Broadcom Spooked AI’s Euphoria

What Broadcom’s earnings say about AI Networking.

Friday’s sell-off is the exact moment we were waiting for after cautioning our investors over the past month. The AI trade that became overcrowded is finally unwinding, and we are ready to deploy our 30%+ cash that we diligently raised (through April and May) in The TPO Portfolio towards our highest conviction names in the coming weeks.

Join us! We help hundreds of investors navigate the rapidly evolving AI innovation landscape, identify rock-solid businesses with strong growth trajectories & operational grit, and deliver proven alpha-generating returns.

Since March, the TPO Portfolio delivered returns of 28% 💪, compared to 15% for QQQ and 25% for AIQ.

Become a paid subscriber today.

Let’s Set The Stage

Despite a stellar earnings report, Broadcom AVGO 0.00%↑ failed to fuel the rally further in its shares after management opted for prudent forward guidance. The sell-off in Broadcom’s shares proves once again that Wall Street’s favorite newfound pastime is punishing AI beneficiaries for failing to promise the moon.

Unfortunately, Broadcom’s disappointing Q2 results also coincided with a hot May jobs report, which sent yields soaring above 4.5%, shifting the attention back toward inflation and rate hikes. The double whammy from both those coinciding events on Friday resulted in investors realizing the AI trade was too crowded, that it was time to cut profits and run towards safe assets.

At The Pragmatic Optimist, we’ve been quietly waiting for the AI hype train to take a brief, scheduled pitstop. Over the last several weeks, we have been cautioning investors as the rally in the S&P 500 stretched further, led by a narrow participation from just a handful of AI companies.

In the meantime, we diligently raised cash through April and May in order to give us the emotional and financial oxygen to take advantage of the volatility we were anticipating, instead of being controlled by it. From about 15% of cash at the end of March, we raised it all the way to over 35% of our portfolio 💰💰 by the start of June.

This allowed The Pragmatic Optimist Portfolio to shield the Friday 06/05 volatility much better, even though most of our holdings are primarily in growth technology/AI.

📌Since March 1, The TPO Portfolio has delivered returns of 28% 💪, compared to 15% for QQQ QQQ 0.00%↑ and 25% for AIQ AIQ 0.00%↑.For the month of June so far, our portfolio is also faring much better than QQQ and AIQ as well.

You can track our entire portfolio and all our live trades in the AI Stock Tracker 2.0 tool using the link below. 👇

(Paid Members can access the AI Stock Tracker 2.0 directly from here)

In this post, we will explain our expanded views on Broadcom’s report while also highlighting other names in the AI Networking complex that include Celestica CLS 0.00%↑, Ciena CIEN 0.00%↑, Credo CRDO 0.00%↑ and Marvell MRVL 0.00%↑ and how we plan to deploy our capital forward in these names.

📅Please note that in the coming weeks, we will start to nibble in stages into our existing and potentially new highest-conviction names again at a reasonable price. We will send a separate post out on Tuesday with key technical levels we are watching across all our existing high-conviction names under coverage in the AI Stock Tracker 2.0.

Broadcom’s Achilles Heel in Q2

In a note to our subscribers on Friday, we highlighted 2 key issues that markets had with Broadcom’s Q2 ER.

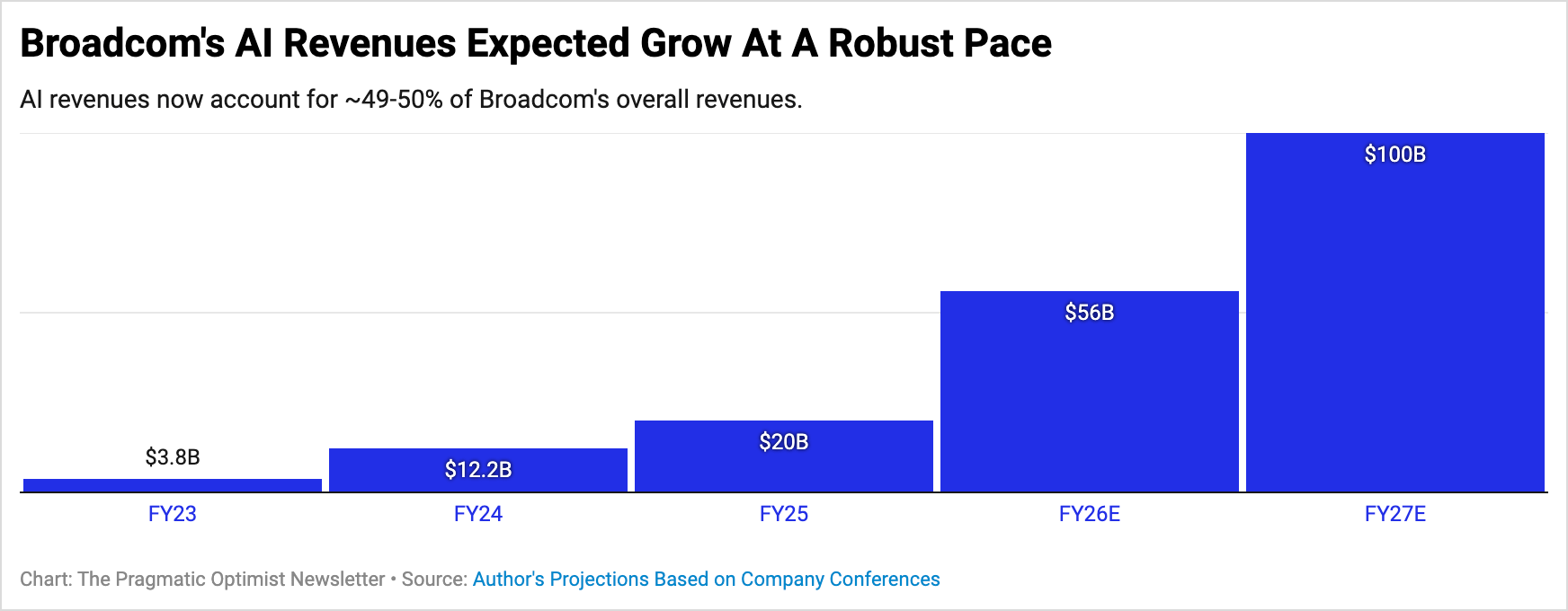

Sure, Broadcom’s top line has been growing rapidly. In fact, Q2 revenues were its fastest growth ever since November 2024, growing 48% to $22.2B. That’s also because AI revenues, sales of its XPU chips and AI networking products, jumped 143% to $10.8B, now accounting for 49% of Broadcom’s overall revenues, versus a ~33% revenue share last year. These numbers were very strong. So markets were naturally expecting Broadcom to revise their CY26 targets higher.

Except Broadcom’s Hock Tan merely reiterated $56B in FY26 AI revenue expectations, the same as the previous quarter, while charting FY27’s AI revenues to $100B. The problem is that markets dislike a mere reiteration of targets when Q2 growth was undoubtedly strong. Plus, a 64% stock surge over two months heightened Q2 expectations, only to be left disappointed by a mere reiteration of targets. So investors took profits after Q2’s report.

But a 20% post-earnings correction in Broadcom’s shares also reflects that some more near-term issues are at play here. Upon closer inspection, Broadcom’s guidance failed on a very important metric that markets hold dearly in 2026. Here’s why we think the stock will remain pressured in the near term and where we believe price levels will likely bottom out.