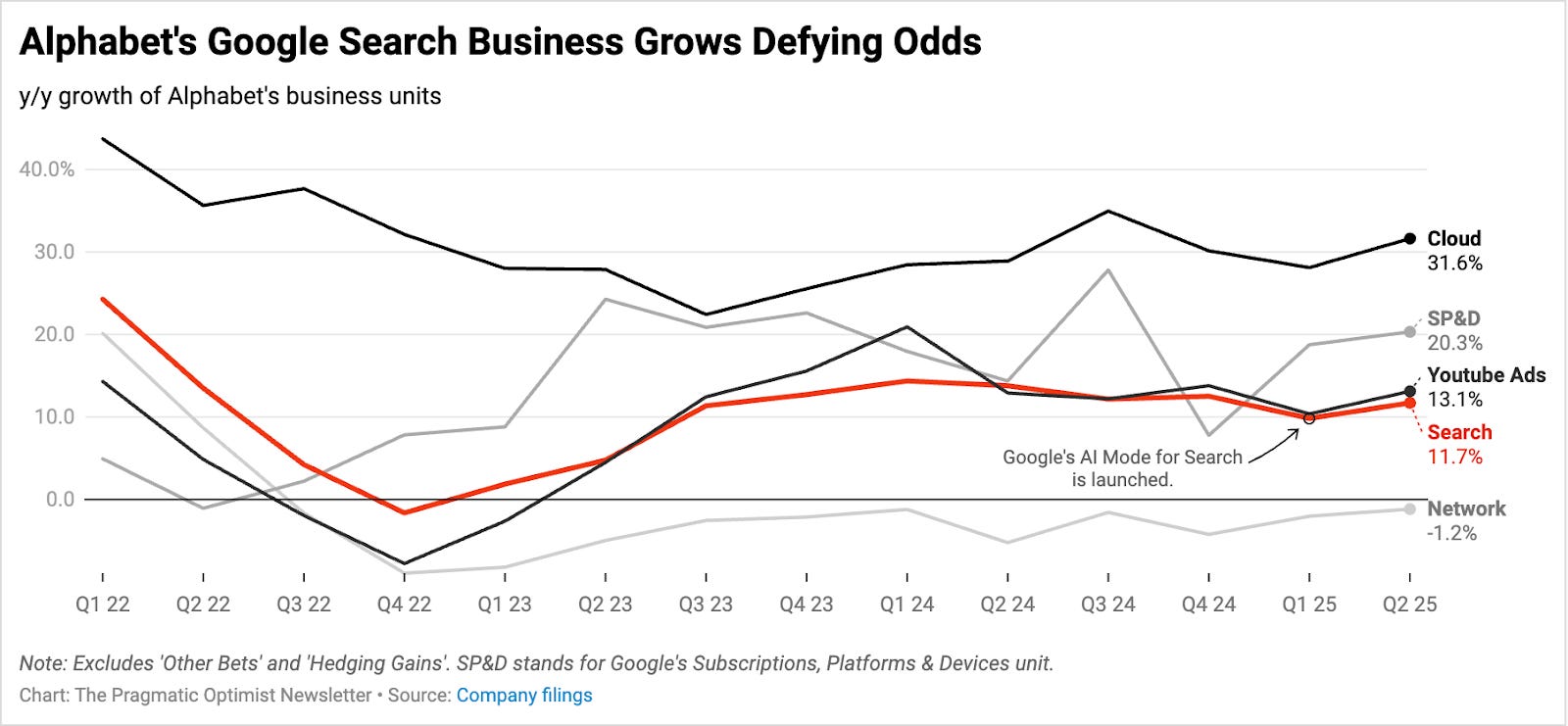

To those who feared that AI was going to kill Search, does this look like a dying business to you?

That’s right, Google Search revenue accelerated sequentially, growing 11.7% YoY vs. 8% expected.

That’s an upside surprise of roughly 370 basis points.

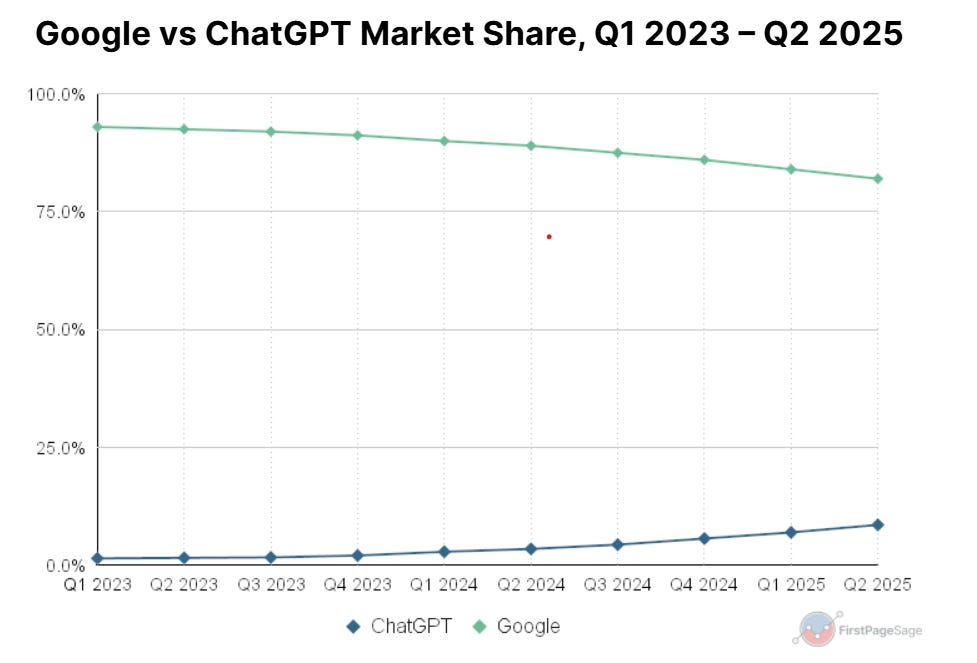

But let’s understand why investors were pessimistic in the first place about Google losing its search dominance to ChatGPT and other LLM players.

First, OpenAI’s ChatGPT has indeed been taking market share from Google Search, as can be seen in the graph below, especially as it surpasses over half a billion monthly active users, as Sam Altman described in this clip.

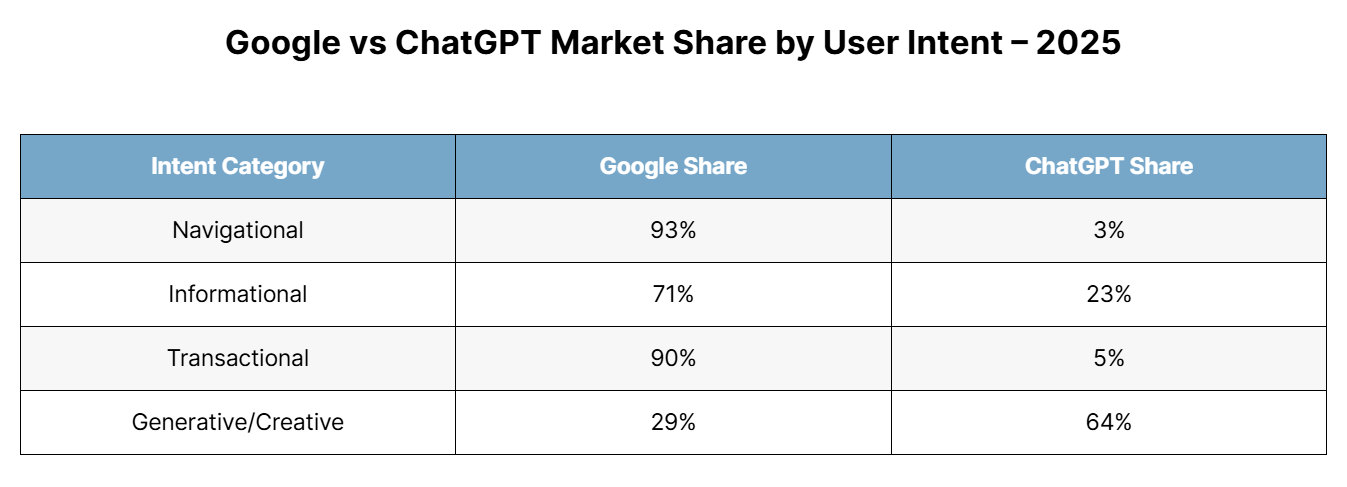

However, in the table below, you can see digital queries classified into four primary intent categories, showing how Google Search and ChatGPT are utilized differently.

The thing is that Google Search leads in transactional intent & the commercial viability from those search transactions are far more valuable to businesses compared to OpenAI’s ChatGPT, which dominates in generative/creative queries such as ideation, storytelling, and academic drafting.

During the quarter, Google’s AI Overviews (powered by Gemini 2.5) surpassed over 2B monthly actives, driving 10% more queries and delivering the fastest AI responses in the industry. At the same time, their end-to-end AI search experience, AI Mode, boasted over 100M monthly actives. Google’s AI Mode was launched four months ago and compares to the deep research tools by Perplexity & ChatGPT.

What is also important to note is that paid clicks accelerated sequentially to 4% (up from 2% in the previous quarter), while the price per ad continues to go up, particularly in developed markets. This has not only translated to Advertising Revenue accelerating as a whole to 10.4% YoY(including Search, YouTube, and Google Network) but, also expanded operating margin by 40 basis points year-over-year to 46.3%.

The way I see it, OpenAI's launch in 2022 has forced a cultural reset at Google, pushing the company to move faster, especially with AI Overviews, as user behavior shifts towards conversational AI. And the search giant is adapting well to competitive (& regulatory) headwinds.

You see, features like AI Overviews is designed to keep users engaged within the search ecosystem by encouraging follow-up queries, which could materially increase query volume. Plus, the future of query growth is likely to come not just from new users or new types of queries, but from deeper engagement per session through AI-driven interactions.

That is where I believe that the monetization opportunity in AI Overviews is huge, particularly as AI enables more detailed, context-rich queries and follow-ups, thus driving better targeting and dynamic creative generation. To that, Google can leverage its massive advertiser base, its vast ecosystem of first-party data (Gmail, Search, YouTube, etc.), creative assets, and automation tools to tailor ads in real time to match user intent, which could create a powerful monetization engine in the next 1-2 years.

In other words, we are looking into a future (very close by) where ads feel like useful recommendations rather than distractions.

Sure, OpenAI could technically develop an ad business to compete over time, but the real challenge lies in building a high-performing, scalable ad ecosystem, where Google’s competitive edge lies in its entrenched infrastructure.

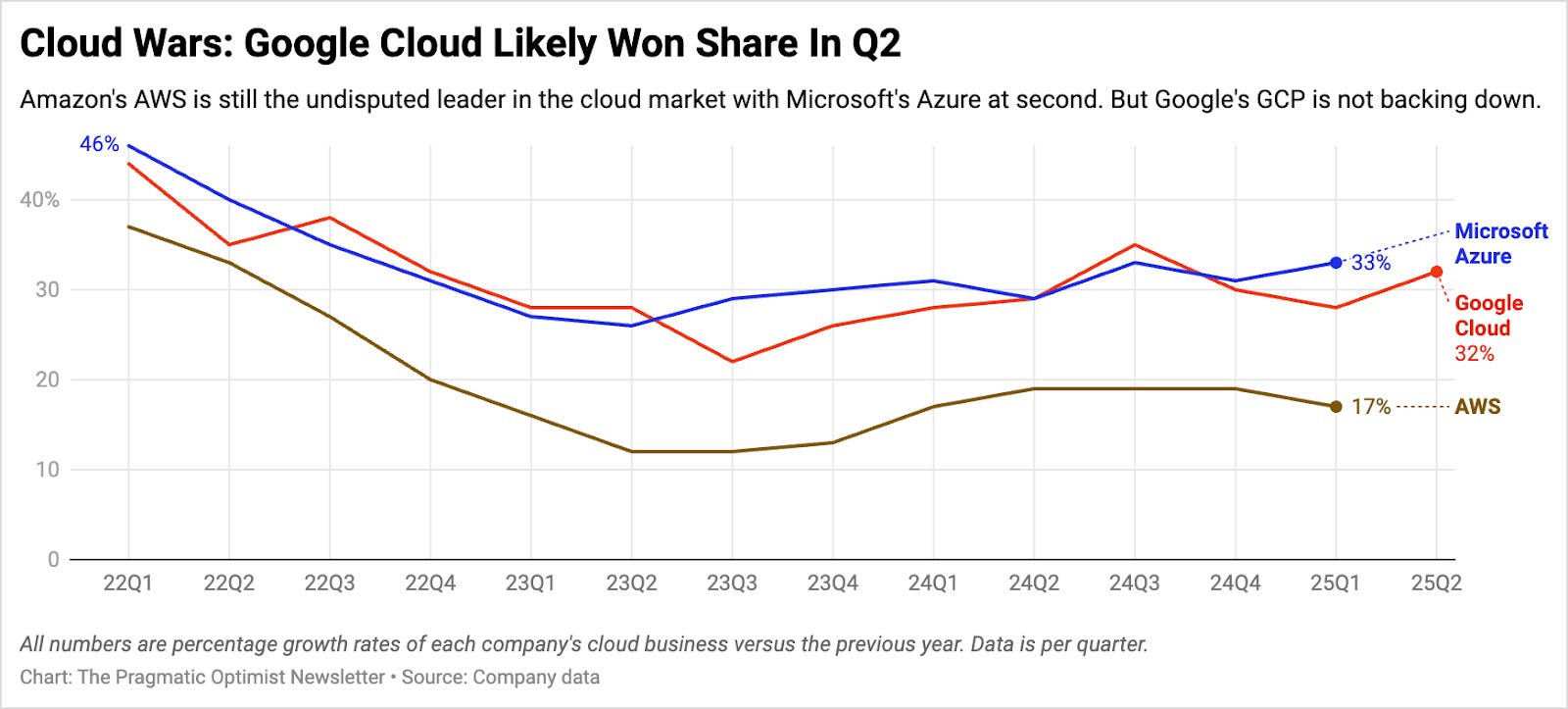

Google Cloud Likely Won Market Share in Q2

Meanwhile, Google Cloud saw its revenues accelerate sequentially to 32% YoY to $13.6B, compared to estimates of $13.14B.

To note, last quarter, Microsoft led the pack by growing their Azure revenues at the fastest rate of 35%, marking an acceleration in trend, while both Google Cloud and Amazon AWS (Amazon Web Services) saw their revenue growth rates decelerate to 28% and 17%, respectively.

When Microsoft reports next week, it is expected that Azure will continue to grow in the 34-35% range, while it is safe to assume that Amazon will likely report a 17-19% growth in AWS.

While Amazon AWS remains the leader in place, the Q2 growth numbers for Google Cloud demonstrate that it is not backing down, with the segment contributing over 14% to Total revenue in Q2, compared to 12% in the same quarter of the previous year.

During the quarter, the number of deals over $250M doubled year-over-year, with the number of new GCP customers growing 28% quarter-over-quarter, with more than 85,000 enterprises now building with Gemini and Gemini-powered agents to unlock productivity gains across business cases, translating to 35x growth in Gemini usage year-over-year.

Not to mention that OpenAI has signed a deal with Google Cloud to provide additional compute resources for its ChatGPT chatbot product, adding to OpenAI’s list of compute providers that includes Microsoft, Oracle ORCL 0.00%↑ and more.

What I am also bullish about is the expanding operating leverage, with operating margins expanding a whopping 940 basis points to 20.7% for the segment during the quarter.

While Amazon AWS commands the highest cloud operating margins of all hyperscalers, I strongly believe Google is demonstrating robust progress, especially as they continue to pursue efficiencies with custom TPUs to drive industry-leading performance and cost efficiency for both training and inference.

However, in order to address booming customer demand, management has decided to invest $10B more in capex than what it had previously guided for. Let’s understand what the implications of the additional capex mean for the overall business health.

The AI Arms Race Comes With an Extra $10B Added to Alphabet’s Capex Bill

In the previous quarter we had estimated the Big 4 hyperscaler capex at $322B, growing 48% YoY.

Well, the capex bill just got $10B steeper with the latest projections from Alphabet, where they raised their full-year capex target from $75 to $85B.

Assuming a forward revenue estimate of $388B for FY25, which represents a year-over-year growth of 11% (as per consensus estimates), the latest capex projections would amount to 22% of revenue, as opposed to 19.4% earlier.

However, like I have discussed in my previous hyperscaler deep dives, with higher capex investments comes a larger depreciation expense, which is basically an accounting practice that allows businesses to spread the cost of physical assets over a period of years.

In prior earnings calls, Sundar Pichai had repeatedly warned investors of margin headwinds from depreciation-related expenses in FY25.

This time, it is no different, with the operating margin being impacted by a significant increase of 35% YoY in depreciation expense to $5B, which was partially offset by strong revenue growth and continued efficiencies in their expense base.

Given the increase in capex investments, the management now expects depreciation to further accelerate in Q3.

Naturally, free cash flow is taking a beating as a result, where it is down some 70% YoY and 72% sequentially, as can be seen below.

However, the way I see it, it would be short-sighted for investors to turn bearish solely based on Q2’s free cash flow levels without context.

You see, the reason Alphabet is increasing its capex investments is as a result of the demand they are seeing from their customers as well as growth opportunities across the company that would require additional investment in servers and acceleration in the pace of data center construction.

When it comes to the consumer side of the business, we are seeing an acceleration in AI Overviews in Search, with Gemini now integrated into over 15 products with more than 500M users.

Meanwhile, the number of $1B deals that Alphabet has signed in Google Cloud so far in FY25 has already surpassed the number of billion-dollar deals that it did in the previous year.

With inference demand exploding, Alphabet is currently capacity constrained and is expected to remain in a tight demand-supply environment going into 2026.

Sure, its revenues are yet to catch up to the growth rate of its capex. With momentum in Google Cloud likely extending throughout the year, with Advertising revenues set for some strong tailwinds next year with midterm elections, I believe we will be at a cash flow inflection point in 2026, especially as capex growth moderates.

Here’s My Updated Alphabet Price Target and Portfolio Allocation.

Compared to all other hyperscalers, Alphabet’s stock continues to be priced at