I built an Economic Scenario Map to guide me through key economic outcomes for the US. Here’s how you can use it.

Building a US Economic scenario map, a tale of two markets and a summary of macroeconomic indicators

Welcome to my first post. In this post, I will present to you my US Economic Scenario Map, that I had built out for my investment fund.

I use this map as a guiding framework to assess the trend of the leading and lagging economic indicators, connect them together to lay out key scenarios that may play out for the US economy and use the insights to drive my investment decisions.

But first, let’s provide some context.

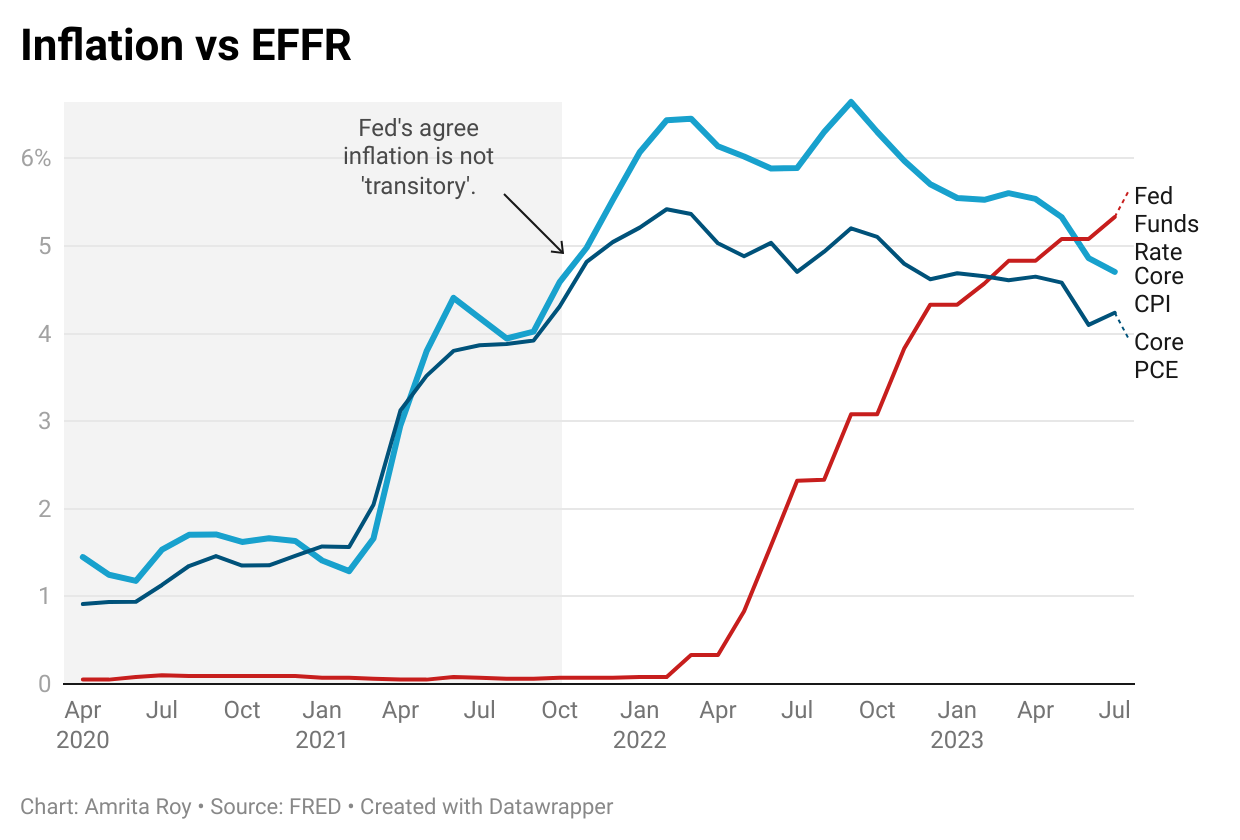

Inflation in the USA spiked to its highest level at 5.4% in February 2022 . The Fed's effective funds rate was at 0%.

The Fed believed with a high degree of conviction that inflation was transitory, driven by post Covid supply chain constraints.

Come November 2021. Core Inflation prints continued to surprise on the upside.

The Fed stepped in. Since then, they have hiked interest rates 11 times to a target range of 5.25-5.5%, the highest level in 22 years. In addition, they have reduced their balance sheet to its lowest level in two years, as they rolled off $960 billion of bonds since June 2022.

As of Friday August 25th at the Jackson Hole Economic Symposium, Fed Chair Powell called for more vigilance in the fight against inflation and warned that additional interest rate increases could be yet to come. He also reinstated that the inflation target would be kept at 2%.

Second, let’s take a look at some of the progress we have made since the tightening cycle began.

Key Observations

The Good: Since the tightening cycle began, we can see that indicators across Spending, Production, Employment and Income have come down from its peak and trending lower. (This slowdown was much necessary from the peak in order to re-establish price stability, consumer confidence and long term economic growth).

The Worrisome:

Indicators such as Core Inflation is still higher than Fed’s 2023 projection of 3.9% and long term projection at 2.2%.

While Manufacturing activity has slowed into contraction territory, Services activity is still strong and growing above 50%

Job Openings per Unemployed person still remains at an elevated level which keeps the labor market tight and wage pressures up.

Average Hourly Earnings is still growing at a rate of 4.3% on an annual basis, a level inconsistent with the long term inflation target of 2.2%.

This dilemma has given rise to 2 contradictory economic narratives in the market.

Narrative 1: The Soft Landing camp

Fed’s rate hikes have cooled the economy enough where consumers have slowed spending as Core Inflation falls, but not so much so that it hurts company earnings and employment.

Company earnings continue to surprise on the upside in 2023.

The Fed should stop hiking rates and possibly start to lower rates in order to fuel the next stage of economic expansion.

Narrative 2: The Hard Landing camp

The Fed needs to keep rates higher for longer, as consumer resilience and company earnings strength continues.

As a result, the cost of borrowing for consumers and businesses will remain higher for longer.

This will end in some form of a credit event, which will cause an earnings recession and higher than expected job losses.

So, how do I decide which camp I should belong to?

🥁 🥁 🥁 Enter the US Economic Scenario Map

Instead of mindlessly jumping from one narrative to the other every week based on noise, I take a framework driven approach to building key economic scenarios that may play out in the US.

In this post, I will

a) explain the approach to The Economic Scenario Map

b) describe the key scenarios that I have outlined in the map

c) walk you through how to use the map as a guide on your investment journey.

The Approach

The Economic Scenario Map framework is divided into 2 categories.

Growth Outlook

Inflation Outlook

The Growth Outlook has 2 possible outcomes:

Economic Expansion: Real GDP >0%

Economic Recession: Real GDP <0%

The Inflation Outlook has 4 possible outcomes:

Disinflation: Core Inflation trends to 2.2%

Deflation: Core Inflation trends lower than 2.2%

High Inflation: Core Inflation is higher than 2.2% and Fed's 2023 target of 3.9%, but showing evidence of slowing down.

Hyperinflation: Core Inflation trends higher over Fed's 2023 target of 3.9%

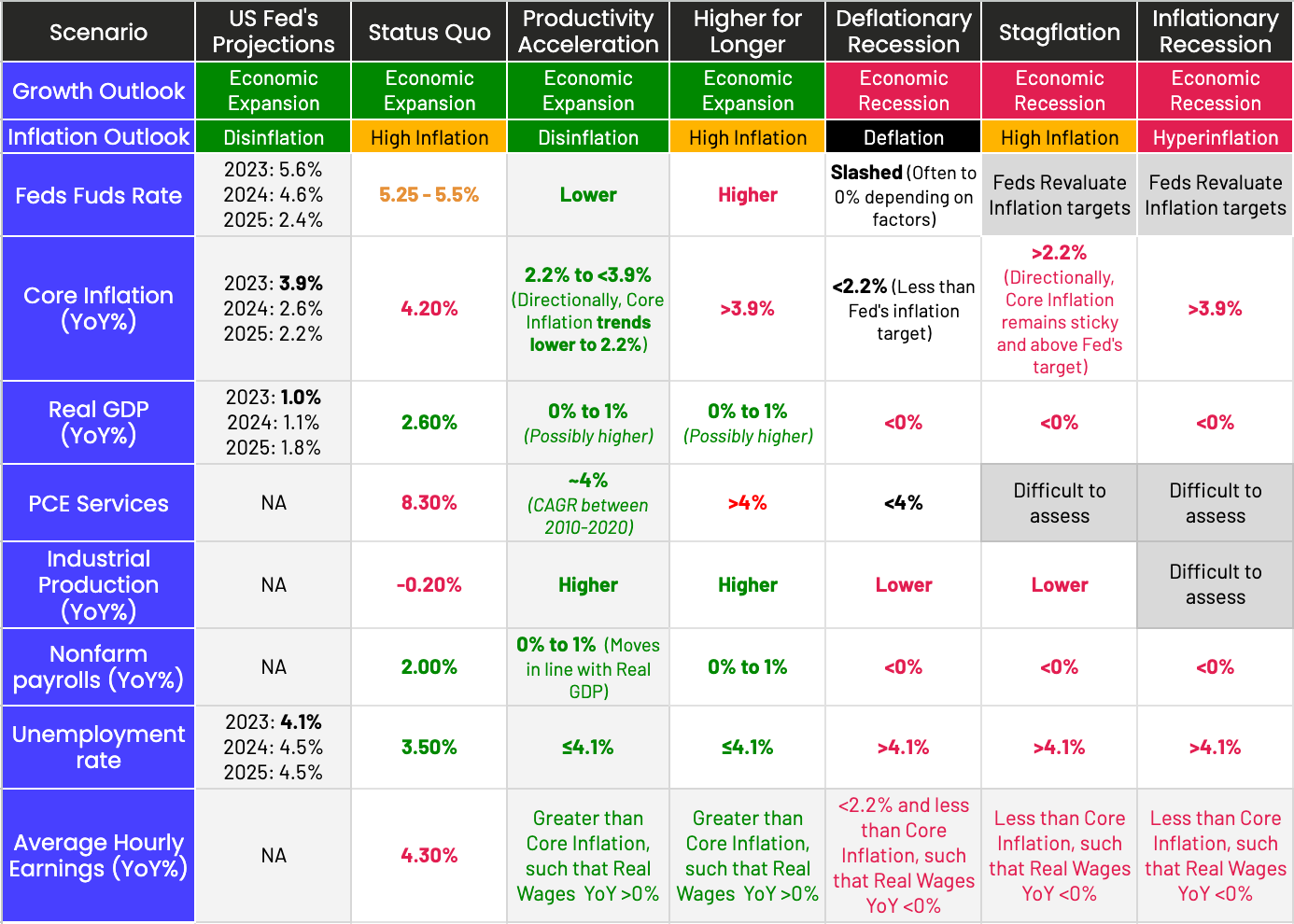

Combine the Growth and Inflation outlook and it gives rise to 6 possible scenarios that may play out in the US economy.

For each scenario, I have outlined the direction of key indicators across Spending, Production, Employment and Income that will act as a guide to knowing which scenarios have a higher probability of playing out.

Presenting the Scenarios + how to read the data to assess the likelihood of the future scenario

The Economic Expansion club has 3 scenarios.

Status quo: This is where we currently stand from an economic perspective. In this scenario, with the current FF Rate at 5.25-5.5%, we have,

Core Inflation YoY = 4.2%. It is trending lower but still higher than Fed’s 2023 target of 3.9% and long term target of 2.2%

Services Inflation YoY = 8.3%. It is trending lower, but higher than its long term growth rate. On a 3 Month Annualized basis, it is growing at 5.4%, which is still higher than the long term growth rate. Therefore, it would be safe to assume, that we would need to have tightening for longer in order for Services Inflation to come to a level where Core Inflation trends towards Fed’s 2023 and long term target.

Non Farm Payroll YoY = 2.0%. Non farm payroll grows in line with Real GDP, and as a result, we see Real GDP growing at a rate of 2.6%.

Unemployment Rate = 3.5%. Unemployment is at level often considered as “full employment”. As a result, it can be assumed that the labor market is tight.

Average Hourly Earnings YoY = 4.3%. Given the growth in Non farm payrolls and tight labor market, average hourly earnings is growing at 4.3%, which is higher than average. Most importantly, it is growing at a level where Core Inflation is unlikely to come down to the 2.2%.

Given the direction of the economic data so far, I would place Higher for Longer and/or Stagflation to be the most likely outcomes of all the economic scenarios so far.

Productivity Acceleration: In this scenario, we will observe that

Core Inflation YoY will drop to the Fed’s 2023 target of 3.9% and continue to head lower to 2.2%, while Real GDP remains positive.

This will be played out by Services Inflation slowing down to annualized growth rate of 4%.

Industrial Production will likely pick up from current levels.

Non farm payrolls will slow down along with Real GDP growth, but remain positive. This will be reflected in Unemployment rate going up from current levels but not exceeding 4.1%. As labor market conditions loosen, Average Hourly earnings will grow at a slower pace, but above Core Inflation levels to maintain positive Real Wages.

Depending on the rate of slowdown, the Fed would most likely choose to lower rates in order to spur the next phase of economic expansion.

This is the soft landing scenario. Given the current direction of data, this scenario remains a small possibility, but lower in probability than higher for longer and stagflation.

Higher for longer: In this scenario, we will observe that

Core Inflation remains at elevated levels at or slightly above 3.9%. While it may show signs of slowdown or stability, it is not coming down to the Fed’s long term target of 2.2%. In the meantime, Real GDP remains positive.

This will be reflected in Services Inflation which will also remain stubbornly high above long term growth rate of 4%.

Non Farm payroll will continue to grow at the rate of Real GDP, as a result, we may not see much of an uptick in unemployment rate.

Average Hourly earnings will continue to trend over Core Inflation to reflect positive Real Wages.

This will cause the Fed to once again raise FF rate from current levels, which will be repriced in the bond and equity markets.

The Economic Recession has 3 possible scenarios.

A Deflationary Recession: This scenario is similar to the Global Financial Crisis. In this scenario, we will observe that

Core Inflation YoY drops abruptly below 2.2%

This will be fueled by a sharp drop in Non farm payrolls declining on an annualized basis, causing a sharp rise in Unemployment Rate over 4.1%

With Job Openings falling and Unemployment level rising, Average Hourly Earnings will see a sharp drop too, and below the rate of Core Inflation, thus producing negative Real wages.

This will cause spending in services to fall sharply, and thus Core Inflation will continue to drop in a reverse flywheel unless the Fed steps in.

The Fed would likely slash rates to 0% to re-stabilize the economy. This scenario can be fueled by a credit event, that results in sharp declines in company declines and rise in layoffs.

While there are evidence of cracks in the system, especially with the mini banking crisis in early 2023, I would not assign a high probability to this scenario to play out next, given the current direction of macroeconomic data.

Stagflation: In this scenario, we will observe that,

Core Inflation YoY remains stubbornly high, similar to the higher for longer scenario.

However, in this case, the economy slips into a recession where Real GDP <0%

Non farm payrolls will drop at the rate of Real GDP, below 0%. This will result in an uptick in Unemployment rate, likely above 4.1%.

Average Hourly Earnings will also drop below Core Inflation, thus resulting in negative Real Wages.

This scenario is most likely to play out if there is an uptick in commodities or goods inflation, such as Oil and Food prices.

The action on Fed’s behalf will be complicated, and difficult to assess currently.

An inflationary Recession: This is the worst possible outcome for the US. This will resemble some form of a BOP (balance of payments) crisis, often observed in emerging market economies. This scenario will be treacherous for the US Treasury Market and the US Dollar. I have outlined the scenario in the table with the data points, but since I don’t think this scenario will play out as the next possible scenario for the US economy, I am not going to go deeper.

(Please Note: All economic scenarios are transient and as data prints become available, the probabilities of each scenario changes. The purpose of the US Economic Scenario Map to look at data in a meaningful, critical and framework driven way.)

In the coming sessions, I will be diving deeper into the economic scenarios, key macroeconomic concepts and data. If you like to connect the dots in macroeconomics, technology and society to understand the “big” picture, then I would be very grateful if you show your support by liking the post, leaving a comment and sharing with your network.

Amrita

Thank you for inviting me to read and subscribe to your Substack newsletter! Your Economic Map is a is clear and systematic way for interpreting this confusing market! I may argue that in a productivity accelerating scenario, the real GDP growth can be closer to the long-term potential of 2 to 2.5%, especially you have a PCE growing at 4% (personal consumption is almost 70% of US GDP). Look forward to reading more stories and the growth of your newsletter!