S&P 500 hit a new record. What I have learnt from the Q4 earnings so far?

Bank earnings were mixed. Consumer demand for air travel remains robust. TSMC is bullish on AI demand. CEOs at Davos are optimistic even though geopolitical, trade & election uncertainties remain.

Welcome back to The Pragmatic Optimist’s edition of the Monday Macro.

««Monday Macro- The 2-minute version»»

As Wall Street celebrates new all-time highs for the S&P 500, there is growing optimism that the US economy is indeed headed for a soft-landing. While there is no doubt that the S&P 500 has defied all the doubters so far, are Q4 earnings echoing the same optimism? Partially.

Kicking it off with the big banks: JPMorgan made a record $50B in profit in 2023. Along with Wells Fargo, Citigroup and Bank of America, the four largest banks in the US earned $104B in profit in 2023, thanks to a resilient consumer and economy.

However: Trouble in commercial real estate could be brewing with record high vacancy rates, higher borrowing costs and falling prices. Bank of America said it charged off more than $100M tied to eight office buildings, while Well Fargo said it charged off $377M in commercial real estate loans. On the consumer credit side, auto loan delinquencies rose above pre-pandemic levels at both JPMorgan and Wells Fargo in Q4.

On the bright side: Investment-banking revenue picked up after 2 years of drought. Possible indications of a bottom?

Hiring remains selective: While JPMorgan said that it will continue hiring for bankers, wealth management advisors and front office employees for new branches, Goldman Sachs and Bank of America remain cautious with indications that AI can reduce the need for some roles. Meanwhile, Citigroup is expected to layoff 20,000 employees by 2026 as part of a restructuring under their new CEO.

Demand for air travel remains robust: With Delta Airline doubling its quarterly profit, CEO Ed Bastian remains upbeat about the outlook for air travel in 2024. There is some good news for travelers in 2024, with airfares falling below pre-pandemic prices. Plus, corporate travel demand is also improving, with workers ending labor strikes after reaching new contracts last year.

What about AI? Taiwanese chip manufacturing giant, TSM expects 2024 to be a healthy growth year, supported by a strong ramp-up of the industry-leading three nanometer technologies, robust demand for the five nanometer technologies and sustained AI-related demand. Meanwhile, UBS expects AI to grow into a $225B market by 2027.

Optimism in Davos: Meanwhile, CEOs from Rockwell Automation, Intel, PepsiCo, Honeywell and more remain optimistic about the US economy and the strength of consumer demand. despite ongoing geopolitical, trade and election uncertainties in the US and abroad.

S&P 500 reached an all time high. That’s right. 513 trading days and 11 rate hikes later, S&P 500 has defied the doubters.

Last month, Americans kept shopping that helped propel the economy forward. With retail sales growing higher than expectation at 5.6% on a YoY basis, the US economy is now expected to grow 2.4% in Q4. Cooling inflation is one of the drivers of consumer spending. Since last May, average hourly earnings have been rising faster than consumer prices, which has boosted workers’ inflation-adjusted spending power. At the same time, while pandemic related savings have been drawn out, there still appears to be some savings buffer left. Meanwhile, employment growth has moderated while initial claims for unemployment benefits show that layoff activity remains contained.

Consumer sentiment also echoes the growing optimism, as it surged 29% since November, the biggest two-month increase since 1991. A better mood among Americans is good for growth since happier consumers are likely to keep spending, and that consumption drives close to 70% of the US economy.

So, is it time to let our guards off and celebrate the “soft” landing?

At the Pragmatic Optimist, I like to remain vigilant and one of the ways that I do this is by diving into key industry defining earnings reports and events which allow me to understand the evolving pulse of the economy and connect the dots to build a well-balanced thesis for where the US economy is heading.

So, let’s dive right in👇🏼👇🏼👇🏼

Bank earnings are a mixed bag. Rising commercial loan defaults & job cuts are to watch for.

Kicking off the earnings season, JPMorgan Chase JPM 0.00%↑ made a record $50B in profit in 2023. Along with Wells Fargo WFC 0.00%↑, Citigroup C 0.00%↑ and Bank of America BAC 0.00%↑, the four largest banks in the US earned $104B in profit in 2023, up 11% on a YoY basis.

“The consumer still has plenty of firepower,” Alastair Borthwick, CFO of Bank of America, said during the earnings call.

Jamie Dimon, CEO of JPMorgan echoed with Bank of America’s commentary on consumer resilience.

“The US economy continues to be resilient, with consumers still spending, and markets currently expect a soft landing,” Dimon said in the earnings release.

Trouble in the Commercial Real Estate Sector could be brewing.

The four banks charged off $6.6B in loans in Q4, twice as much as in the same period a year ago. Particularly, loans tied to the struggling commercial real estate sector are a sore spot. Bank of America said it charged off more than $100M tied to eight office buildings, while Well Fargo said it charged off $377M in commercial real estate loans.

According to Capital Economics, commercial real estate could face a reckoning this year as property values continue to fall. The research firm pointed to the difficulties commercial real estate faced last year, with property values falling an estimated 11%. Prices are set to fall another 10% this year, the firm estimated, spelling trouble for the debt backed by commercial buildings.

"Distress is only just emerging and 2024 could be the year the dam bursts,” Capital Economics deputy chief property economist Kiran Raichura warned in a note.

Meanwhile, a recent survey from the Mortgage Bankers Association (MBA) found missed payments on loans backed by office properties jumped to 6.5% of balances at the end of Q4, up from 5.1% in the prior quarter.

"Long-term interest rates have come down from their highs of last year, which should provide some relief to some loans, but many properties and loans still face higher rates, uncertainty about property values and changes in fundamentals," Jamie Woodwell, MBA's head of commercial real estate research, said in a press release.

Office loans have been weighed down by depressed demand for working spaces since the pandemic. The persistence of work-from-home and hybrid models have pushed office vacancies up to all-time highs.

A recent report from Moody's Analytics described the US office market as being in "uncharted territory" with vacancy rates notching a record 19.6%.

The commercial real estate sector has been in a pinch ever since interest rate hikes made borrowing money a lot more expensive. Higher rates have made refinancing existing debt much more difficult for borrowers and risky for lenders. That's a huge problem for commercial property owners, who have around $1.5T of debt that's approaching maturity.

Consumer Credit may be seeing pockets of stress in auto loans.

Shifting gears to consumer credit, executives cautioned that rising loan losses were to be expected as the pandemic stimulus fades into the rearview mirror, though they said that the losses don’t look particularly worrisome.

“The way we see it, the consumer is fine. All of the relevant metrics are now effectively normalized,” JPMorgan CFO Jeremy Barnum said.

Executives pointed to the labor market as the key to consumer strength. But there are signs that high costs have started to leave more consumers overstretched.

“The modest deterioration Wells Fargo has seen in credit is in line with its expectations and average deposit balances per customer remain above pre pandemic levels. Having said that, there are cohorts of customers that are more stressed.” said Charlie Scharf, CEO of Wells Fargo.

Yet, Americans are increasingly struggling to keep up with their monthly car payments, which have ballooned in size. Car prices shot up during the pandemic, and higher interest rates made monthly payments more expensive. Auto delinquencies rose further above pre-pandemic levels at JPMorgan and Wells Fargo in Q4.

New signs of life in Investment Banks?

Meanwhile, investment-banking revenue showed signs of picking back up in Q4, and fees rose at JPMorgan, Citigroup and Bank of America. Debt underwriting powered the gains, and executives projected optimism about deals in the new year. Loans to businesses were up in Q4 at JPMorgan, Bank of America and Citigroup.

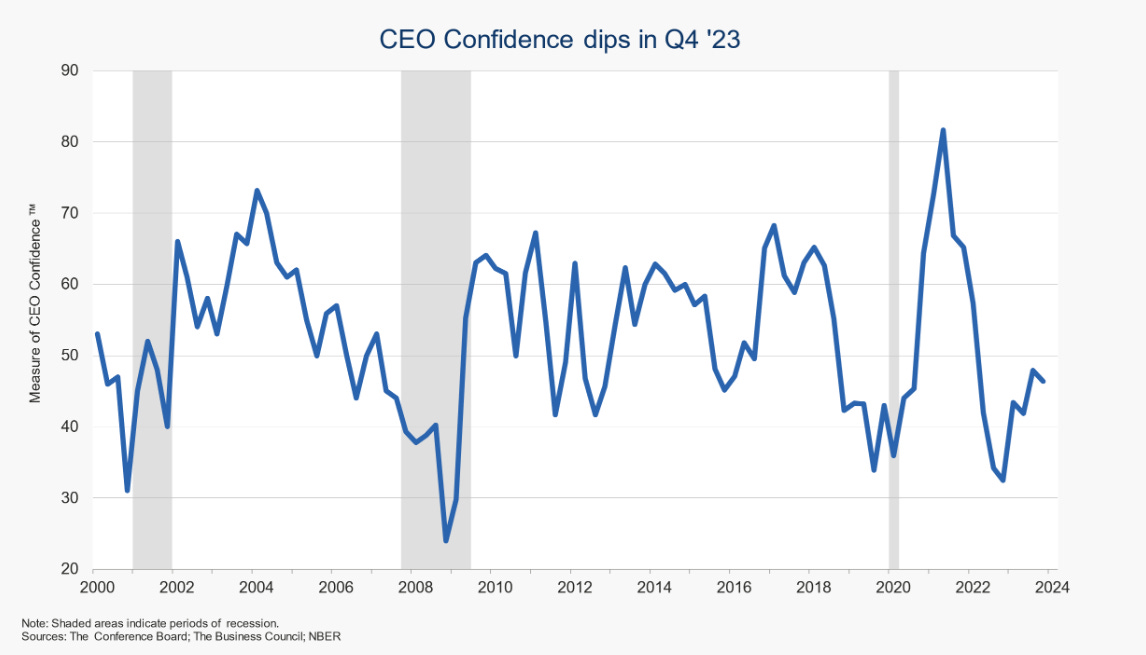

One of the other leading indicators of a possible pickup in IPO & M&A activity in 2024 is to watch for the trend in CEO Confidence as measured by the Conference Board. While CEO Confidence has been improving through 2023 onwards, it is still nowhere near the levels reached in 2021, when global M&A hit a record $5T.

Job outlook for 2024 in Wall Street’s biggest banks

Pivoting to the overall trend in hiring, Wall Street’s biggest banks have laid off thousands of employees in 2023, and more cuts are coming. Citigroup kicked off 2024 ominously, warning that it will lay off as many as 20,000 employees by 2026. But the bank is also going through a restructuring under CEO Jane Fraser and is not necessarily representative of the rest of the industry.

JPMorgan reported that in 2023 it increased compensation spending by 12%, and the bank's CFO Jeremy Barnum said on the call that hiring would continue for bankers, wealth management advisors, and front office employees for new branches.

Goldman Sachs GS 0.00%↑ has also been shrinking staff amid an M&A and IPO drought, although the bank’s CFO Denis Coleman said that the market for talent remains competitive.

"We're staying true to our mantra of pay for performance. It's what our people expect, and it's one of the things that enables us to attract such exceptional talent and deliver excellence for our clients," Coleman said during the earnings call.

Meanwhile, Bank of America execs suggested there was more room for headcount to fall organically. As AI and technology initiatives reduce the need for some roles, they've been redeploying people internally and curbing the need for external hires.

Looking ahead…

Looking ahead, Jamie Dimon cautioned that deficit spending and supply chain adjustments may lead inflation to be stickier and rates to be higher than markets expect. He also added that central banks’ steps to rein in support programs and wars in Ukraine and Middle East are some of the unprecedented forces that pose risk to the US market and economy.

Still missing a (possibly) big piece of the puzzle

Personally, I believe that while the bank earnings point to a somewhat resilient US economy with possible pockets of stress developing, I believe that a bigger blackhole is the growing stress in small and mid-size private companies in the US.

According to Marblegate Asset Management, which focuses on distressed credit and private credit, EBITDA margins collapsed by 25% in private mid market companies, while Russell 3000’s margins only softened by 2% between 2019 and end of 2022. Meanwhile, financial leverage rose 62% in the midmarket in stark contrast to public companies where it declined 12%. In 2023, rising interest costs were a major source of stress for companies across the midmarket, which mostly borrow from regional banks and private credit funds using floating-rate debt.

With bankruptcies in the private mid market companies on the rise, how will this stress ripple into the broader economy, particularly in the labor market? After all, the strength of the labor market has driven the consumer spending growth that’s been keeping the economy strong so far.

Consumer demand for air travel remains robust. The trend will likely continue. Thanks to cheaper air tickets.

Delta Air Lines DAL 0.00%↑ closed out the year by doubling its quarterly profit as travel demand, particularly for international trips, helped drive record revenue in 2023. CEO Ed Bastian said continued strong travel demand could boost earnings this year.

“Business is going great. Just go to any airport,” Bastian told CNBC in an interview.

Delta’s president, Glen Hauenstein, said in a news release that the carrier has seen strong demand for international travel that has outpaced US flight revenue. Furthermore, record numbers of people paid to sit in Delta’s higher-priced cabins such as first class or premium economy in Q4, driving revenue from premium cabins up 15% during the period, outpacing 10% revenue growth from standard coach seats.

Corporate travel demand is also improving, Delta’s CEO said, pointing to growth from the technology sector as well as auto and entertainment industries, whose workers ended labor strikes after reaching new contracts last year.

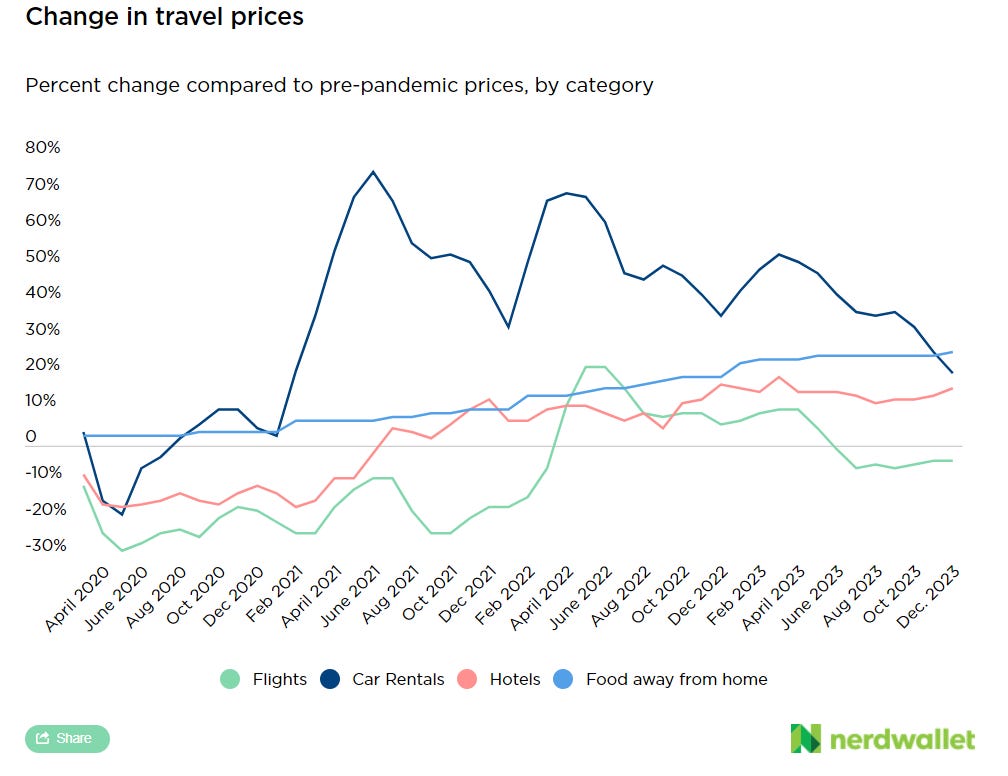

Looking ahead, there is good news for travelers. Airfares are significantly cheaper than they were this time last year. Last month, airfares were down (9.4)% versus the same month in 2022, and they are 3.6% lower than what they were in December 2019, before the pandemic. That’s according to the latest set of Consumer Price Index (CPI) data. Car rental prices are also lower, down (12)% versus December last year. Hotel prices are also slightly lower since last year, down 0.5%.

Falling travel prices is a bright spot for customers. Coupled with a healthy job market, demand for travel, especially ones involving air travel, will likely remain robust in 2024.

TSMC is bullish on AI demand in 2024, while UBS projects AI to grow into a $225B market by 2027.

Taiwanese chipmaker TSMC TSM 0.00%↑ projected more than 20% growth in 2024 revenue on booming demand for high-end chips used in artificial intelligence applications even as the broader industry deals with weak smartphone and electric vehicle sales.

“We expect 2024 to be a healthy growth year for TSMC, supported by continuous strong ramp-up of our industry-leading three nanometer technologies, strong demand for the five nanometer technologies and robust AI-related demand,” said Wei.

Looking ahead, TSMC said it plans to expand its global manufacturing footprint, with construction at its fab plant in Germany expected to begin in Q4 of this year, while the company is still deciding on what technology node to build at a second fab in Arizona.

It forecast capital spending at $28-$32B for 2024, in line with 2023, and said it will also expand production at home in Taiwan.

The performance and guidance from TSMC are in line with the overall narrative that 2024 will be the year that AI solidifies its position as a dominant investing theme. Furthermore, as per UBS, AI is expected to grow into a $225B market by 2027.

Stronger-than-expected demand will be a boost for AI software moving forward, fueling a 138% CAGR for the application sector.

"If the launch of the ChatGPT application is the iPhone moment for the AI industry, the recent rollouts of numerous applications like copilots and features like Turbo and vision from OpenAI in Q4 2023 mean the App Store moment for the AI industry has arrived, in our view," the UBS report said.

Meanwhile, increased clarity around AI infrastructure spending will also contribute to tech's multi-year momentum. The segment is expected to grow from $25.8B in 2022 to $195B in 2027.

"This will likely make AI one of the fastest-growing and largest segments within global tech and arguably the 'tech theme of the decade,' as we don't see similar growth profiles elsewhere in tech," the report said.

The general sentiment amongst global CEOs at Davos is one of optimism, despite ongoing geopolitical, trade and election uncertainties.

At the annual gathering of more than 800 CEOs and chairs, business leaders ticked off their reasons for confidence about the economy. PepsiCo PEP 0.00%↑ CEO Ramon Laguarta said he is encouraged by what he described as a stabilizing job market and falling prices for some commodities. Honeywell HON 0.00%↑ CEO Vimal Kapur noted demand for air travel remains strong. At the mining giant BHP BHP 0.00%↑ , CEO Mike Henry said the appetite for copper, iron ore and other materials remains high worldwide.

The concern is that geopolitical events could strain confidence among CEOs and make it harder for companies to run their businesses or ship their products around the world. There are also elections in more than 60 countries in 2024, impacting roughly half of the global population. Besides the US election in November, countries including India, Indonesia and the United Kingdom have elections planned for later this year.

Pat Gelsinger, CEO of Intel INTC 0.00%↑, said the uncertainties are real but the chip market is well-positioned.

“Geopolitically, I think it’s going to be a turbulent year. You have lots of elections going on. We have two active wars in the world that affect supply chains in a meaningful way,” Gelsinger said.

Despite the tumult in the world, a number of CEOs said they remain optimistic.

“The world crises keep stacking one on top of the other,” said Blake Moret, CEO of industrial automation company Rockwell Automation ROK 0.00%↑. “But, for the moment, for the economy, the underlying demand continues to be positive.”

“Demand for air travel remains robust”

Especially for jets without screen doors

I think that TSMC datapoint is a very important one. Discussed it in my weekend report as well. Worth noting the global chip industry saw its first y/y gain in sales in 14 months.