Pepsi smashed its Q3 earnings. Should you invest in the stock?

With Pepsi's stock down -10% YTD, I outline the investment case by building out my valuation framework. While the long term upside is intact, the short term downside risks may cause volatility.

At a Glance

PepsiCo smashed its Q3 earnings, as it delivered revenues and earnings that exceeded analysts’ expectations. Furthermore, the management has raised the company’s financial guidance for the FY 2023, as well as for FY 2024.

Pepsi is not only known for its defensive qualities, but also for its robust dividend growth history. That’s right. During the 2008 GFC crisis, when the average earnings of S&P 500 companies fell -78%, Pepsi’s earnings declined just -10%. Furthermore, the company has been increasing its dividend payout at a rate of 8.13% over the last 10 years.

Despite the company’s current efforts to optimize its operational efficiency, the stock is down -10% YTD, severely underperforming the S&P 500. In this post, I evaluate the investment case of Pepsi using 3 different valuation techniques.

Out of the 3 different valuation techniques, the one that I prefer the most is the “discounted cash flow” model and using this technique, I built my optimistic and pessimistic assumptions on the macroeconomic and business outlook to arrive at the bull and bear price target for Pepsi.

While there is a sizable upside for the long term investor, the short term downside risk is difficult to estimate. Read below to find out the price targets that I have laid out for Pepsi and my rationale for doing so.

PepsiCo PEP 0.00%↑ reported its Q3 earnings on October 10, 2023. Its revenues came in at $23.45B, which rose 7% on a year-on-year basis and its earnings per share came in at $2.25, which also grew at 16% on a year-on-year basis. Both revenue and earnings beat analyst expectations. In the meantime, the company also saw an improvement in its gross and operating margins by 105-bps and 80-bps respectively.

The management, despite warning that the US consumer is becoming more cautious, still offered a rosy outlook for the rest of the year, with revenue and earning per share (on a constant currency basis) expected to grow at 10% and 13% respectively. The management also offered a positive outlook for FY 2024, where it expects revenue to grow between 4-6% and earnings per share to grow in high single digits.

Yet, the stock is down -10% YTD, severely underperforming the S&P 500 index, which begs the question: Is it time to invest in Pepsi?

In this post, I will assess the investment case of Pepsi using 3 different valuation techniques.

The relative pricing model is where I look at the current forward Price to Earnings ratio and expected earnings growth rate of Pepsi and compare it with its competitors and the S&P 500 index to determine if the stock is over or under valued.

In the dividend discount model, I assess the current state of Pepsi’s dividend and build out its “fair” price using an expected dividend growth rate in perpetuity.

Finally, in the discounted cashflow model, I build out a bull and a bear case for the Pepsi stock, where I outline my assumptions on the overall macroeconomic and business conditions. This enables me to estimate the present value of Pepsi’s estimated future free cashflows, which then informs me whether the stock has potential upside or downside.

While all valuation models have limitations, I personally find the discounted cashflow model to be the most rigorous method, where the investor can intently build operational assumptions based on overall macroeconomic and business outlook. Therefore, if you want to skip directly to the discounted cashflow model, please go to Section 4.

1. Pepsi offers both defense and dividends. Plus, its latest strategy is helping it optimize its pricing strategy.

Pepsi is not only known as a defensive play, but it is also a dividend king at the same time. The company has been increasing its dividends by 8.13% annually on average over the last 10 years. It has been able to do that because of its relentless focus on driving product innovation and balance sheet discipline, which enables it to weather tough times.

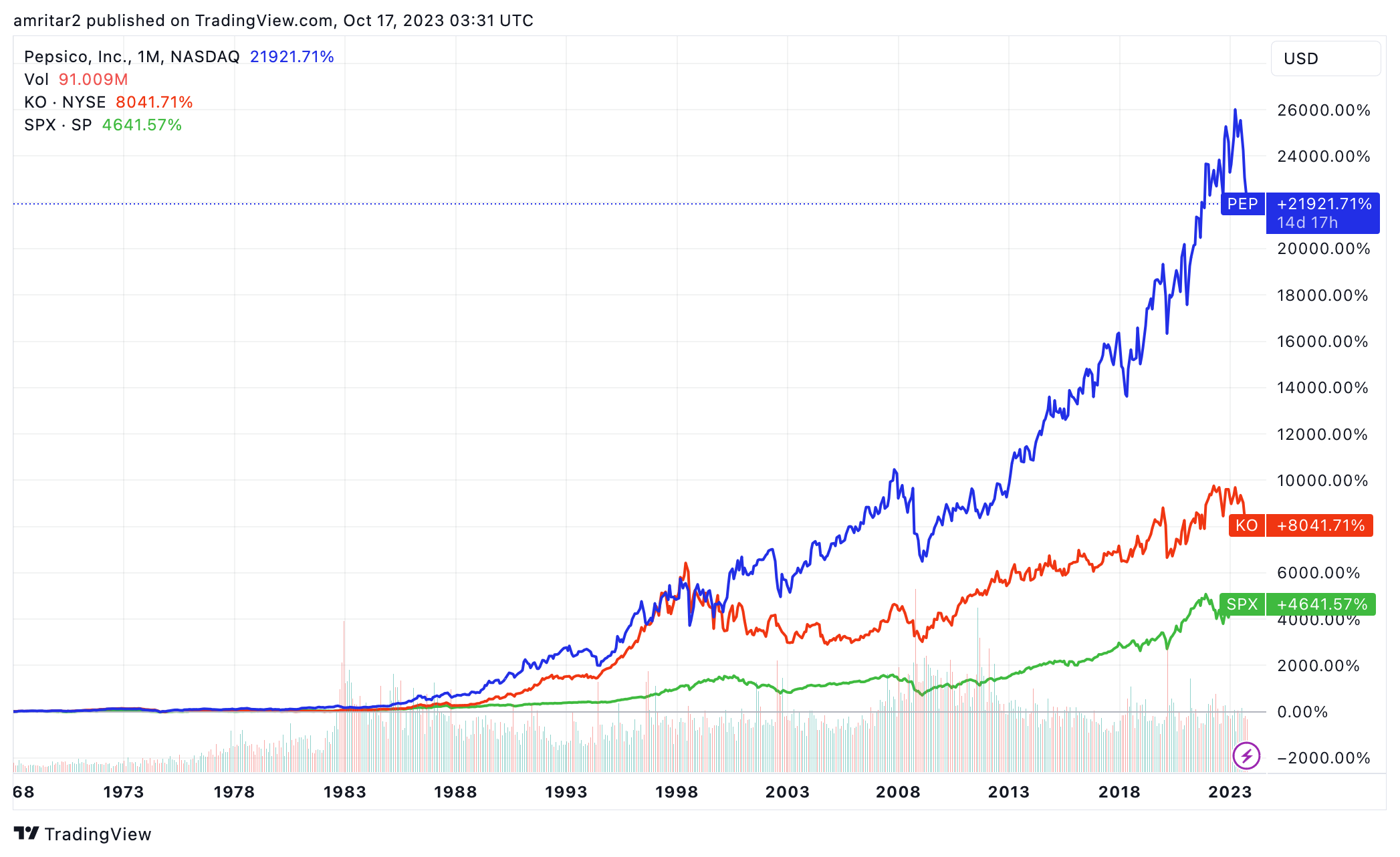

During the 2008 Great Financial Crisis, Pepsi’s sales went down by -0.5% and its earnings dropped by -10% on a year-on-year basis. In the meantime, the average earnings of S&P500 companies fell by -78% between December 2007 to December 2008. While the stock did take a beating of -35%, it is significantly lower than -55% decline in the S&P 500 index. Furthermore, the company managed to outperform the S&P500 index and its main competitor Coca-Cola KO 0.00%↑ during the 1970’s inflationary period and beyond, as the company had made some shrewd investments to build out its snack portfolio.

In 2023, Pepsi has introduced smaller pack sizes to cater to consumers who are increasingly health and cost conscious. For instance, Pepsi’s Frito-Lay North America segment has managed to gain market share in the macro and savory snack categories in Q3 2023, as a result of smaller pack sizes as well as the introduction of bite-size Doritos, Cheetos and SunChips brands. This strategy has enabled Pepsi to better adjust their pricing strategy, which subsequently has contributed to the overall margin expansion, despite moderate decline in sales volume.

2. Let’s assess Pepsi’s investment case using a relative pricing model.

Despite Pepsi’s business strength, the stock is down -10% YTD, severely underperforming the S&P500. Historically, Pepsi has outperformed the S&P 500 and its core competitor Coca Cola since the 1970s, as can be seen in the chart below.

However, if we look at the relative pricing of Pepsi based on its earnings growth in 2024 compared to S&P 500, the case for investment becomes a little unclear.

In this exercise, I look at the Price to Earnings ratio (PE ratio) of Pepsi and compare it to its 10 year historical average to see if the stock is currently trading at a premium or at a discount. Furthermore, based on Pepsi's projected earnings growth in 2024, I compute the adjusted PE ratio that the stock should be trading at or around, given the S&P 500’s forward PE ratio.

In summary, this method is telling us that on one hand, Pepsi is trading below its 10-year average PE, implying an upside of 21%. On the other hand, given the relative pricing of S&P 500 in 2024, Pepsi could still have another -35% downside. Given the risk-reward, there is no investment case yet for Pepsi, using the relative pricing model.

❗❗However, this method is not without its limitations, as it has a very short time horizon. So, let’s dissect Pepsi using its dividend as a guide to determine if there is an investment case.❗❗

3. The state of Pepsi’s dividend and estimating Pepsi’s fair value using a dividend discount model.

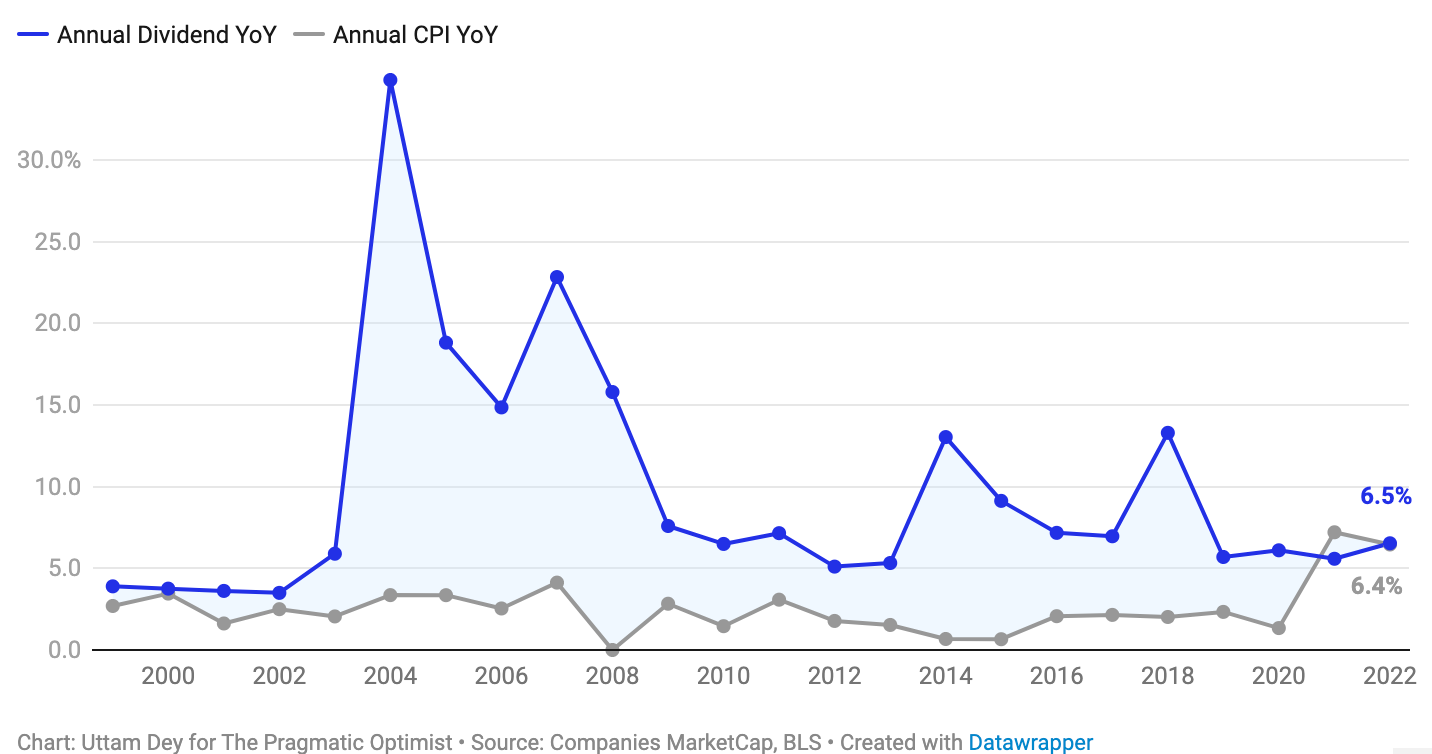

Pepsi has the “Dividend King” status as the company has been consistently increasing their dividend payouts since 1965, where dividend per share has been increasing at an average rate of 8.13% over the last 10 years.

✅ In fact, Pepsi’s dividend growth rate has been outpacing inflation. This means that if you are an investor who had invested in Pepsi, you would have a real return (nominal dividend yield - inflation) on your dividend, which would have improved your overall purchasing power.

✅ Furthermore, today the dividend yield is slightly higher compared to its long-term average of 2.8%. The Dividend yield is a financial ratio that tells you the percentage of a company’s share price that it pays out in dividends each year. When the current dividend yield is lower than the long term average dividend yield, it is a possible sign of undervaluation.

❌ However, if you look at the spread between the 10Y Treasury bond yield and the current dividend yield, the 10Y Treasury bond offers higher yield, which is a dampener for income-seeking investors to invest in a company like Pepsi.

This is similar to the decade before 2000, when 10Y Treasury bond yields offered higher yields than Pepsi’s dividend yields, which was offset by the fact that Pepsi’s dividends would grow each year.

So, in today’s environment, if we believe that Pepsi will continue to increase its dividend payout at a growth rate, such that it offsets the current yield on the 10Y Treasury bond, there is a decent investment case for the stock.

Alternatively, we could have a recession, where 10Y Treasury bond yields would likely collapse, in which case the spread will become positive (similar to the 2010 decade) and the investment case for Pepsi would be strong, once the dust settles.

So, based on the above information, we can quickly build Pepsi’s fair value of the stock based on its bull and bear case of its future dividend growth rate.

In the bull case, we assume Pepsi’s dividend to grow at a rate of 5.5% in perpetuity, with cost of equity at 8%. In this case, Pepsi’s “fair” value should be at $213.

In the bear case, we assume Pepsi’s dividend to grow at a rate of 3.5-4%, with the cost of equity at 8%, in which case, Pepsi’s fair value would be at $120-$130.

❗❗The problem with the dividend discount model is that it forces us to assume a dividend growth rate into perpetuity, which could be very limiting and dangerous, if the company does in fact run into obstacles down the path, where it needs to cut or pause its dividend program, as we saw with many companies during the Covid-19 pandemic.❗❗

4. Building the bull and bear case of Pepsi using a discounted cashflow model.

The final method that we will use to determine Pepsi’s investment case is use a discounted cashflow model, that we had earlier used to determine Dollar General’s bull and bear case last Tuesday.

Thus, I present to you the bull and the bull case for PepsiCo. Both of these scenarios contain an explanation of my assumptions that I have built into the model, to help me determine Pepsi’s “fair” price.

📈The Bull Case: Pepsi’s price target = $260

In this scenario, we expect Revenue to grow at 7% until 2030, and then at a Terminal growth rate of 3.0% after that, into perpetuity.

In my opinion, this will be primarily driven by growth in its snack division Frito-Lay (which has the 2nd largest revenue contribution to top line), as well as growth in international markets.

Furthermore, this scenario does not believe any material damage to Pepsi’s top-line growth would take place, from the sensational weight loss drug Ozempic that claims to reduce appetite and change consumer consumption pattern.

Gross Margin is expected to be at 54%, which is slightly higher than the gross margin of the last 2 years.

This would happen if overall inflation remains anchored or decline from current levels and Pepsi’s distribution channels remain robust. Today, some of the headwinds associated with Pepsi are the rising prices of sugar, which is a key raw ingredient in Pepsi’s products.

We also expect Operating expenses as a percentage of sales to remain anchored at its previous level of 40%.

In order for this to take place, the company need to actively manage its costs, which it is doing today, in the form of cutting back on marketing promotions and driving more targeted outreach in order to achieve a better margin.

Furthermore, wage inflation would need to stay anchored or decline.

As a result, Operating Income would grow in line (or higher) with Revenue growth at 7%.

Today, Frito Lay North America segment has the highest operating margin at Pepsi at 28%, whereas PepsiCo Beverages segment has the lowest operating margin at 13.5%. Latin America and Asia Pacific are the most profitable international market segments, whilst contributing 18.2% of total revenue.

Assuming that Capital Expenditures grow at 4.5%, in line with long term trend and shares outstanding decline by -1.5%, we believe that Pepsi’s fair value stands at $260, given a discount rate of 8%.

This implies an upside of approximately 62% from its current price levels.

📉The Bear Case: Pepsi’s Price Target = $225

In this scenario, we expect Revenue to grow at 4.5% until 2030 and 2.5% after that. This could be driven by a multitude of factors, such as a prolonged recession, changing consumer consumption habits and the inability of Pepsi to innovate rapidly and a slowdown in international markets.

Gross Margin drops to 52% compared to 53% today. While it could drop even more, this will be driven by raw input inflation and weakness in Pepsi’s distribution network.

Operating expense as a percentage of Sales rises to 42%, as wage price inflation drives up labor costs and ROI of marketing initiatives decline.

In this scenario, Operating Income Margin will drop to 11%, as Frito Lay and international markets may not prove to grow at the rate which was originally expected.

With the same assumptions of Capital Expenditure and share buyback as above, we believe that Pepsi’s fair value in the bear-case is approximately $226, at a discount rate of 8%. This implies that even in bear-case, Pepsi has a potential upside of 41%.

5. What to make of it all?

The decision to invest in Pepsi is primarily a function of the belief that the management can effectively continue to innovate on its product portfolio and gain market share in international markets, while maintaining balance sheet disciple, which would allow it to increase its dividend payouts.

Today, the management is actively working on clever strategies with package sizes to adjust its pricing strategy. And so far, the strategy has paid off, as margins have improved and offset the decline in sales volume in Q3. Furthermore, the company is actively driving cost efficiencies across its marketing channels at a time, when the macroeconomic conditions are broadly uncertain.

In the earnings call, the Chairman and CEO Ramon Laguarta said that Pepsi is positioned to perform well in the coming years as growth normalizes because the company has made numerous investments in their brands, manufacturing capacity, go-to-market systems, supply chain, technology and people in order to execute against their strategic framework and modernize the company.

Given the company’s long-term track record and its current commitment, I believe that there is room for optimism. While the relative pricing model did not clearly outline an attractive risk-reward for Pepsi’s stock, I believe the bull and the bear case outlined by the discounted cashflow model, demonstrates the long term investment thesis in the company, despite short term headwinds that may occur from valuation compressions and/or a recession.

Currently from a risk-reward standpoint, there is an upside of 62% in the bull case and a 41% upside in the bear case scenario in the discounted cashflow model. In the meantime, the relative pricing model paints the worst possible outcome, which could be a downside of -35% for the stock from its current levels. However, I am not fully confident of the magnitude of the downside, because of the short-sighted nature of the relative pricing model.

Whether one invests in Pepsi now, vs. later, would ultimately depend on their time horizon and their margin of safety. Simply put, if you believe in Pepsi’s management and think that the US Fed is done hiking rates and the economy is not going to enter a recession, then Pepsi could potentially provide upside. However, if you believe that the US economy is about to enter a recession, then I would recommend to stay in the sidelines.

Note: I don’t hold any position in PEP 0.00%↑ . You are fully responsible for doing your own investment research before you invest in a stock. My recommendation is not to be taken as financial advice.

That’s all for today!! Are you a Pepsi bull or bear? Leave your answer in the comments below.

Amrita👋🏽👋🏽

Thank you for this Amrita. Very easy to understand. I'll do a bit more reading but I think you might have convinced me to invest in some PepsiCo. (he says whilst sipping on a Pepsi Max. Not healthy I know.)

Nice work, hopefully we see a bull... However looking out upon the Horizon there’s already the worst housing market since the bubble burst 2008, and then there’s the Auto Union ready to kill the goose... All floating on a sea of gov’t inflated cash, and even worse the collapse of the dollar as the reserve currency (which already begun, only no other currency is as yet fully empowered or motivated). Unnecessary war so that the gov’t can empower itself and screw the ppl. Indeed we are our own worst enemy. There’s no other reason to explain the methodical disassembly of what once was a very healthy economy.