Kellogg's just broke up its cereal business. It now wants to sell you snacks.

Kellogg’s, the world's iconic cereal company split into 2 to sharpen its focus on snacks. The snack economy is raging & CPG companies concentrate their focus on snack innovation to boost profits.

At a Glance

The Kellogg’s brand is synonymous with cereals. But with the multi-decade decline of their cereal business, the company is branching out into other growth priorities such as cookies, crackers, chips, pretzels & popcorn.

A deeper look into the CPG industry reveals how companies in this space are boosting focus on their snacks business, in order to take advantage of burgeoning inflationary trends and optimize their pricing strategies, as consumers obsession with snacks continue.

According to a recent Bernstein Research, consumers often stick with their chosen brands of chocolate and other snack foods even when their prices increase.

“History never repeats itself, but it often rhymes.” A look at the Cola Wars from the 1970’s stagflation era also gives us a clue as to why CPG companies are getting excited to bet on snacks again.

With the snacks industry showing signs of long term growth, companies are ramping up their investments ahead - Kellogg’s split, M&A activity such as the Hormel+Twinkies deal and rapid snacks innovation are some of the strategies.

Kellogg’s, the iconic brand behind all the cereal boxes and crackers, rewrote their 117 year history by splitting into 2 separate business entities last Monday - Kellanova and W.K Kelloggs.

While W.K. Kelloggs KLG 0.00%↑ will be the sole owner of all cereal brands such as Frosted Flakes, Fruit Loops, Mini-Wheats, Special K, Raisin Bran, Corn Flakes and Kashi, the oddly named Kellanova’s K 0.00%↑ portfolio of brands will include all of the erstwhile Kellogg’s snack brands such as Pringles, Rice Krispies, Cheez-It and Pop-Tarts. Kellanova will also include plant-based products such as Incogmeato & RXBAR.

As per the CEO and the Board of Kellogg’s, the rationale behind splitting Kellogg’s into 2 separate business units is to drive greater operational, strategic and financial focus for each businesses. On being probed further, Kellanova’s CEO Steve Cahillane pointed out the tremendous growth that the company has been seeing in their snack business, especially in Emerging markets. Steve also called out countries like Nigeria, Brazil and India where Kellanova is able to take advantage of their growing market share.

A deeper look into the Kellogg’s book of accounts and their income statements validate the CEO’s comments and highlight a larger trend in the industry that could possibly be on its way up.

Why is Kellogg’s refocusing on Snacks?

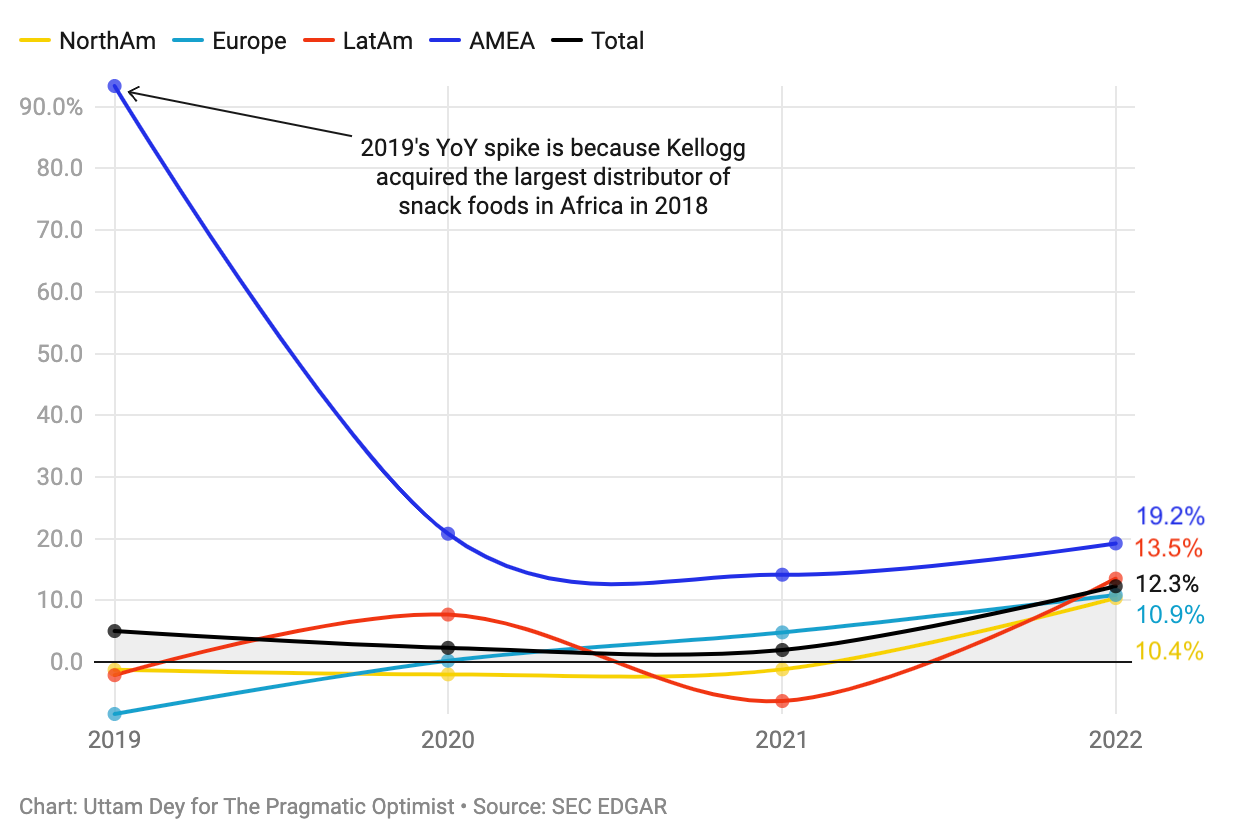

The last 4 years of Kellogg’s annual statements highlight that there is one definitive trend that is not backing down - American consumers have been buying more snacks with every year that passes by.

Cereals are kind of a mixed bag performance. Frozen foods were always on a decline. When the pandemic-era lockdowns started, consumers initially stress-ate frozen foods (like frozen pizzas and such), but quickly stopped spending money on frozen foods the moment the lockdowns ended.

Moreover, this does not seem to be just a trend that is just localized to the US. Consumers in many countries appear to have adjusted their spending patterns to purchase more snacks - especially those in emerging markets such as Latin America (LATAM) and Asia, Middle East & Africa (AMEA). Africa & Asia are now the fastest and largest growth markets for snacks in the world.

In fact, Steve Cahillane, CEO of the newly formed entity Kellanova, has been doing roadshows after roadshows proudly telling investors that “80% of Kellanova’s portfolio is now snacking and international businesses - very high growth”.

It’s not just Kellogg’s. The snack powerhouse brands of the world have also been resharpening their focus on emerging markets and further innovating the pipeline of products in their snack businesses.

It’s not just Kelloggs. The entire Consumer Foods & Beverage industry is booming as they notoriously raise prices amidst strong consumer demand.

Look at the chart (below) of the price mix vs sales volume for some of the world’s largest consumer food & beverage brands. The chart demonstrates the pricing power that these companies have at their disposal. Price Mix is a term used to describe the amount by which company’s raise the prices of their products during a given period of time. Sales Volume is volume of units sold by the company.

In this case, most companies (that have been captured in the chart below) have been able to increase prices of their products by a whopping 13.6% on average for the first half of 2023, while their sales volumes have fallen just -0.9% on average during the same period.

This is taking place in the background when US CPI (inflation) has been generally receding. While the Food and Beverage CPI index rose 1.7% in the first 6 months of the year, US Retail Sales for Food & Beverages rose by a paltry 0.2%. So far, it looks like the price increases of these CPG (Consumer packaged goods) companies are far greater than what the US CPI number is reporting.

Ramon Laguarta, CEO of PepsiCo PEP 0.00%↑, said in July that consumers have continued to buy Pepsi's brands, including Quaker Oats and Gatorade, even though these products have become more expensive. "We've been able to raise prices, and consumers stay within our brands," he said during the Q2 earnings call. At the same time, on Kellogg’s earnings call, the management also sounded confident of over-achieving their financial targets primarily due to the “price elasticity” that they are seeing in their shelf products.

Price elasticity is a measure of how demand responds when the price of a good or a service changes. A product can have a high degree of price elasticity or a low degree of price elasticity. If the demand for a product or service quickly shifts once price changes in either direction, then the product or service has a high price elasticity (think luxury items, dining out, etc.). If the demand for the product or service does not shift once price changes in either direction, the product or service has low price elasticity (such as groceries, gasoline, etc.).

Most CPG companies began seeing tighter price elasticities across their products, which is the main reason why they were confident to raise their financial targets for the fiscal year.

Kellogg’s has already raised their financial targets twice this year. Pepsi announced that they are raising their targets for FY23 again in their Q3 earnings report this week.

The comments coming out of the boardrooms of some of the world’s largest CPG companies are indicating that there are more price hikes that would be coming for a much longer period of time - much in line with the Fed’s higher-for-longer interest rate narrative.

The chart below might also give a clue as to why companies are so keen on hiking the prices of their consumer products. Today, we can see that some of the largest CPG companies in the world are lagging behind their 10Y average gross margins. In order to catch up, companies are boisterously raising prices as demand does not show any material sign of weakness. As per business logic, why leave money on the table?

What others are saying?

The Snack Foods Association (SFA) is an international trade group of the snack food industry that represents snack manufacturers and suppliers worldwide. The association has previously noted that "personal indulgence has proven to be pandemic and inflation-proof.” According to the SFA, chips, pretzels and other snacks were the highest-selling specialty food category in 2022, moving up from third place in 2021 and becoming the first specialty category ever to exceed $6B in annual sales.

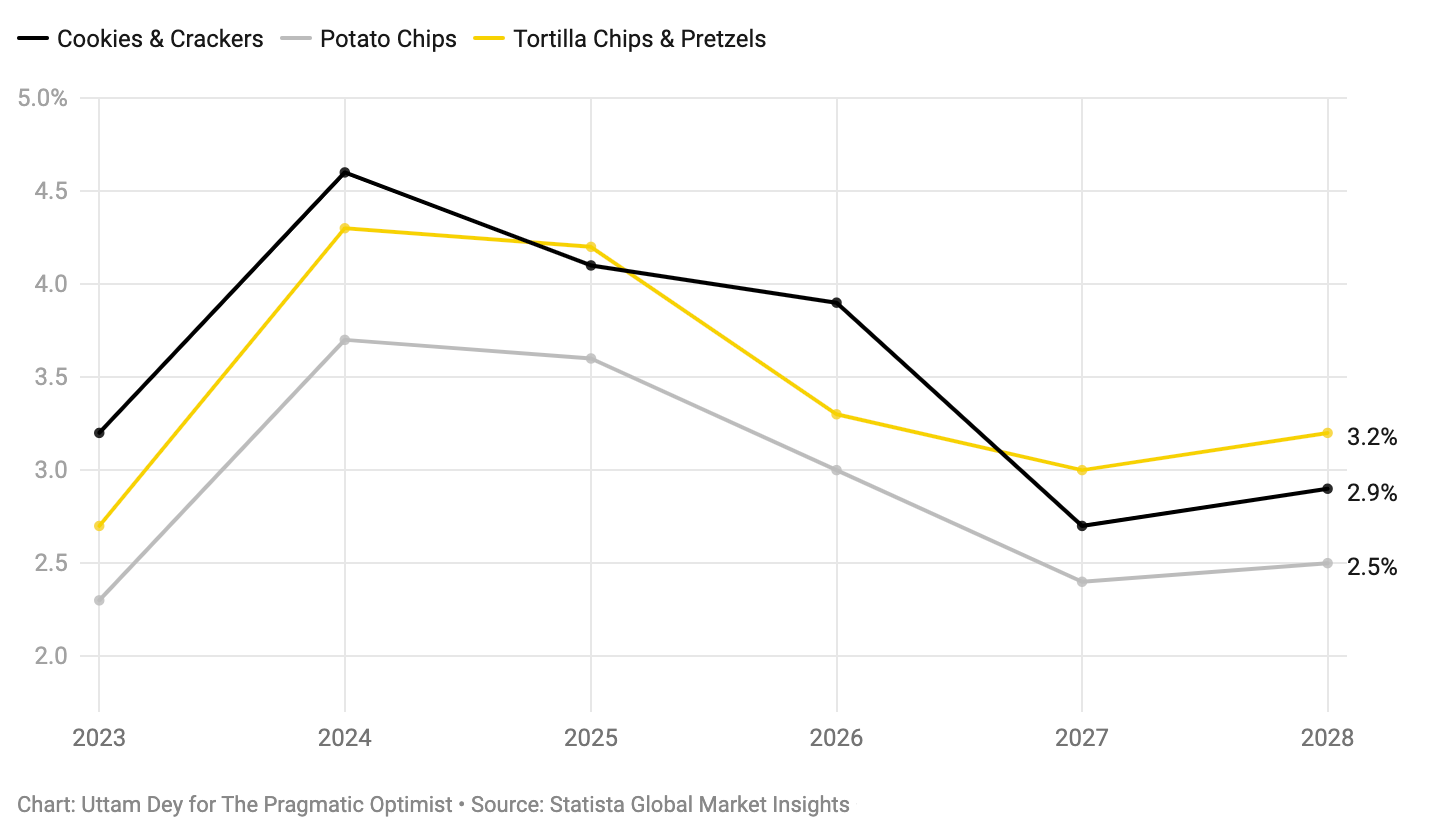

A separate projection from Statista Global Market Insights also confirms the study by the SFA.

According to Statista Global Market insights, “Cookies & Crackers” segment are projected to be the fastest growing sub-category within the Snacks industry in 2024, growing at 4.5% YoY. The growth rate is then expected to flat line to around 3% for a good part of this decade. Any participant in the industry will take these numbers given that the Cookies & Crackers sector was growing at just 1.9% in 2019.

M&A activity in this space has also picked up with Hormel Brands HRL 0.00%↑ acquiring Twinkies owner Hostess TWNK 0.00%↑ for a 30% premium while Mondelez acquired ClifBar MDLZ 0.00%↑ in June last year for $2.9B.

A look back at history also shows how companies that align their product portfolio towards snacks tend to outperform their peers during periods of high inflation. Such was the case during the 1970’s Cola Wars that we talk about in the next section.

The 1970’s Cola Wars show how Pepsi gained an edge over Coca-Cola because of its snacks portfolio.

In the 1970’s, when inflation was raging, consumer spending had started to fall. But companies that sold products which were price inelastic not only stood to gain financially, but were also rewarded by investors.

An example would be how Pepsi positioned itself during the 1970s inflation era by purchasing Frito lay and expanding its product catalog into snacks. This enabled Pepsi’s stock to outperform Coca-Cola’s KO 0.00%↑ stock and the S&P 500 index during the decade that followed.

How did investors take the news of Kellogg’s business split?

As of market close on September 29, 2023, Kellogg’s was worth $20.4B. By the time trading closed on the following Monday, it had become two separate companies worth $19.1B combined, having lost almost $1B in market value.

Last year on June 21, 2022, when Kellogg’s had announced that they intend to spin out Kellogg’s fast-growing snack business into a separate entity, markets cheered, sending the stock up 10% higher. Yet on the day, the company officially split on October 2, 2023, the stock tanked.

The sentiment could be led by the news headlines of the weight loss drug Ozempic that is causing ripples in the stock market and the food industry. Companies such as General Mills GIS 0.00%↑ , Coca-Cola, Hershey and Kellogg’s are experiencing sharp declines in their stock prices, and Walmart WMT 0.00%↑ has reported changes in shopping demand driven by consumers who are taking the drug.

We don’t think that this is a long term phenomena that will reshape consumers’ snacking behaviors. We believe that the current sell-off in the consumer food and beverage industry will likely cease as soon as the news of Ozempic dies down.

Closing Thoughts!!

The snack industry is booming. Brands have already taken note and are adjusting their consumer product catalog, keeping in mind of the generational mix in consumers. While salty snacks like pretzels, chips and popcorn are back in vogue, brands are heavily investing in food innovation to cater to the changing palates of their consumers and build on the momentum they’re seeing in their snacks business.

Upcycled foods for the environment-conscious, sleep-inducing snacks for the late-night snackers, and rose-flavored potato chips are just some of the innovations that are happening in this space, as brands try to innovate their way into their consumers wallets.

The CPG sector that had been on the decline for many years has now suddenly awoken.

🥨🍿🍪🍫🍟 What are some of your favorite snacks that you are munching on these days? We would love to hear in the comments section below.

Uttam & Amrita 👋🏼👋🏼

| A guest post by

|

Awesome. thanks for this. And I love a Toblerone or chocolate M&M's.

Fine work... And tasty.