Dollar General: The bull and the bear case for the stock | Part 2

While Dollar General is dethroned from its "defensive"status, does the stock have sizable upside if the management is successful in delivering balance sheet discipline & improved business outlook?

At a Glance

Dollar General which has historically outperformed the S&P 500, is down -58% YTD. The reaction however, is fully warranted. As the business revenues slowed and operating income declined on a year-on-year basis, the company took on additional debt to finance its dividends paid out to shareholders. This has ballooned the company’s interest payments and put downward pressure on its net income.

Furthermore, the company slashed its revenue and income guidance for FY 2023 in its Q2 earnings call that rightfully scared away investors.

While Dollar General is undoubtedly under a lot of pressure today, it doesn’t necessarily mean that the future holds little to no upside. Or, does it?

In this week’s Tuesday Top Picks, I outline the bull and the bear case for Dollar General and its stock, given how the business evolves in the next 10 years and beyond.

While the risk-reward for the stock looks attractive at an initial glance, there are still a lot of conditions that need to be met before investor confidence is re-instilled back.

Dollar General is dethroned from its “defensive” play status after its Q2 earnings report. Is this warranted?

Last week, I dove into Dollar General’s Q2 Earnings report to understand the underlying causes driving the stock’s weakness. Dollar General has historically outperformed the S&P 500. Yet, after its earnings call, the stock lost over -36% of its value and has been dethroned from its “defensive” play status.

When I dug into the earnings report, it quickly became clear why investors have lost confidence in the stock. While Dollar General’s revenue growth is slowing and its operating and net income are declining on a year-on-year, it is the management’s latest guidance that has rightfully scared away investors.

The management is now guiding for revenue growth of 1.3-3.3% (vs. previous expectation of 3.5-5.0%) and diluted earnings per share decline of -22% to -34% (vs. previous expectation of -8% decline) in FY 2023.

Furthermore, the company’s net interest expense has doubled since last year, as the company has taken on debt to fund its capital expenditure and dividend payments to shareholders. Year-to-date, the company is free cashflow negative, and therefore cannot fund its outlays for capital expenditure and dividend payments using its free cashflow. This is worrisome, especially because interest rates are at a multi decade high, which makes borrowing expensive, causing interest expenses to balloon and squeeze net income.

Finally, the company is facing structural storm clouds today as the state of the economy and the world is changing. Business valuations have come under pressure due to higher interest rates, import costs are rising as the east-west gap widens putting pressure on gross margins, labor costs are growing as inflation proves to be stickier squeezing operating margins, consumer demand is weakening and to add to it all, organized retail crime is creating inventory shrink.

What is this post about?

Dollar General is undoubtedly under a lot of pressure today. But, that doesn’t necessarily mean that the future holds little to no upside. Or, does it? 🤔

It depends on how the management takes control of its fate and steer the company forward in the coming years, that will define whether Dollar General has long term upside or not.

While we (investors) cannot predict what the future holds for a business with certainty, we can use key business metrics to build possible scenarios that may play out for the company and position our portfolios based on our belief systems.

In this post, I will present to you 3 possible scenarios for Dollar General and its stock, given how the business evolves in the next 10 years and beyond. I will then present my final assessment and conclusion, as to whether I would invest in the stock or not.

My goal in this exercise is to provide you with a framework on how to think about evolving business and macroeconomic conditions to build a valuation model for a mature business. Determining the “fair” price of the company based on your assessment of its future cashflows can help you drive your investment decisions confidently. At the end of the exercise, I would urge you to conduct your own scenario analysis and make your investment decision independent from my assessment of Dollar General.

The bull, the bear and the neutral case for Dollar General

Here, I present to you the bull, the bear and the neutral case for Dollar General. Each scenarios contains an explanation of my thinking of how the business and macroeconomic conditions evolve, that I have built into the Discounted Cashflow Model to help me determine its “fair” price.

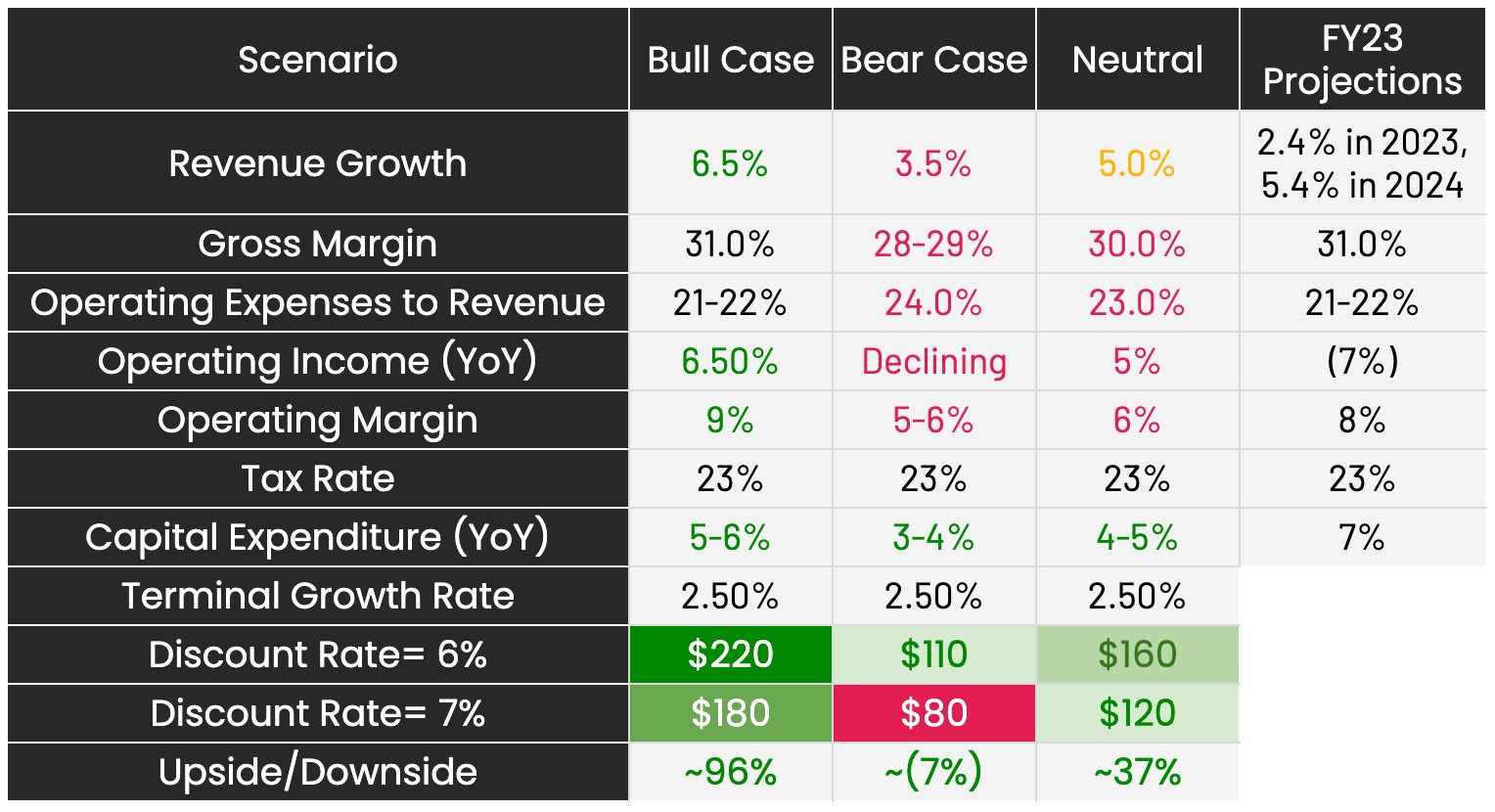

📈 The Bull Case: Dollar General’s Price Target = $180-$220

In this scenario, we expect Revenue to grow at 6.5% until 2030, and then at a Terminal growth rate of 2.5% after that. Please note that the revenue growth projection into 2030 of 6.5% is still materially lower than the 9% annual compounded growth rate since its IPO in 2009.

Gross Margin is expected to remain anchored at 31%. This would only happen if the economic narrative remains strong and inflation anchored.

We also expect Operating expense as a percentage of sales to remain anchored at its previous levels of 21-22%. In order for this to take place, we have to believe that the inflationary pressures on wages and rent are going to ease from here onwards.

As a result, Operating Income would grow more or less in line with Revenue growth at 6.5%.

Assuming that Capital Expenditure will grow at the rate of 5-6% every year, shares outstanding grows at -2.5% and the discount rate is between 6-7%, we believe that the Dollar General stock’s fair value stands at $180-$220. This implies an upside of approximately 96% from current price levels. Or in other words, Dollar General stock is undervalued by close to 96%.

Must haves for the bull scenario to play out: Inflationary pressures have to ease from here on, which will enable Dollar General to anchor its gross and operating margin. We further bet that the economy will not slip into a recession, which would hurt consumer demand and affect business revenue.

📉 The Bear Case: Dollar General’s Price Target = $80-$110

In this scenario, we expect Revenue to grow at 3.5% until 2030 and 2.5% after that.

Gross Margin drops considerably to 28-29%, as inflation proves to be stickier and structurally higher than the last decade.

Operating expense as a percentage of Sales goes up to 24%, as wage price inflation drives up labor costs and other operating expenses, such as rent and utilities.

In this scenario, Operating Income Margin will drop to 5-6% from its current levels and operating income will continue to decline.

Free Cashflow will turn negative in FY 2023 and FY 2024 and will then grow in line with revenue growth.

Assuming Capital Expenditure grows between 3-4%, shares outstanding grows at -2.5% and the discount rate is between 6-7%, we believe that the Dollar General stock’s fair value stands at $80-$110. This implies a downside of approximately 7% from current price levels. Or in other words, Dollar General stock is currently still overvalued by 7%.

😐 The Neutral Case: Dollar General’s Price Target = $120-$160

In this scenario, Revenue grows at 5% on a year-on-year basis until 2030 and then grows at the terminal growth rate of 2.5% after that.

The gross margin slightly drops to 30% compared to 31-32% in the previous decade. This is driven by an environment of higher than last decade’s inflation.

Operating Expense as a percentage of Sales goes up marginally to 23% driven by slightly higher labor costs.

Operating Income grows in line with revenue growth, but operating margin shrinks to around 7%.

While Free Cashflow would be negative in FY 2023, it would turn positive and grow in line with revenue growth afterwards.

If share float growth rate is at -2.5% and the discount rate between 6-7%, the Dollar General stock’s fair price would be around $120-$160. This implies an upside of approximately 37% from current levels.

What to make of it all?

The decision to invest in Dollar General is primarily a function of the belief that the management re-establishes its balance sheet discipline and that inflationary forces have peaked.

Currently from a risk-reward standpoint, there is an upwards of 37% upside (which could be as high as 100% upside, depending on factors), compared to -7% on the downside. In other words, there is a net upside of at least 30% , assuming that the company is able to turn its fate around.

Furthermore, the company is trading at a Trailing Price to Earnings ratio (PE ratio) of 10, which is well below its long term Average Price to Earnings ratio of 15. At the same time, the S&P 500 is trading at 19.8, when its earnings are supposed to grow approximately 0.5% in FY 2023.

On one hand, Dollar General PE ratio of 10 (vs. S&P 500’s PE ratio of 19.8) is fully warranted as Dollar General’s earnings are expected to decline 22-34% on a year-on-year basis, whereas S&P 500 is priced to deliver 0.5% earnings growth in FY 2023.

On the other hand, if the stock has to revert to its long term Average PE ratio of 15, that implies an upside of 50%. This would happen if in the upcoming quarters, the management is able to instill investor confidence from a combination of better balance sheet management and long term business forecasts.

Would I invest in the stock? Though there is attractive net upside on the stock today, I would choose to stay in the sidelines, until I get confirmation that the management is indeed taking active steps to build the business back up. At the same time, I am concerned about valuation pressures that the S&P 500 index faces in the background of steep interest rates. This environment is tricky to go bullish on individual stocks, as the overall macroeconomic environment is not supportive. Yet, if the management can show balance sheet rigor in its upcoming earnings call, I think the stock can rise significantly to the upside.

In case you want to understand how to read Dollar General’s balance sheet, Part 1 of this post (from last week) covers that. Take a look 👇🏽

Hope you enjoyed reading today’s post. See you on Thursday!!

Amrita 👋🏽👋🏽

Nice work, best for a short term bull, with the strikes by the Auto workers and the skirmishes and proxy war (read political money laundry on going ). They put that stab in the back speaker back in the diver’s seat.. No way out, unholy inflation will continue, but a short bull opportunity on options if you hedge correctly coming and going. I’m looking for a dead cat bounce.

Great article, I think the valuations along with your reasoning are spot on!