A bond market meltdown to a soft landing- Is the US economy slowing down faster than anticipated?

Economic data & company earnings point to a slowdown in the US economy, yet the labor market is strong & US households sit at record net worth. The dilemma for the Fed grows stronger.

««The 2-minute version»»

Background: The US economy went from an inflation panic mode to a soft-landing mode in less than 2 months. A series of economic reports coming in since last week has instilled renewed optimism that inflation in the US economy may have peaked, as the volatility in long duration bonds has cooled down since then and S&P 500 has come roaring back.

The data that points to a slowdown:

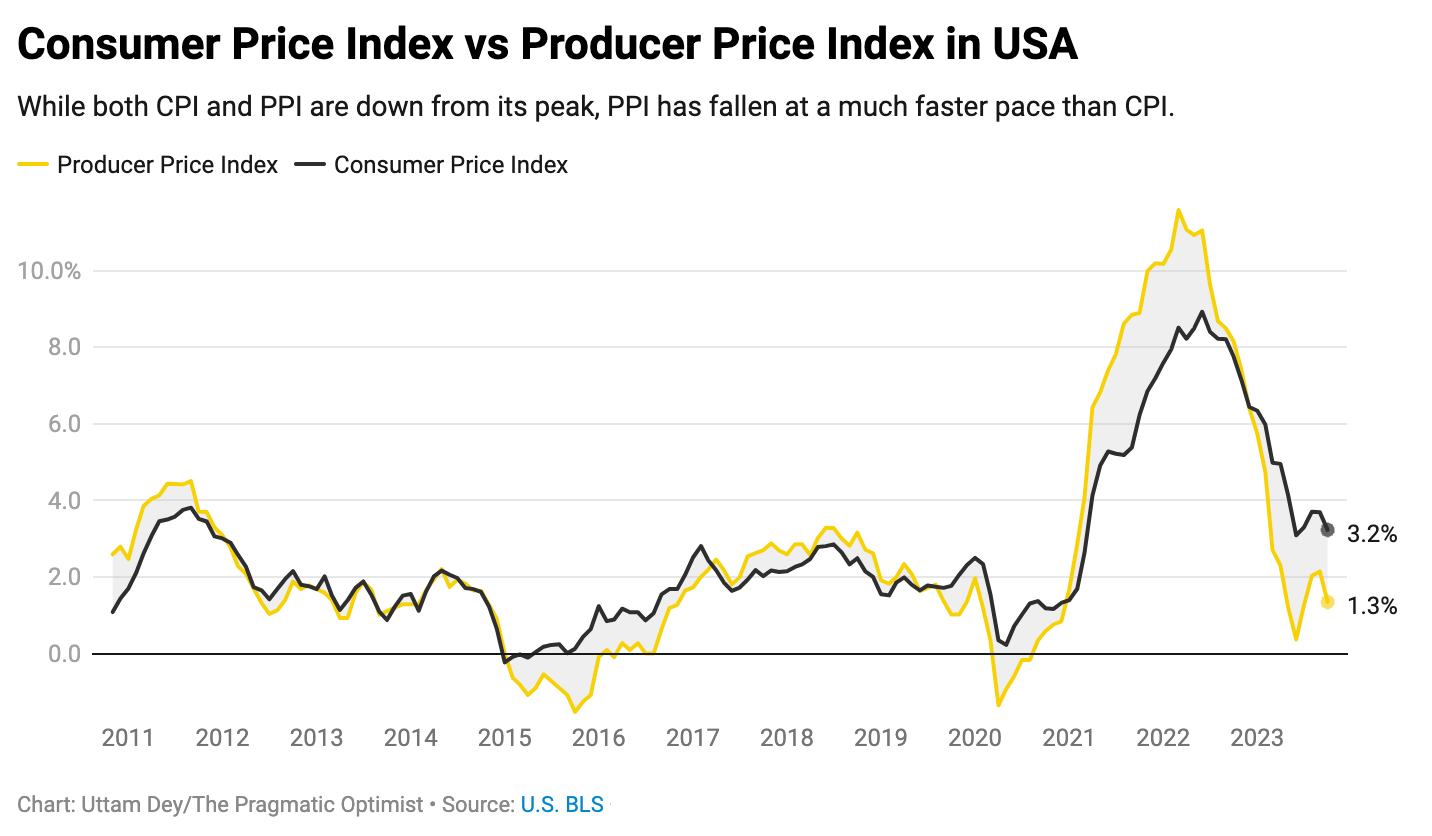

On the inflation front, both consumer and producer prices are growing at levels lower than expected.

The housing market is also looking pretty gloomy as NAHB Housing Market Index fell 6 points MoM and is back to December 2022 levels.

Meanwhile Real Retail Sales and Industrial Production are declining on a YoY basis.

But it’s not that straightforward: While there are signs of slowdown, there are indicators that would caution Fed against loosening too quickly.

The labor market is still strong and wages are still growing at an elevated level.

As a result, consumer spending expectations remain higher than average.

The net worth of households in the US sit at all all time high of $155T.

What others are saying: Goldman Sachs and Ed Yardeni of Yardeni Research are optimistic of a soft-landing scenario, while Cathie Wood believes that the Fed has already done a lot of damage and a possible deflationary bust is underway. Meanwhile, CEOs of Walmart, Target and Home Depot sound cautious on their Q3 earnings call, as they point to slowdown in consumer demand affecting holiday sales.

The Pragmatic Optimist’s final word: While liquidity is flat, reverse repos are getting drawn out quickly. Meanwhile, there are early signs that bank lending standards maybe starting to loosen from peak tightening, which usually marks the bottom for the stock market. However, given the unusual nature of large fiscal deficits, determining long-term direction of equities is challenging. In my view, I expect sideways choppy price action with a very wide volatility band.

On Sep 20, 2023, when the Federal Reserve released their US economic projections, the bond market had a meltdown. The Fed projected that the US economy would remain stronger for longer, and as a result, it guided for interest rates to remain anchored for longer.

Bond investors aggressively sold off long duration bonds in anticipation of higher inflation and interest rates than previously anticipated. Such a degree of volatility led to a sharp bear steepening in the bond yield curve where the spread between the 2Y and 10Y US Treasury bond narrowed from (77)bps to (20)bps The equity markets also sold off as bond yields climbed, making equities look less favorable as compared to risk-free assets.

Yet, after a series of softer than expected economic reports over the last 1 month, there is a growing narrative that inflation in the US economy may have peaked. Especially after last week, there is a renewed confidence that not only has the US inflation peaked, but we may be heading for a soft landing after all.

It took less than 2 months for the economic narrative to swing from one extreme to the other. Not to mention, the S&P500 came back roaring climbing 2.5% over the last week.

My goal with this post is to weave together the data from macroeconomics, consumer & business surveys, company earnings and more to understand the “big picture". Therefore, in this post, we will do the following:

Establish what “soft” and “hard” landing actually means.

Provide an overview of key data prints that point to a slowing US economy vs. data that showcases that the US economy is doing just fine.

Listen to what Goldman Sachs, Cathie Wood, Ed Yardeni and CEOs at Walmart, Target and Home Depot have to say about the US economy?

Outline what I make of this all?

Let’s get started 👇🏼👇🏼👇🏼

1. “Soft” vs. “Hard” Landing. Let’s demystify Wall Street lingo.

😇 Soft landing

The general idea behind the soft landing narrative is that the Fed’s rate hikes have cooled the economy enough, where consumers have slowed spending as inflation falls, but not so much that it hurts company earnings and employment.

Under the soft landing premise, company earnings will come at or above expectation for the remainder of 2023 and into 2024. Proponents of the soft landing camp would also project that the Fed stop hiking interest rates and possibly lower rates soon enough in order to fuel the next stage of economic expansion.

All of this must take place without a recession.

👿 Hard landing

On the other hand, the hard landing narrative is built on the belief system that the Fed needs to keep interest rates higher for longer, as consumer spending and company earnings strength continues.

Under this premise, as interest rates are kept higher for longer, the cost of borrowing for consumers and businesses remains high. Ultimately, this will lead to weaker consumer spending, wobbly company earnings and possibly broad credit events (in the form of bankruptcies), which results in a recession.

2. Are we heading for a slowdown? All the data that supports the claim

Inflation continued its broad moderation in October, down from its pandemic-era highs that hadn’t been seen in more than 40 years. Overall consumer price inflation did not increase month-over-month and currently is up 3.2% on a year-over-year basis.

In fact, digging one level deeper, we can see consumer price inflation for durable goods is in “deflationary territory” declining (2.1)% on a year-over-year basis. Meanwhile consumer price inflation for non-durable goods and services rose 1.7% and 5.5% respectively on a year-over-year basis.

At the same time, wholesale prices in October also posted their biggest decline in over 3 years, providing another indication that the worst of the inflation surge may have passed. The producer-price index, which measured the final-demand input costs for businesses declined (0.5)% for the month, against expectations for a 0.1% increase. On a YoY (year-over-year) basis, headline PPI increased 1.3%.

Plus, retail sales in the USA declined (0.2)% MoM (month-over-month) in October 2023, putting an end to a 6-month streak of increases. It however declined slightly slower than market consensus of (0.3)% decline. While retail sales is still growing at 1.6% on a YoY basis, Real Retail sales, which adjusts for inflation, is now down (0.7)% on a YoY basis.

The housing market is also turning gloomy based on this week's NAHB/Wells Fargo Housing Market Index survey results. The survey is designed to take the pulse of the single-family housing market. The survey asks respondents to rate market conditions for the sale of new homes at the present time and in the next 6 months as well as the traffic of prospective buyers of new homes.

The NAHB index declined by 6 points to reach 34 in November 2023, significantly below the market’s expected level of 40. This marks the 4th consecutive month of declines, bringing the index to its lowest point since December 2022, due to the substantial impact of high mortgage rates on both builder confidence and consumer demand.

Finally, industrial production also declined more than expected in October, as auto workers' strikes continue to exert downward pressure on a range of market groups. US industrial production fell (0.6)% in October from a revised 0.1% rise in September.

Manufacturing output also declined by 0.7% in Q3, which was dragged down by a 10% drop in the output of motor vehicles and parts that was affected by strikes at several manufacturers of motor vehicles.

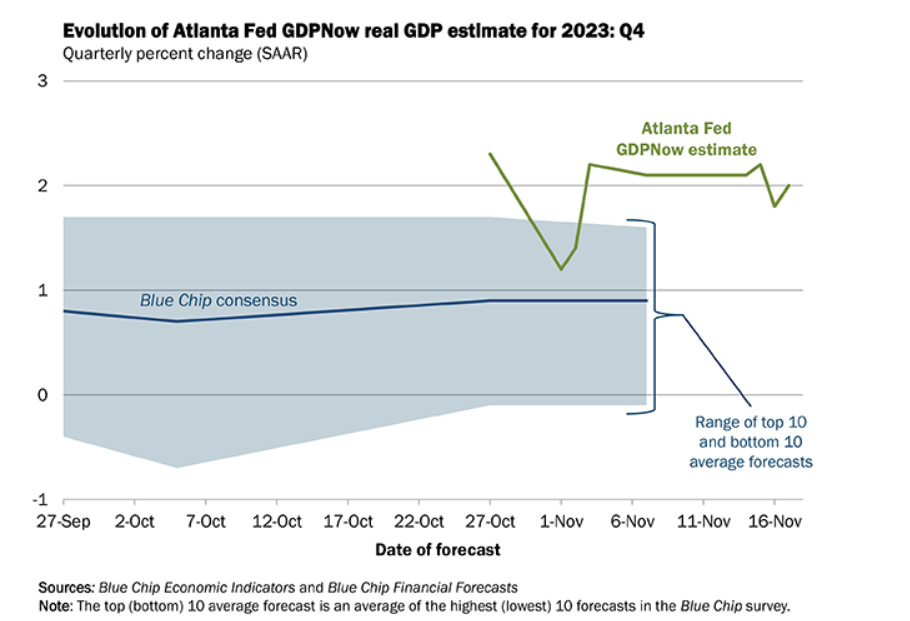

On the back of weaker than expected economic data, the Atlanta Fed GDPNow model estimates for real GDP for Q4 2023 to grow at 2.0%, as of the latest reading on November 17. This down from a previous forecast of real GDP growth rate of 2.2% on November 15th.

3. Yet, there are indicators that cautions the Fed not to take off its guards just yet

While overall inflation and spending has come down since the Fed started tightening interest rates, the long term inflation and spending expectation are still at elevated levels as per New York Fed Survey.

Consumers believe that inflation will likely be 3.6% one year ahead and 2.7% over the next 5 years. But, what is slightly more worrisome is household spending growth expectation which stands at 5.3%, well above the long-term trend.

Remember if household spending grows at 5.3%, where consumer spending accounts for 70% of GDP, it is very difficult to attain an inflation rate of 2.2% unless we experience an exponential surge in productivity.

The confidence in household spending is driven by the strength in the labor market, where non-farm payrolls is still growing at 1.9% and hourly wages that are growing at 4.1% YoY. In fact, according to the Atlanta Fed wage growth tracker, wages are growing on a 3-month moving average rate of 5.2%, higher than what the labor report states.

In fact, job switchers continue to receive higher wages compared to job-stayers, though the gap has narrowed from its peaks earlier on.

Finally, the total household net worth of US stands at all time high of $155T, which. There is no denying, that a large portion of the net worth has accumulated to the upper middle class and the wealthy, as we have already seen households in lower to middle income families deplete their savings and tap into credit card debt.

Please note that the upper middle and wealthy segment of the society tend to benefit from higher interest rates as they have savings that produce net interest income. Plus, there is a higher likelihood that this segment of individuals already owned their homes from before, which means that they have either locked in lower rates or are completely mortgage free, allowing them more spending power.

4. What are portfolio managers & industry CEOs saying?

On the soft landing side, Goldman Sachs forecasts that the US economy is expected to outpace other developed markets with estimated growth of 2.1%. Goldman also believes that the bulk of the drag from monetary and fiscal tightening policies is over. While they hold the view that US real income growth is set to slow from its 2023 pace of 4%, it is still purported to support consumption and GDP growth of at least 2%.

“We continue to see only limited recession risk and reaffirm our 15% US recession probability,” Hatzius said in the outlook report.

Echoing Goldman Sachs is Ed Yardeni of Yardeni Research, who also believes that given the net worth of US households stand at $150T and half of that is held by baby boomers, they are likely to continue spending at a higher rate. Going into 2024, Ed Yardeni believes it will be a growth year, as consumers will see employment gains and real wage growth as inflation continues to decline, driven by a productivity surge.

On the other side of the fence is Cathie Wood who believes that deflation is already underway in the US across industries, which will force the Federal Reserve to kick off a big interest-rate cutting cycle.

“The Federal Reserve has overdone it, we’re going to see a lot more deflation going forward. If we’re right, and they’ve gone way too far, they’ll have to cut fairly significantly,” Cathie Wood, Head of Ark Investment Management said on Bloomberg.

Wood has long expected an era of falling prices, backed by emerging technologies including artificial intelligence, electric vehicles, robotics, genomic sequencing and blockchain. She has also criticized the Fed, saying its aggressive interest-rate hikes could increase the risks of a deflationary bust.

Meanwhile, we also saw large US consumer retailers report their Q3 earnings last week. Among them, Walmart CEO Doug McMillion said that the US food industry may be heading into a period of deflation after 3 years of punishing price hikes that have caused sticker shocker for shoppers at the grocery store.

“We may see dry grocery and consumables start to deflate in the coming weeks and months,” McMillon said. Walmart could enter “a deflationary environment.”

In a separate interview with CNBC, Chief Financial Officer of Walmart, John David Rainey said consumers are “leaning heavily” into major promotions as they watch their spending and search for deals. While Walmart WMT 0.00%↑ has beat earnings and revenue estimates for Q3, it has pulled back its Q4 earnings guidance, as management has become cautious about the outlook on consumer spending moving forward.

Target TGT 0.00%↑ which also reported its Q3 earnings forecasted a weak holiday season this year, as consumers continue to forgo discretionary purchases like furniture, electronics and clothing.

Finally, the home improvement retailer, Home Depot HD 0.00%↑ which beat revenue and earnings expectations has also sounded the alarm on its outlook for consumer spending as it narrowed its full-year outlook.

“A customer who might have remodeled their entire home may be opting for a partial remodel,” Home Depot’s CFO Richard McPhail said. “Maybe they won’t redo their entire kitchen. Maybe they’ll just do the countertop and backsplash. And so it’s really just the downscaling of projects that we’ve seen.”

Still, he said Home Depot’s customers are in good shape financially.

“The consumer — and particularly the homeowning consumer who is our customer — is healthy,” he said. “They’re employed. They’ve seen income gains and wealth gains in recent years. They have excess savings and they remain engaged in home improvement.”

5. What to make of it all?

On one hand, there is reliable evidence that economic growth in the US is slowing down, thanks to a tight monetary policy that has slowed down consumer spending, industrial production, housing activity and overall inflation.

On the other hand, the labor market and wage growth continues to be strong. And consumers’ spending expectation remains to be above elevated levels.

Therefore, it creates a paradox for the Fed to solve and optimize for given its set of mandates and the monetary tools at its disposal.

On one hand, the Fed can keep rates at current levels and wait for further data prints in the coming months to decide on the next steps. This would continue to squeeze the private sector and slow the economy even more, while bringing inflation down further. Doing this, the Fed is going to be protecting the economy from future inflation surprises. But at the same time, it also risks tipping the economy into a recession a.k.a The Hard Landing, should spending fall much faster than expected, a liquidity crisis transpires in the repo market or a series of bankruptcies erupt as debt comes due.

On the other hand, should the Fed start winding down its Quantitative Tightening and lowering interest rates given the current set of economic data, it could spur the next leg of economic growth and expansion as it will reduce the cost of borrowing for households and businesses. Thus, we will likely see a pick up in bank lending and private credit growth. However, given the current state of the labor market and level of government spending, it risks inciting the next leg of inflation soon after, unless it is accompanied by a faster growth in productivity.

As of the last FOMC meeting, the Fed has decided to pause interest rates for the moment. The Fed indicated that the sharp rise in long duration bond yields was doing some of the Fed’s tightening for it, which gives the Fed more time to wait and assess incoming data.

Objectively, we know that the overall state of liquidity in the US is more or less flat, driven by the drawdown in reverse repos as the US Treasury issues more T-bills, as there isn’t much demand for longer-duration bonds. The reverse repo facility is currently under $1T for the first time since 2021. The ongoing drawdown of the reverse repo facility is putting liquidity back into the system. However, once the reverse repo facility runs out, liquidity problems could become pretty severe and require a change of course by the Fed.

Finally, Senior Loan Officer Surveys for Q3 2023 showed that banks across the board, are easing up on their tightening of credit standards for the first time in a while. Historically, the peak in credit tightening standards have corresponded to market bottoms in the past.

Ultimately, I continue to be less bullish than many of the bulls, but less bearish than most of the bears. I believe that large fiscal deficits have created an unusual environment for the Fed’s policies to effectively work. Therefore, determining the general long-term direction of equities will be challenging in the coming decade. In my view, I expect sideways choppy price action with a very wide volatility band.

Love your 2-minute version so readers get the gist nicely! Let us also appreciate your header picture - how fun and creative!!

I think whether the Fed hold further or cut interest rates, long bond yield may still stay high given bond and inflation Nd supply risk premium all have come back. So long rates are the key to watch for the health of the rest of the economy!

Excellent read. Looks to me like the Fed has lost control of it. Too many large company insiders selling significant amounts of their personal stock.