Part 1: Dollar General's fundamentals are weakening. Can it recover?

The rise and fall of Dollar General as a defensive play as its revenues slow, income declines and interest expenses rise in a tough macroeconomic, competitive and geopolitical environment

At a Glance

Dollar General has been dethroned from its “defensive” play status. Dollar General, which has outperformed the S&P 500 since its IPO, is now down -58% YTD.

In this post, I dove into the Q2 Earnings report to uncover the truths that is plaguing the Dollar General stock.

Turns out that investors’ flight away from the stock is completely warranted. Dollar General’s revenue growth is slowing. At the same time, its operating and net income are declining on a year-on-year basis. Furthermore, Dollar General’s management has severely slashed its financial outlook for FY 2023.

The biggest concern for Dollar General is that its interest expense is growing, as the company takes on additional debt in today’s high interest rate environment to fund its dividend payouts.

While there are many structural storm clouds hanging over Dollar General today, the company can still reverse the course of its fate, if it enforces stricter balance sheet discipline over the coming fiscal years.

So, is Dollar General a severely undervalued stock? Or is it a value trap? Read below to find out.

Let’s set the stage!!!

Dollar General DG 0.00%↑ reported its earnings on August 31, 2023. Dollar General, which historically outperformed the S&P 500 (since its IPO), is now down -58% YTD.

Last week, I wrote that investment portfolios that contain a higher allocation of its funds to defensive sectors tend to outperform the index (S&P 500) and shield themselves against market volatility, during recessions. You would naturally think that Dollar General is a perfect example of a “defensive” business, where consumers shop for essential staples that they need, regardless of macroeconomic conditions.

Dollar General has indeed been a lifeline for lower-income shoppers, particularly in rural areas with few other retail options. The company says its “core customer” makes under $40,000 a year.

However, its latest earnings report showcased that Dollar General may no longer offer the defense. In fact, given weaker consumer demand, higher wages and rising import costs, investors are increasingly worried about the company’s valuation. At the same time, the company is increasing facing the brunt of inventory shrink from Organized Retail Crime, as we discussed last week. A combination of these factors are causing Dollar General’s business fundamentals to rapidly weaken and investors to loose confidence in the stock.

Given that Dollar General is down -58% YTD, does this make it a deeply undervalued stock? Or is this a value trap?

👉🏽👉🏽👉🏽Plan for the Post

In Part 1 (today), I will dive into the Q2 earnings report to uncover the truths that are plaguing Dollar General. I will then use a Reverse Discounted Cashflow Model to determine the implied growth rate of future cashflows that are priced in Dollar General’s stock today.

In Part 2 (next week), I will present an optimistic, a pessimistic and a neutral thesis for Dollar General based on my assessment of its future business fundamentals that are driven by industry trends and the macroeconomic environment.

Let’s uncover the secrets from Dollar General’s Q2 Earnings report

The 3 key reports that I look for in a company’s earnings reports are 1) The Income Statement, 2) The Cashflow Statement and the 3) The Balance Sheet. In this section, we will focus on uncovering the truths hidden behind the Income Statement and the Cashflow Statement from Dollar General’s Q2 earnings call.

✅ Dollar General’s Q2 Income Statement

I have highlighted the key metrics in the Income statement that we will be looking at.

1. Revenue

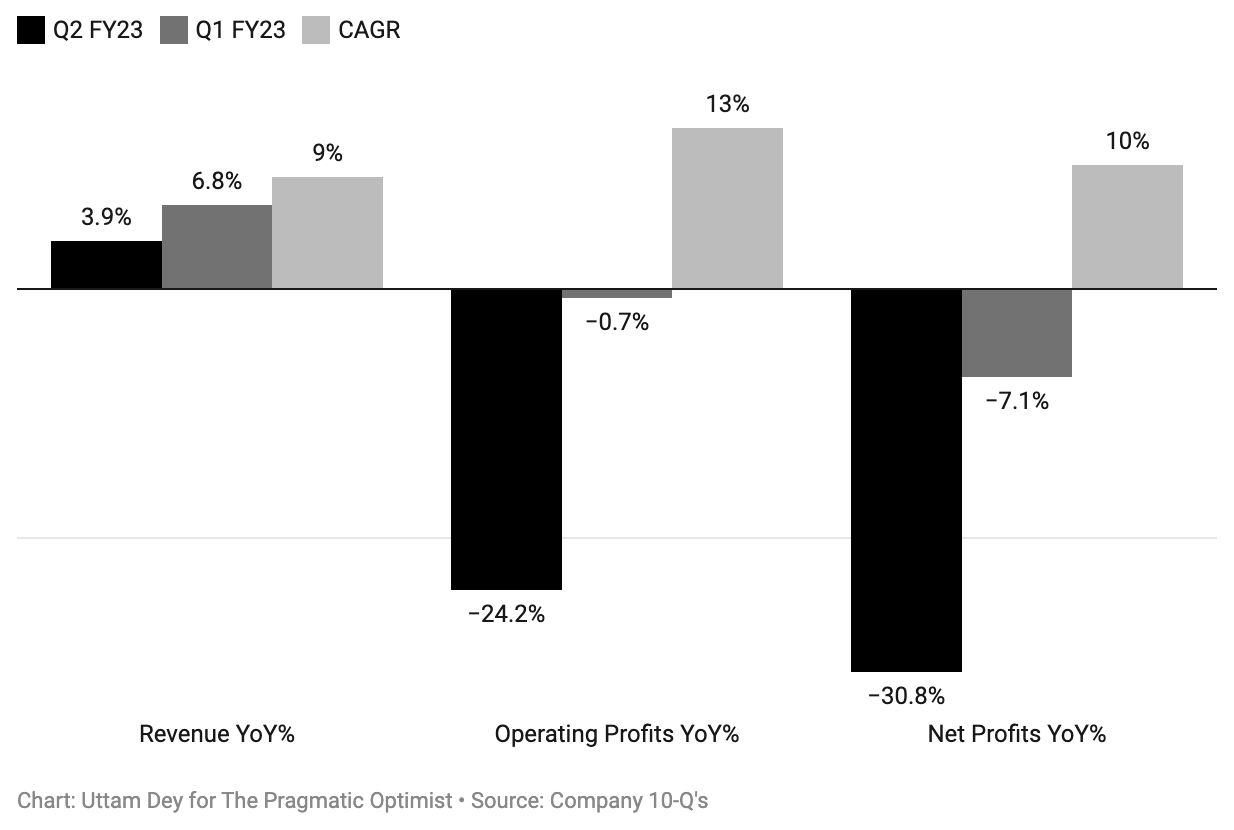

Dollar General’s Q2 revenue was $9.796B, a 3.93% increase YoY.

This compares to a revenue growth rate of 6.76% YoY in Q1.

Since its IPO in 2009, the company has grown its revenue at a CAGR of 9%

So, we can see that the company is most certainly experiencing a slowdown in demand from its historical levels.

The company further noted that same store sales decreased 0.1% during Q2.

2. Gross Margin

While Gross Profit stayed more or less flat YoY, Gross Margin fell 100 b.p YoY to 31%

3. Operating Profit & Margin

Dollar General’s Q2 Operating Income was $0.692B, a 24.21% decline YoY.

Since its IPO, Dollar General’s Operating Profit has grown at a CAGR of 13% (faster than revenue growth).

In Q2, its Operating Margin was 7%, compared with its historical average of 9.5%.

This is driven by rising SG&A (selling, general and administrative expenses) that has grown 10% YoY. Higher labor costs, rent and utilities contributed to rising operating expenses, that shrunk operating margins.

4. Interest Expense

Interest Expense on debt increased to $84.3M, which is nearly double of what it was YoY. So, their interest expense is growing massively, and that is significantly weighing down on net income.

5. Net Income

Dollar General’s Q2 net income was $0.469B, a 30.85% decline year-over-year.

Dollar General’s net income margin stands at 4.79% vs. 7.2% a year ago.

My Comment: This is a very weak report for Dollar General. While, revenue is still growing (albeit slowly from historical trends), we are seeing cost of goods sold and operating expenses grow faster, which is causing margins to shrink across the board. Furthermore, the doubling of interest expense is undoubtedly concerning. Dollar General highlighted during its earnings call that the increase in interest expenses is primarily due to higher outstanding borrowings and higher interest rates. I don’t personally like to see this, because if interest rates are higher, a business should be taking on less debt, or reducing its current level of debt outstanding, so that interest payments stay anchored and the business can increase its profitability henceforth.

✅ Cashflow Statement (6 months ending August 04,2023)

I have highlighted the key metrics in the cashflow statement that we will be looking at.

1. Cashflow from Operating Activities

Net Income: This is the same Net Income that is present in the Income statement, and we can see that the Net Income (for 6 months ending August 04, 2023) is down -30% to $983M

Merchandise inventory: Merchandise inventory is down -46% YoY. In other words, Dollar General is seeing $711M less cash outflows from buying inventory. This is a net positive for overall cashflow from operating activities.

Accounts Payable: Accounts Payable is significantly down YoY by approximately $500M. This is weighing down on the overall cashflow from operating activities. Accounts payable is a record of all of the money that is owed to third parties such as vendors and suppliers. If accounts payable increase, it means that these funds have not left the company account and therefore indicates an increase in cash for the accounting team. If accounts payable has decreased, as is the case with Dollar General YTD, it means that that cash has actually been paid to vendors or suppliers and therefore the company has less cash.

Overall, the net cashflow from operating activities was equal to $726M, which is 23% lower YoY (in line with the decline in Operating Income).

2. Cashflow from investing activities

Capital Expenditure: Purchase of property and equipment (capital expenditures) was $768M YTD (which is 20% higher YoY).

Please note that the capital expenditures YTD is more than the cashflow from operating activities.

This means that Dollar General is Free Cashflow negative YTD.

Also, Dollar General pays a dividend to its shareholders. Therefore, if Dollar General is Free Cashflow Negative, it begs the question of how it is paying a dividend to its shareholders? Cashflow from financing activities will be able to answer the question.

3. Cashflow from financing activities

Issuance of long-term obligations: We can see that Dollar General has issued $1.5B in debt YTD.

Net increase (decrease) in commercial paper outstanding: Then they used $1.2B of that debt, to repay other outstanding debt.

Payments of cash dividends: We can then see that the payments of dividends was approximately $260M YTD, so the company is issuing debt to pay its dividends to its shareholders.

My Comment: In Dollar General’s income statement, we saw that interest expenses had nearly doubled YoY to $84M. This is happening partly because the company has taken on more debt ($1.5B) and partly from higher interest rates. Ideally, a financially healthy company should be able to pay its dividends organically with organic cashflows. But since Dollar General has turned Free Cashflow Negative this year, it can either cancel its dividend payouts until a later date, or it would need to borrow money to pay its dividends.

✅ Dollar General’s Financial Outlook for FY 2023

Revenue Guidance: Dollar General expects FY 2023 Revenue growth to be in the range of 1.3%-3.3% ($38-$40B). This is lowered from its previous guidance of revenue growth estimates of 3.5%-5.0%.

Diluted Earnings per share: Dollar General now expects Diluted earnings per share in the range of $7.10-$8.30, which is a decline of 34-22% YoY. Their previous guidance expected the diluted EPS to decline 8%. This means, we can expect operating income to decline in the same range. Furthermore, Dollar General stated that diluted EPS guidance include an anticipated negative impact of approximately 4% points due to higher interest expense in 2023.

These are huge negative revisions to the revenue and profit outlooks for Dollar General in 2023. Prior to the earnings report, the stock was trading at approximately $155. With the updated revisions, where revenue is expected to grow 1.3%-3.3% (vs. 3.5%-5%) and EPS is expected to fall -34% to -22% (instead of -8%), it is quite natural, that the stock has taken a -36% plunge since Q2 earnings.

What is the future “implied” growth rate of Dollar General that is priced into the stock today?

A company’s stock price is a reflection of the investors’ expectation of the discounted present value of the future cashflows that the business would generate. In other words, if Company ABC’s stock is trading at $100, it is possible to determine the expected growth rate of future cashflows of Company ABC that are priced in the $100 of the stock price.

In this section, we will explore the Discounted Cashflow and the Reverse Discounted Cashflow Models.

📘📘📘A crash course on Discounted Cashflow Model: A discounted cashflow model is a method to estimate the “fair” value of a company’s stock, based on its future cashflows.

In a Discounted Cashflow Model, we need to know the current business metrics, such as Free Cashflow or Earnings (per share). We also need to build our assumptions of how the business metrics grow over the course of 5-10 years and our estimate of the discount rate. Once we have the business metrics and our assumptions in place, we will be able to input the respective values into the model. The result: We get a “fair” price value of the stock that it should be trading at today, given the assumptions that we have built.

📕📕📕A crash course on Reverse Discounted Cashflow Model: On the other hand, a Reverse Discounted Cashflow Model is used to estimate the “implied” growth rate of the stock (business) based on its current price. Simply put, in a Discounted Cashflow Model, you are solving for the stock price. In the Reverse Discounted Cashflow Model, we are entering the current stock price to solve for the future growth rate of the stock (company) that is priced in today.

In this section, I will use the format that Brian Feroldi has already laid out to perform a Reverse Discounted Cashflow Model. I will also use the Reverse Discounted Cashflow calculator that he has built to save me some time. Let’s dive right into it. 👇🏽👇🏽👇🏽

Step 1: Where is Dollar General in the business growth cycle?

(Note: Reverse Discounted Cashflow model won’t work for early stage and high growth companies, which are usually operating at a loss)

In Step 1, I put in the inputs for the general trend of Revenue, Gross Profit, Operating Profit, Net Profit and Share Count for Dollar General as follows:

Revenue: Growing slowly

Gross Profit: Declining

Operating Profit: Declining

Net Profit: Declining

Share Count: Declining

Based on the above inputs, Dollar General currently belongs in between Stage 4: Capital Return to Stage 5: Decline phase.

Step 2: What is Dollar General’s TTM (Trailing 12 Months) Free Cashflow?

Dollar General’s TTM FCF = $93.5M

Step 3: What should we take as Dollar General’s Terminal growth rate?

A Terminal growth rate is the growth rate of a company once it has fully matured and saturated its total addressable market. While, the concept is undeniably theoretical, a terminal growth rate can be thought of as the company’s eternal growth rate. Usually, the number is set to the value of long term US Real GDP, which is approximately 2.5-3%.

In the case of Dollar General, we will put a more conservative Terminal growth rate of 1.8-2%, which is equivalent to the Fed’s projection of long-term US Real GDP as per the latest FOMC meeting.

Step 4: What would be an appropriate discount rate for Dollar General?

The discount rate is the interest rate used to determine the present value of future cashflows in a discounted or reverse discounted cashflow (DCF) analysis. Or in other words, "discount rate” is the required rate of return that an investor demands for owning the asset.

For example, the required rate of return for holding a US 10 Y Treasury bond is 4.65% (as of October 2, 2023).

In a separate post, where I addressed the S&P 500 equity risk premium, I had discussed that the equity risk premium for S&P 500 was approximately 4.6% (September 2023). This would mean an investor would demand an additional 4.6% on top of the risk free rate to invest in the S&P 500. That would make the discount rate of the S&P 500 = 9.2%.

The idea is that safer investments have lower rate of return on investment vs. riskier investments. (Investing in the US 10 Y Treasury bond is safer than investing in the S&P 500).

In the case of Dollar General, we are going to take a discount rate of 8%.

The Final Step 5: What is the “implied” growth rate of Dollar General’s Free cashflow over the next 10 years, that is priced into Dollar General’s stock today?

🥁🥁🥁

Unfortunately, here, we run into a problem. Since, Dollar General’s Free Cashflow has turned negative YTD, the TTM Free Cashflow of $93.5M is abysmally small compared to previous years.

Given the current TTM FCF of $93.5M, and assuming a Terminal growth rate of 2% and a Discount rate of 8%, the Dollar General stock is currently pricing a 37.6% growth rate in Free Cashflow annually for the next 10 years.

We know that an expected 37% growth rate in Free Cashflow over the next 10 years is absurd Dollar General. In fact, it would be absurd even for a high growth tech company to maintain this level of free cashflow growth over the next 10 years. This is one of the instances, where a sudden drop in FCF won’t allow the Reverse Discounted Cashflow model to work properly.

As a result, we will go the arduous route of the Discounted Cashflow model, which would require us to build additional layers of assumptions to determine the fair value of Dollar General’s stock price. But before we get into that in Part 2, I want to take a moment to highlight some of the key risks that I see that Dollar General may be structurally facing. This will enable us to build a more robust set of assumptions for an optimistic, pessimistic and neutral discounted cashflow model for Dollar General.

The Structural storm clouds that Dollar General is up against

While Dollar General has historically outperformed the S&P 500 since its IPO and is currently trading at a Price to Earnings ratio of 10.5, there are structural shifts in the economy and the competitive landscape that may not bode well for Dollar General, unless it finds innovative solutions around it.

Risk 1: Valuation Pressures

In my opinion, the overall S&P 500 is not well-positioned to provide great forward returns. The US 10 Y Treasury yields 4.6% and T-bills yield well over 5%, which seriously hurts the relative value of equities.

While Dollar General is trading at a PE (Price to Earnings ratio) of 10.5, which is lower than S&P 500 PE of 19.6, the weak revenue and earnings outlook, along with growing interest expense in a higher rate environment, may continue to put downward pressure on the stock.

Risk 2: The changing world order

There are fundamental differences between the modern consumer economy today vs. the one that existed between 1980-2012. During 1980-2012, there was a significant increase in offshore factory and productivity expansion in China and India. At the same time, there was a massive gap in domestic wages between US and China (and other emerging nations, which played a significant part in offshoring). As a result, producer input prices would be stable and/or growing at a much slower pace than consumer prices, allowing businesses to expand margins.

Today the east-west gap is getting wider, as trade relations are weaker and transportation fuel costs are higher. As a result, retail companies, such as Dollar General, Target, Walmart and others may experience higher import costs. As import costs (which is part of producer input prices) go up faster than consumer prices, it will start to create gross margin pressures at these companies. And if you factor in higher wages from higher consumer prices, we will see pressures on operating margin as well.

Risk 3: Persistent inflation is killing consumer demand

There are structural forces at play today that suggest that inflation may be sticky for the long term. The west is battling with 3 main inflationary forces today. The first is the aging population, which results in lower labor-force participation rate. The second is de-globalization and the subsequent re-shoring of factories and manufacturing that needs to take place. The third is the shift to renewable energy, which has created a vacuum in the commodity markets (which was already underinvested to begin with). Unless we see a rapid increase in productivity, driven by technological forces and the US expanding its factory production, these inflationary forces will stick around.

As inflation remains sticky, so does the cost of borrowing. Today, the boost from the pandemic checks that resulted in elevated levels of person savings savings have mostly dried up. Consumers have turned towards credit cards to finance payments. Today, the credit card debt sits at $1.015T, and is growing at 10% on a YoY basis. In the meantime, average hourly earnings is growing at 4.3% and if you look at Real Average Hourly earnings, it has grown just 0.7% since 2019, when Real GDP has grown by 6.7-7%. No wonder, real retail sales is down -1.2% on a YoY basis.

Risk 4: Organized Retail Crime is a systemic issue

Last week, I had published a piece on how big a problem shoplifting or ORC (more broadly) possess for the US retailers. While the findings are mixed, with some retailers facing the brunt more strongly than others, Organized Retail Crime is undoubtedly a systemic issue in the US. If the government does not take targeted actions, the issue is likely to worsen in the coming years.

Risk 5: Competitive landscape makes Dollar General look like a premium store

Did you know that Dollar General DG 0.00%↑ and Dollar Tree DLTR 0.00%↑ have higher gross margins than Costco COST 0.00%↑ , BJ’s BJ 0.00%↑ , Walmart WMT 0.00%↑ and Target TGT 0.00%↑ ?

Since Costco, Walmart, Target have lower gross margins, it means they are the actual “discount stores”. This could explain why people’s behavior have shifted towards purchasing bulk items from Costco and Walmart, which turns out to be cheaper, compared to purchasing individual items from Dollar General. As a result, we are not seeing the business weakness in Costco and Walmart, that we are seeing in Dollar General.

Closing Thoughts

In today’s post, we dove into Dollar General’s Q2 Report to uncover the truths behind the stock’s severe underperformance. We now know (for a matter of fact), that the stock’s underperformance is indeed driven by slowing revenue growth, declining operating and net income and increasing interest expense as the company takes on additional debt in a high interest rate environment to pay dividends to its shareholders. Investors have rightfully lost confidence. Given how sharply Free Cashflow has fallen, it is not possible to determine the future “implied” growth rate of cashflows that are priced in the stock today. Furthermore, there are structural storm clouds that overshadow Dollar General’s future. It is however, completely possible that Dollar General finds innovative solution to overcome its weaknesses in the future.

In Part 2, I present an optimistic, a pessimistic and a neutral thesis for Dollar General and compute the “fair” value of the stock price using a Discounted Cashflow Model. This will allow us to fully understand the scope of Dollar Generals’ future business fundamentals based on industry and macroeconomic trends, which will then make us capable to determine if Dollar General is really an undervalued stock or a value trap.

Thanks for reading!!!

Amrita 👋🏽👋🏽

Analysis is on spot. Kudos. Personally speaking I lost money on this stock thinking it provide shelter but I now know DG mis-stepped on their inventory plans and wounded themselves in the foot. I do think if they start to refocus back onto their $40k consumer as you point out, it should be a good stock again. Thats months away.

I live out in the rural country between Porterville and Terra Bella (about 12 minutes from both). Dollar General is the only inexpensive store in the tiny town of Terra Bella. For a quick shopping trip I often choose to go there for my shopping rather then into larger Porterville. Dolllar General is the lifeline for most of the poor people who live there. It’s closure will significantly change their lives.