AI Still Pays The Bills For Silicon

Broadcom & Credo vs. AMD, Nvidia & the whole AI Networking Space

At The Pragmatic Optimist, we help hundreds of investors navigate the evolving AI innovation landscape, identify rock-solid businesses with strong growth trajectories and operational grit, and make long-term investments in the space with proven alpha generating returns.

Become a paid subscriber today

This isn’t the first time Broadcom’s AVGO 0.00%↑ Hock Tan rattled markets with his gravity-defying projections for the AI beneficiary that Broadcom has become.

Just like their Q4 FY24 ER in December last year, Broadcom’s Q3 FY25 ER published last week led to another boisterous rally in the custom silicon leader’s shares on Friday, adding an extra $200B to Broadcom’s market cap.

Broadcom's Q3 FY25 report was another one for the ages that had analysts lining up for more juicy details about how much higher Broadcom could aim beyond the 60% CAGR in their AI revenue. Post Broadcom’s results, markets were quick to react, with some names rising and others crashing on Friday. (Remember Ben Graham's “voting machine” quote…?)

But many have overlooked details such as OpenAI’s massive 100%+ cash burn projections issued last week, while some may have even forgotten the targets that AMD AMD 0.00%↑ and Nvidia NVDA 0.00%↑ had set for themselves in the last few weeks. As a result, we believe this will require some reframing in the big picture for AI, which we discuss below.

In addition, we have also conducted deep dives on Broadcom’s Q3 and Credo’s Q1 ERs, while updating our PTs on some other winners from the AI infrastructure and networking space we had called earlier this year.

Note, you can find our updated price targets, conviction score and ratings history on all stocks under our coverage in the AI Stock Rec Tracker below.👇

Robust Progress On Our AI Networking Thesis

In March this year, we had sent out a deep dive about how underrated the AI Networking sector was and issued a deep dive to help investors get up to speed. We even followed up that thesis with initiating a position in Celestica CLS 0.00%↑ which has turned out to be our best call so far for this year.

Others like Credo CRDO 0.00%↑, Astera Labs ALAB 0.00%↑, Arista Networks ANET 0.00%↑ have also spectacularly rallied, while our consistently neutral thesis on Marvell MRVL 0.00%↑ has been spot on.

The short version of our updated thesis about AI Networking: AI is still more than happy to pay the bills for silicon and networking.

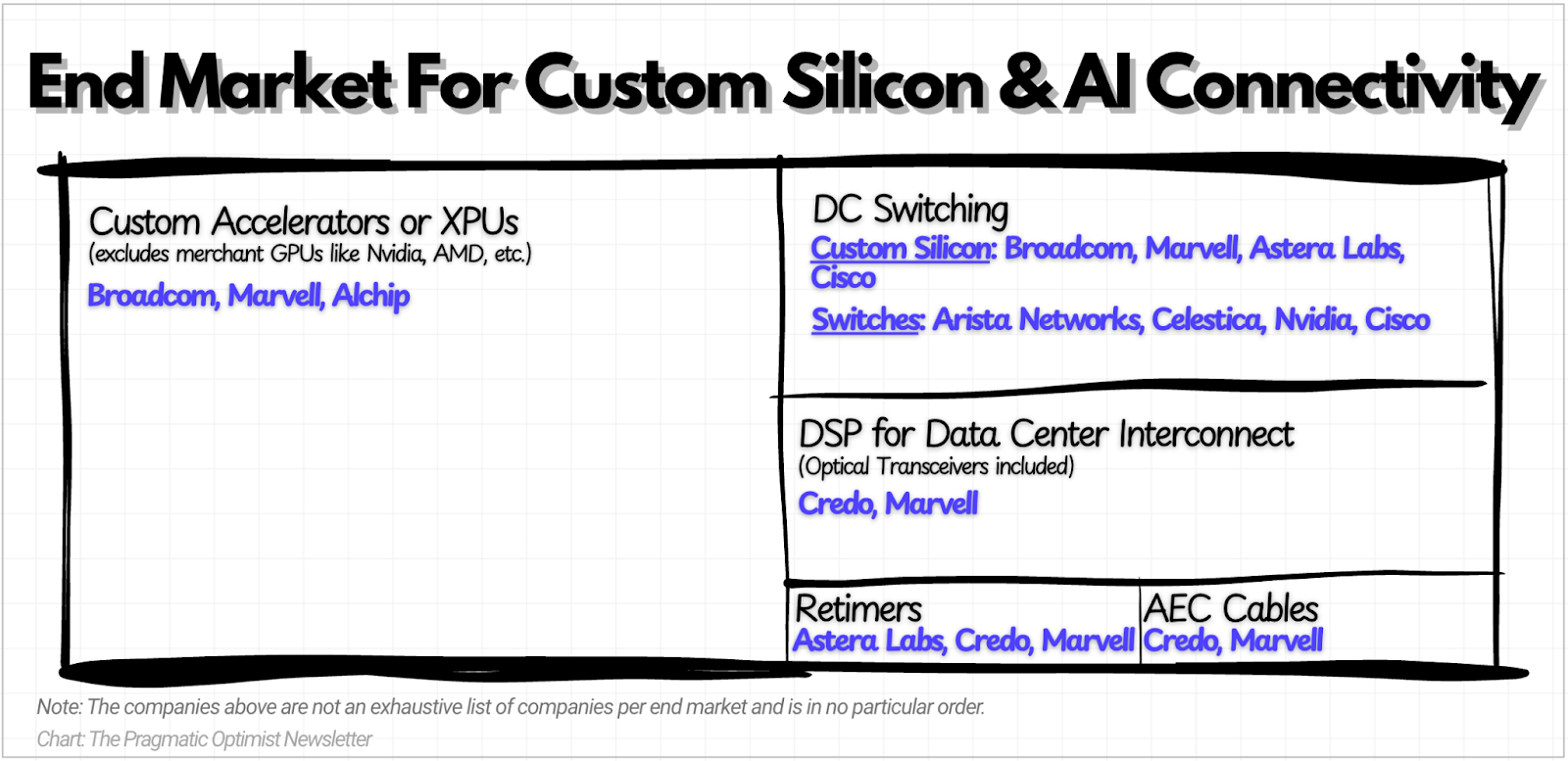

Our average growth rates for each category of the DC (data center) market for custom silicon and AI networking are still mostly unchanged for now since our March report, where it is expected to be growing at ~$100B/year through CY28.

Of that number, AI ASICs alone account for roughly half that ~$100B/year growth rate, while AI Networking accounts for the rest—DC Switching growing at $45B+, DSP IC business across DC interconnect driving $10B+ in optical transceiver revenue, Retimers at $1B+, and AECs at $1B+. We’ve doodled a little chart for you all that helps illustrate who all the players in these different end markets are.

(Remember: the companies named below are not an exhaustive list & are in no particular order.)

Some of these end markets are expected to grow at 50-70% growth rates, while others are projected to grow approximately >2x over this time period.

We suspect that Broadcom’s Q3 ER and Credo’s Q1 ER from last week may have pulled forward some of those growth rates while competition heats up between hyperscalers, neoclouds, and AI hypergrowth startups.

In the section below for our paid members, we detail OpenAI’s massive capex budget ramp-up that was revealed at the end of last week and how that impacts the price targets for Broadcom, AMD, and Nvidia.