Launching Tuesday Top Picks: Why am I bullish on Pinterest, Toast and Duolingo?

Discussing Pinterest and Toast that are up 22% and 60% respectively in portfolio and Duolingo that I am looking to initiate a position in after post-earnings sell-off.

Welcome everyone to The Pragmatic Optimist.

In case you are wondering whether this is a delayed Monday Macro or an earlier Thursday Dive, it’s neither. I’m launching a brand new segment to The Pragmatic Optimist- Tuesday Top Picks 🥁🥁🥁 , where I will highlight some of the key companies that I am investing in, carefully watching, or getting ready to sell.

A quick background: For me, investing has always been about finding companies that sit at the intersection of 1) technology waves and 2) societal/cultural waves. Many of you know that I have been an active contributor on Seeking Alpha since the beginning of the year. And so after some thinking, I decided it was time to bring my “investing” voice on to the Substack platform and share investment ideas from the key companies that I own or would like to own in my portfolio.

So, without further ado, let’s get started.

Plan for today: Today, I am going to talk about two winning stocks in my portfolio and one that I am currently watching. I will take a “rapid-fire” like approach, where I will answer a list of 5 questions in 3 minutes (reading time wise) per company. After that, you can recommend which one of these companies you would like me to do a deep-dive in the next edition. Sounds good?

Pinterest- Winning with GenZ’s with plenty of runway for user user monetization | Status: Bullish 💪

**Let the timer begin**⏰⏰⏰

✅ What is Pinterest and how does it make money?

Pinterest is a social commerce-based product discovery platform where over half a million users share, explore, curate and shop for ideas related to various interests. Whether it is recipes, workouts, travel, fashion or wedding planning, users can discover and save content (images, videos, etc.) in the form of “pins” and organize them into virtual “boards”.

In terms of its business model, Pinterest generates revenue through advertising, which are strategically displayed on users’ boards, based on relevant search terms and interests.

✅ Why am I bullish on the stock?

User acceleration on the platform: The highlight of Q1 earnings report was its record of 518M Monthly Active Users (MAUs) on the platform, which has grown steadily over the last 7 quarters, up 12% YoY. Interestingly, just 18% of global MAUs are based in the US & Canada, which contribute 80% of total revenue. This means that the company has over 80% of its users abroad, who are contributing just 20% of total revenue, indicating plenty of room for deeper monetization down the road.

AI-led product innovation to improve user experience: Pinterest is heavily leaning into AI to improve personalization and promote user curation as they transitioned from CPU to GPU serving with larger model sizes. At the same time, it has also integrated more shoppable content, as well as launched shoppable video allowing users to pick up where they left off on prior shopping journeys, which I believe is distinct from the rest of social media, allowing it to drive deeper user engagement.

Winning with Gen Z’s: Gen Z’s represent more than 40% of all MAUs, saving 2.4x the content compared to the rest, as they see Pinterest as an “oasis away from the toxicity of social media”. As Gen Z’ers graduate from school, transition to their first full-time job, and gather more spending power, I believe Pinterest should stand to benefit from the demographic tailwind to drive revenue growth.

Focused efforts to drive user monetization: Pinterest has been heavily focused on driving lower funnel improvements for advertisers, which has doubled clicks and conversions YoY for advertisers with the rollout of Direct Links to their lower-funnel ad formats. At the same time, it is also scaling its third-party demand with Amazon Ads in the US and Google Ads Manager, which went live in February in unmonetized international market

Setting 3-5 year plans: The management has laid forth its 3-5 year plan, where it expects its revenue to grow in the mid to high teens, while reaching an Adjusted EBITDA margin of 30% (up from 23% in FY23), as the company continues to leverage user intent by translating it into improving user experience and actionable outcomes, thus growing ad load on the platform, especially as the company grows its monetization outside of the US through a combination of product innovation for advertisers, integrating third-party ad demand and partnering with agencies to grow within these markets.

✅ Where can my thesis go wrong?

A slowdown in the US and global economy can certainly derail consumer discretionary spending, which can hurt Pinterest’s Average Revenue per User (ARPU). Also, while there is tremendous growth for user monetization outside of US & Canada, given the abysmally low ARPU in those regions, there could be challenges to convert user intent to commercial outcomes.

✅ How far up can the stock go from here?

Based on management’s 3-5 year plan, if revenue grows in the mid teens range until FY28 with EBITDA margins expanding to 30%, the company should trade at a PE ratio at least 2x the average multiple of the S&P 500 of 15-18, given the growth rate of its revenue and earnings. This would translate to a PE ratio of 30, or a price target of $51, which represents a further upside of 22%.

✅ What am I doing with my position?

I initiated a position worth 2% of my portfolio at $34 in March, when I estimated the upside to be over 50%. Since then the stock has risen 22%, outperforming the S&P 500. While I will likely trim my position should the price of the stock $50, I continue to remain bullish on Pinterest given the management’s execution in turning the business around since its trough in 2022.

Toast- Expanding new restaurant locations with deepening adoption of its modules | Status: Bullish 💪

**Let the timer begin**⏰⏰⏰

✅ What is Toast and how does it make money?

Toast is a cloud-based technology platform for the restaurant industry. The company derived 81% of its revenue from processing transactions in Q1. At the same time, Toast is rapidly growing its Subscription service, where it sells its customers modules such as digital ordering and delivery, marketing and loyalty, and supply chain, among others, to help them improve efficiencies and elevate their diners’ experiences.

✅ Why am I bullish on the stock?

Accelerating market share in a large TAM: With an estimated total addressable market (TAM) of 860,000 total restaurant locations in the US, Toast added 6000 new locations in Q1 on the platform growing 32% YoY. This brings the total number of restaurant count on the platform to 112,000 or a market share of 13%, up from 12.3% last quarter. Not bad. (Plus, the company is also expanding into Canada, the UK and Ireland).

Growing revenue, especially as customers adopt more modules: 43% of Toast’s customers are using six or more Toast product modules. With growing adoption, Aman Narang, CEO of Toast has been focusing efforts to build a robust sales organization to drive a higher volume of upsell per location, which should result in growing average revenue per restaurant location, as well as improve operational efficiencies.

Robust product innovation to continue winning: Recently launched their Digital Storefront and Marketing suite to help restaurants create tailored guest experiences. One of the key enhancements that I believe is particularly noteworthy is integrating AI to create email marketing campaigns and drive targeted promotional offers, which I believe will attract guests and accelerate return and repeat orders. Its innovation is already paying off with Toast entering into an agreement with Snooze A.M. Eatery to improve their guest experience and deliver faster and more accurate service through their platform across 70 locations in the US.

Improving operational efficiencies: Delivered $57M in Adjusted EBITDA, up from a loss of $17M last year, as streamlining sales and marketing spend, coupled with growing adoption on the platform enabled Toast to expand its profitability.

✅ Where can my thesis go wrong?

Slowdown in consumer spending in restaurants amid a macroeconomic slowdown can push restaurants to cut back on spending, especially on their tech stack in order to protect their margins, thus hurting Toast’s growth prospects.

✅ How far up can the stock go?

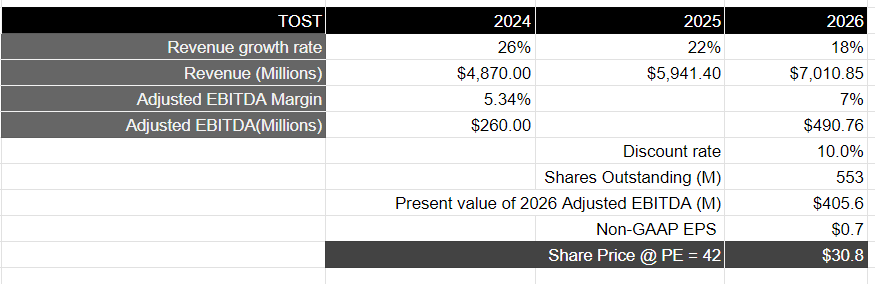

Raised guidance for FY24: The company is expected to grow its revenue 25-27% YoY in FY24 to $4.8B, a slowdown from the 42% growth rate from the previous year, while Adjusted EBITDA margins are expected to expand from 1.3% in FY23 to 5.34% in FY24.

My assumptions looking forward: The company should continue to grow its revenues in the high-teens to mid-twenties region in the coming 2 years, driven by market expansion as well as deepening adoption among existing customers. Assuming that margins expand with increasing economies of scale to 7-9%, it should generate approximately $500M in Adjusted EBITDA, or $400M when discounted at 10%. If we attach a 2.5-3x multiple of the average S&P 500 PE ratio of 15-18, we arrive at a price target of $31, which represents an upside of 14%.

✅ What am I doing with my position?

I initiated a position, worth 1% of my portfolio in January at a price of $17.45. Since then, the stock is up 60%, beating the 10% gain of the S&P 500. However, given the risk-reward at the moment, I am going to trim my position by 33%-50% to book profits in the short-term, while keeping a long-term bullish view on the company.

Duolingo- Faster conversion from freemium to paid subscribers and rising profitability | Status: Bearish, turned to Bullish 💪

**Let the timer begin**⏰⏰⏰

✅What is Duolingo and how does it make money?

Duolingo is primarily a language learning app and its mission is to develop the best education in the world and make it universally accessible. In terms of its business model, Duolingo employs a “freemium” model, where users can access lessons without any cost, with the option to subscribe to premium tiers that includes Duolingo Super and Duolingo Max for an ad-free experience and extra features. The company generates 78.5% of its revenue from Subscriptions, while the remaining came from a combination of Advertisement, Duolingo English Test and in-app purchases.

✅Why am I bullish on the stock?

Highly engaged users on the platform leading to growing monetization: Daily and Monthly Active Users (DAUs and MAUs) grew 54% and 35% YoY respectively in Q1. Meanwhile Paid subscribers as a percentage of MAUs rose from 8.3% in Q4 to 8.6% in Q1. Part of that could be driven by the company’s rapid culture of gamification (their mascot Duo being the star of the show) and creative marketing campaigns, such as their Superbowl Ad and April Fool’s brand moment.

Product expansion & leveraging AI to build immersive experiences: In 2023, Duolingo expanded into Maths and Music to unlock new addressable markets. Meanwhile, the company continues to leverage generative AI to develop new features and lesson types that enable more conversational and listening practice, with the launch of DuoRadio in FY23.

Expanding profitability: Generated $44M in Adjusted EBITDA, which grew 190% YoY, with margins expanding to 26.4% (from 13.1% a year ago), as the company drives higher conversion of freemium to paid users, given a highly engaging and entertainment-driven learning app.

✅ Where can my thesis go wrong?

Over 47% of Duolingo’s revenue is generated internationally. While this could be viewed as an opportunity, it could also also be a threat if Duolingo fails to drive effective conversion from freemium to paid as a ratio of their sales and marketing spend. On top of that, consumer fatigue is also something to be aware of, especially if the effectiveness of Duolingo’s gamification strategies start to wear off.

✅How far up can the stock go?

Raised guidance: The company is expected to grow its revenue 37.5% YoY to $731M in revenue, with an Adjusted EBITDA margin of 23.5% (up from 17.6% a year ago).

My assumptions moving forward: The company should continue to grow its revenue in high twenties range over the next two years, coupled with a margin expansion from a projected 23.5% to 25% in FY26, as it drives new product innovation to expand into new markets, attract, engage and convert users, especially as the language learning market is expected to double in 2025 to $115B. This will compress its PE ratio to approximately 31 by FY26, which I think makes the stock “undervalued”, given the growth rate of its earnings and revenue over a 3-year period, with potential for substantial upside in my opinion.

✅ What am I doing with my position?

I never owned the stock, as I had doubts about the company’s profitability picture. But given the management’s operating excellence thus far, I am looking to initiate a position. I may start a small position at its current levels and then cost average should it decline further, given the growing probabilities of a short-term pullback in the S&P 500.

, , , any insights on the technical landscape of the above stocks?Need your feedback

This is the first pilot of Tuesday Top Picks, and I would really appreciate feedback in order to constructively iterate and improve this segment. I also want to give a shoutout to

, , , , whose work has lately inspired me to start this segment on Substack. For the next edition, I was thinking of doing a deep-dive into one of the above companies, so I need your help in choosing which one.That’s all for today. If you enjoyed today’s post, you can support my work by buying me a a coffee ☕ and a muffin 🧁.

Amrita 👋🏼👋🏼

DISCLAIMER: This is solely my opinion based on my observations and interpretations of events, based on published facts and filings, and should not be construed as personal investment advice. (Because it isn’t!)

It's nice to see you've decided to showcase more of your monster talent. Looking forward to next Tuesday.

I really enjoyed this, Amrita! Looking forward to the deep dive. And thank you for the shoutout!!