The US labor market is resilient. But, is the US consumer healthy| Part 2

The US labor market shows early signs of weakness with new round of layoffs & CEOs leaving at a record pace, consumer savings are depleted & non-mortgage debt service payments grows at a faster rate.

Today’s Monday Macroviews at a glance

The US consumers’ willingness to maintain spending levels despite a slower economy and rising prices proved to be important at a time when many anticipated the potential onset of a recession.

The US consumer has been buoyed by a strong labor market. However, the labor market is showing early signs of weakness, as the growth rate in wages have peaked and millennials and GenZs are increasingly seeking gig work to shield themselves against the rising cost of living.

Excess savings from the pandemic is almost over. Turns out that the low and middle income households have drawn out their savings at a much faster rate, compared to the upper and upper-middle income segment. At the same time, the lower income segment has tapped into credit card debt at a rate that exceeds the pre-pandemic range, suggesting the magnitude of pain that high inflation and interest rates are inflicting on this segment of households.

While household debt has reached an all time high of $1.7T, household debt service payments relative to disposable personal income is not sending any economic warning signs. However, non-mortgage debt service payments are growing at a faster rate than normal and increasingly squeezing disposable personal income.

Read below to find out if the US consumer is really healthy, or about to catch a cold, as we dig into the data and outline key indicators to watch for to continually assess the evolving health of the US consumer.

For much of the last year, recession fears have been building up against a sharp rise in interest rates and market uncertainty. But to everyone’s surprise, the US economy has continued to defy the bold recession prediction (so far), thanks to a resilient labor market.

Remember, a resilient labor market equates to a resilient consumer. Consumer spending plays the most important role in driving the US economy, typically representing about 75% of total economic activity in the US. With non-farm payrolls growing at 2.1% and wages growing at 4.2% on a year-on-year basis, nominal consumer spending is growing at 5.8%. In fact, US retail sales increased 0.7% in September, which was higher than expectation, as households stepped up purchases of motor vehicles and spent more at restaurants and bars.

But how are the US consumers funding their expenses? Are wages sufficiently high enough to cover all the expenditures? Or, are the US consumers being forced to tap into their savings and take on additional credit card debt to cover the cost of living?

In this post, we will assess the underlying financial health of the US consumer across the following dimensions:

Labor Market: Is it really all that resilient?

Consumer Savings: Has the rise and fall of pandemic-fueled excess savings been even across all income groups?

Household debt: As household debt rises to record levels, will the US consumer be able to pay it back?

Let’s jump right in! 👇🏽

1. Are we starting to see early signs of cracks forming in the US labor market?

While nominal wages are growing at a faster rate than headline inflation, there are pockets of categories, such as housing, both rented and owned, where prices are growing at twice the rate of wage growth. Remember, housing constitutes 33% of all consumer spending. This is taking place in an environment, where wages are now growing at a much slower rate.

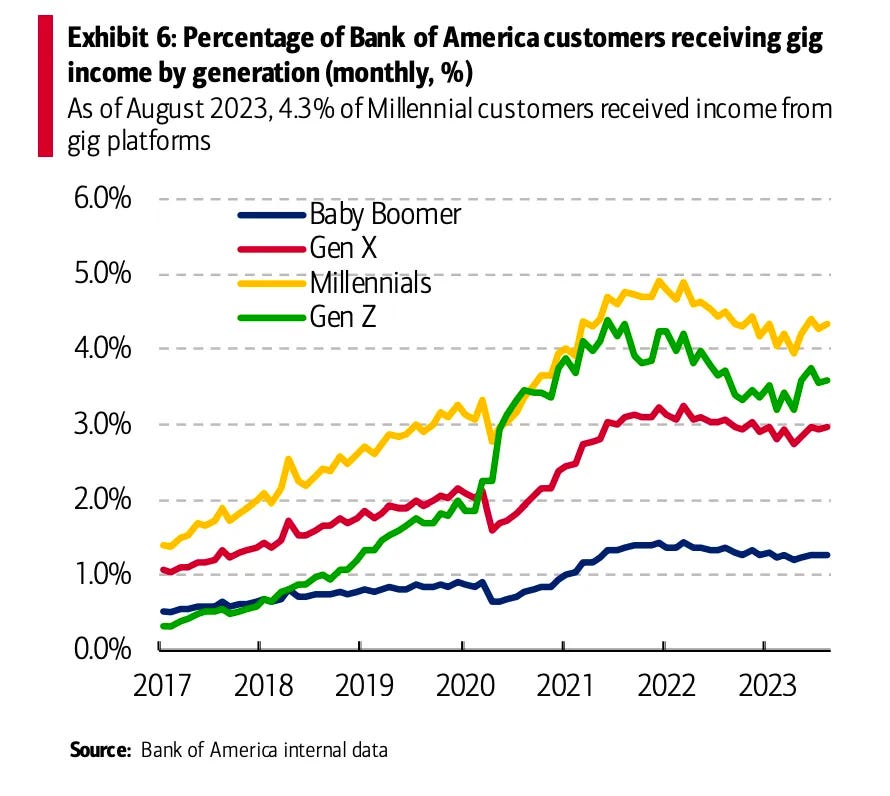

While this is a welcome sign for overall inflation to return to the Fed’s long-term 2.2% inflation target, the latest consumer report from Bank of America sees an uptick in gig jobs over the past few months. Specifically, the percentage of Bank of America customers who received income from gig platforms through direct deposit or debit cards reached 3% in August 2023, up from 2.7% in April 2023.

The increase in gig job participation seems to be driven by younger generations, with millennials continuing to represent the biggest cohort. As of August 2023, 4.3% of millennial customers received income from gig platforms. Next was Gen Z, with 3.6% of customers seeing gig income inflows in August 2023.

With millennials set to represent 75% of the workforce by 2025 and Gen Zs fast on their heels as greater numbers enter the workforce, they will increasingly represent the majority of consumer spending.

Yet, millennials and GenZs are the most exposed to the rising cost of living, as they tend to move more frequently, either for work, to accommodate expanding families, or more broadly, as they seek more space as they age. If this generation has to increasingly pick up multiple jobs to cover the cost of living, we might be looking at a prolonged period of weak consumer spending, should the labor market deteriorate further.

In fact, there were some significant layoff announcements at companies such as LinkedIn, Flexport, Qualcomm, and others last week. At the same time, 1400 US CEOs have left their positions so far this year, up 50% on a year-on-year basis. This is the highest on record since tracking began in 2002.

In the meantime, the US consumer has now mostly depleted their excess savings that they had accumulated from a combination of fiscal stimulus and economic closures during the pandemic.

2. Is the rise and fall of consumer savings been even across income groups?

Pandemic-related fiscal support resulted in a sizable increase in disposable income in the overall US economy at a time when health-related economic closures and social distancing led to a significant drop in household spending. As a result, aggregate personal savings rose rapidly, far beyond its pre-pandemic trends and much higher than in previous recessions.

From the chart below, you can see that there was a total of $2.1T in excess savings that accumulated during the pandemic, which peaked in August 2021. After August 2021, aggregate personal savings dipped below the pre-pandemic trend, signaling an overall drawdown of pandemic-related excess savings. Since then, cumulative drawdowns have reached $1.9T as of June 2023, implying that there is less than $190B in excess savings remaining in the aggregate economy.

Should the recent pace of drawdowns persist, aggregate excess savings would likely be depleted in Q3 2023.

But, are people from all income groups experiencing the same magnitude in the fall of savings?

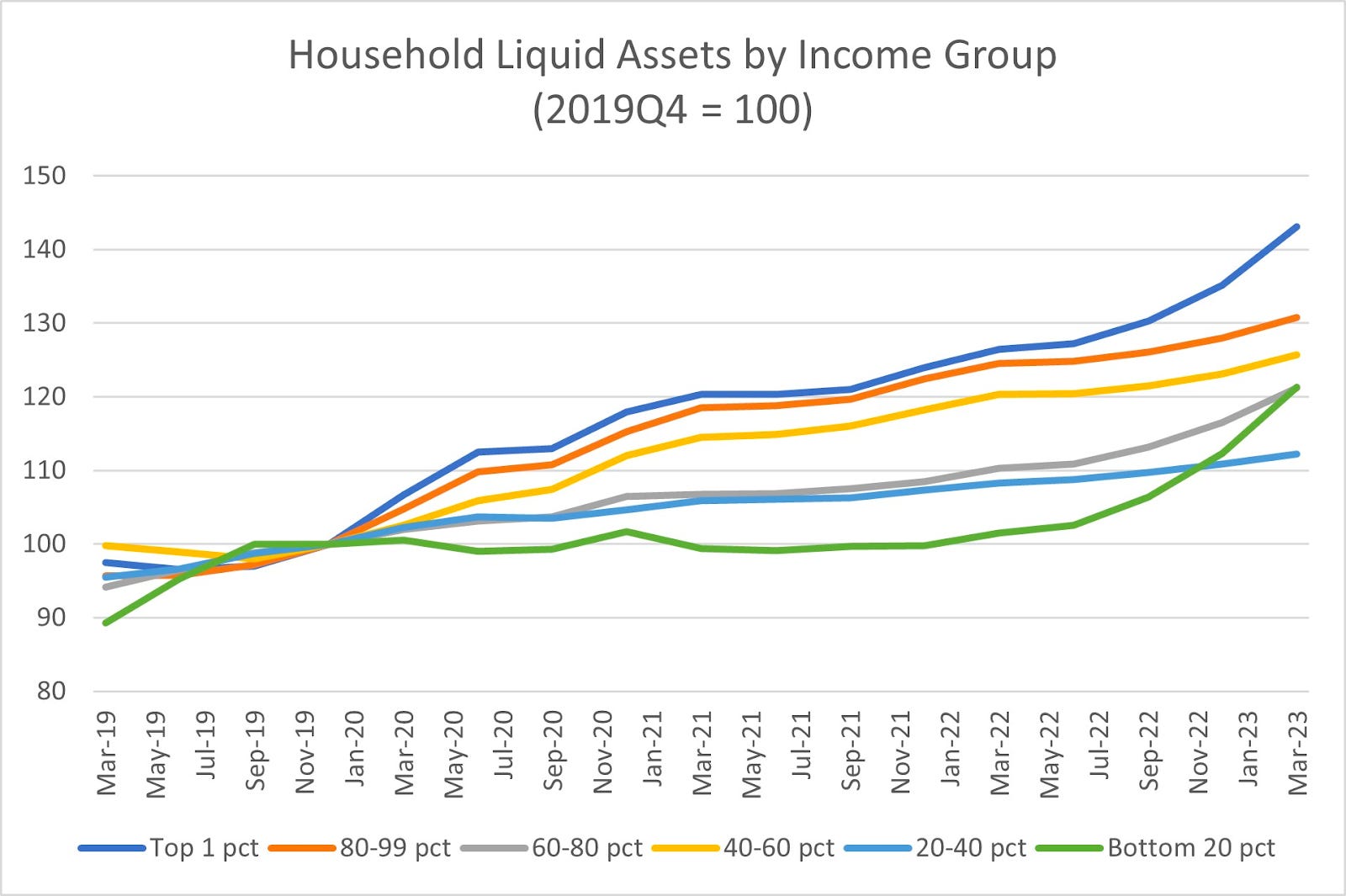

On June 16, the Federal Reserve Board of Governors released the latest Distributional Financial Accounts, where we find that household liquid assets (a measure of savings) generally remain elevated compared to pre-pandemic levels, but levels and trajectories differ across income categories.

Liquid asset is the component of household net worth that can be easily converted to cash. It is the sum of deposits, government and municipal securities and money market fund shares .

The chart below shows nominal liquid assets by household income groups (normalized to equal 100 in Q4 2019 as a pre-pandemic baseline). Across the income distribution, liquid assets have increased relative to the pre-pandemic baseline. The largest increase accrued to the top 1% of households, where liquid assets are up more than 40% versus the pre-pandemic baseline. Lower and middle-income households (the 20th to 40th percentile of households) have seen liquid assets rise by 10% since the start of the pandemic.

Going one level deeper, when we look at the savings rate (liquid assets to income ratio) across income groups, we can see that the savings rate increased from 11.4% in Q4 2019 to 12.2% in Q1 2023 for the upper-income households. For households with income in the upper-middle range, the savings rate has stayed around the same at 5.3%. On the other hand, lower-middle-income households and lower-income households have seen their savings rate fall from the pre-pandemic levels of 4.6% to 4.2%.

This indicates that while the tailwind of excess consumer savings from the pandemic era is mostly over, it is the lower to middle income households that have truly felt the brunt of inflation and high interest rates over the past year and a half, as they had to rapidly drawdown on their savings, indicated by the decline in their savings rate to fund the rising cost of living expenses.

At the same time, consumers also tapped into credit card debt, which sits at an all time high. In the next section, we take a look at the growth rate of household debt and interest payments relative to disposable personal income to see whether the rising debt level poses an immediate threat to the overall consumer well-being.

3. As household debt rises to record levels, will the US consumer be able to pay it back?

The prominent role consumers play in the US economy is one of the primary reasons why we should pay close attention to the state of household debt. In Q2 2023, total household debt in the US reached a record high of $17.06T. This represents a 5.6% increase on a year-on-year basis.

A quick primer on household debt

Total household debt consists of housing debt (70%) and non-housing debt (30%). Housing debt covers mortgages, while non-housing debt covers auto loans, student loans and credit card balances.

While housing debt has grown 20% since the 2008 Great Financial Crisis, non-housing debt has grown 75% during the same time period. The post GFC era, which was marked by low interest rates, was one of the reasons for the rapid increase in non-housing debt, whereas the housing market was still recovering from the shock during this period of time.

The rising credit card debt amongst US households, especially for the lower-income segment

According to Rob Haworth, senior investment strategy director at the US Bank Wealth Management, consumers started 2022 in a strong financial position, since consumer debt was low, savings were high and peoples’ wages were rising. But Haworth said that by the end of 2022, the environment had changed, as consumer borrowing rose meaningfully, mostly in the form of unsecured revolving credit.

Total credit card debt topped $1T for the first time ever in Q2 2023, which had grown 16.2% on a year-on-year basis.

Remember, credit card debt is part of the non-housing debt portion of the overall household debt.

In fact, the latest reading on average credit card balances across income groups by Bank of America in August 2023, suggested that credit card balances for the middle and higher income households are at levels equivalent to that in 2019. However, credit card balances for the lower-income households have seen a steeper rise and have exceeded the pre-pandemic range.

This further validates what we saw earlier with savings depleting at the fastest rate for the low to middle income households as they face the brunt of high inflation and high rates. So, not only is this segment depleting savings at the fastest rate, they are also increasingly tapping into credit card debt.

With the upward trend in household debt, the question arises as to whether the people (who are borrowing money) are in a position to pay it back.

Let’s put the “record” household debt into perspective

One of the metrics to assess whether household debt is growing faster than wages, is to look at the household debt service payments in relation to disposable personal income.

From the chart below, you can see that household debt service payments represent 9.8% of disposable personal income. This level is in line with the pre-pandemic levels and far below the 2008 Great Financial Crisis highs, where household debt service payments reached 13% of disposable personal income.

Generally, this would be a positive sign, suggesting that while the consumer is borrowing, they are not doing so at a rate faster than wage growth. If they did borrow at a rate faster than the rate of wage growth, debt service payments as a percentage of disposable personal income would go up, and clearly, that is not what is happening today.

But, before we take our guards off, I want to bring your attention to the individual components of the household debt once again. Remember, household debt consists of mortgage and non-mortgage debt. While mortgage debt service payments as a percentage of disposable income stands at 4% in Q2 2023, a level that is not alarming, non-mortgage debt, a.k.a consumer debt service payments (which consists of debt service payments for auto loans, student loans and credit card debt) is growing at a rate of 8.5% on a year-on-year basis.

In the meantime, non-mortgage debt service payments represent 5.8% of disposable personal income today, and the number is growing. This is an indication of the pain that is inflicted from rising interest rates on people who need to borrow in order to buy goods and services.

As long as consumer debt service payments relative to disposable personal income grows, we can expect the US consumer to get further squeezed and slow down spending, unless, of course, income starts to grow at a faster rate. Worse, if the labor market weakens materially, followed by a drop in income levels, default risk would rise as the US consumers won’t be able to pay back the debt.

Given the current figures, disposable personal income would need to drop by 20% or more, in order for debt service payments relative to personal income to rise to the 2008 GFC level. That is quite a bit of cushion.

However, should a recession happen, a drop of 20% in income levels is not unprecedented. In such a circumstance, we would see consumer loans default. While the consumer loan delinquency rates are not at alarming levels today, credit card delinquency rates are stand at 2.77% and climbing. Something to watch out for!

Closing thoughts!!!

For now, the US economy is not in a recession, nominal consumer spending is strong and the labor market is resilient. The Fed continues to share a bright outlook for the economy. But things could aggressively turn in the opposite direction, as 69% of US consumers and 84% of US CEOs are preparing for a recession.

Looking forward, I am going to monitor the state of the labor market, the volume of revolving credit relative to disposable personal income and the overall sentiment to assess the evolving health of the US consumer. For now, though the US consumer may seem healthy, it is time to start taking precautions before a possible cold sets in.

You rock!!

It's impressive that you always come up with high quality content 4 times per week. Thanks for your time and dedication!