Oil prices are spiking. What will happen next?

Will rising oil prices see an uptick in inflation? Will US economy grow or fall into a recession?

At a Glance

Oil Prices are going up. With Fed funds rate at 5.25-5.5%, Headline and Core Inflation (PCE) stands at 3.3% and 4.2% respectively. This is higher than the Fed’s long term Core Inflation target of 2.2%

A spike in oil prices will lead to an uptick in Goods Inflation as oil is a major economic input. Rising oil prices increases the cost of producing goods. Producers will pass the cost to the retailers, who will ultimately pass the cost to consumers, creating higher inflation.

Since the tightening cycle began in 2022, Headline Inflation has come down much faster than Core Inflation. The decline in overall inflation is mostly attributed to falling prices in commodities, durable and non-durable goods.

This gives rise to 2 possible paths for the US economy.

US Economy grows, albeit slowly from current levels, at higher inflation levels.

Economy falls into a recession, i.e. Real GDP < 0%

If the economy grows, the Fed will be able to raise rates. If the economy falls into a recession, with inflation at high levels, it is difficult to assess Fed’s moves at this point.

As a result, we have 2 possible scenarios with the highest probability at this point playing out for the US economy next. Higher for longer or Stagflation.

1. What’s happening in the news?

Last week, Saudi Arabia further extended a voluntary 1 million barrel per day oil production cut until the end of December 2023.

Russia, the world’s second largest oil exporter, also agreed to extend 300K barrels per day cuts through the end of the year.

In the US, gas prices are climbing once again, topping a 10-year record for early September. At $3.81, gas prices are higher than at this time last year, and the second-highest on record for this time of year in AAA records going back to 1994.

In July 2023, IEF Secretary General, Joseph McMonigle told CNBC, “So, for the second half of this year, we’re going to have serious problems with supply keeping up, and as a result, you’re going to see prices respond to that.”

McMonigle had further stated that India and China combined would make up 2 million barrels a day of demand pick up in the second half of the year.

At the same time, US crude inventories at the Strategic Petroleum Reserve are at their lowest since 1983 after record drawdowns last year.

Long story short: Supply is tight, demand is strong. As a result, Oil prices are going higher.

2. What does oil price have to do with inflation?

Crude oil is a major economic input.

So a rise in oil prices contributes to a rise in the cost of producing goods, which results in a higher rate of price increases in the economy.

Classic inflation!

Oil prices exert more influence on the Producer Price Index (PPI), which measures the prices of goods at the wholesale level, than Consumer Price Inflation (CPI), which measures the prices consumers pay for goods and services.

Between 1970 and 2017, the correlation between oil prices and the PPI was 0.71.

In comparison, the correlation between oil prices and CPI is 0.27. The weaker link between oil prices and consumer prices comes from the higher weight of services in the U.S. consumption basket.

3. So, rising oil prices won’t produce consumer price inflation?

On the contrary.

When the Producer Price Index goes up (because of a rise in oil prices, or other inputs), producers will pass the cost over to the retailers.

The retailers then markup the price of goods in order to pass the cost over to the consumers.

End result: Consumers pay a higher price for the goods they buy. And now, we have a rise in Goods inflation.

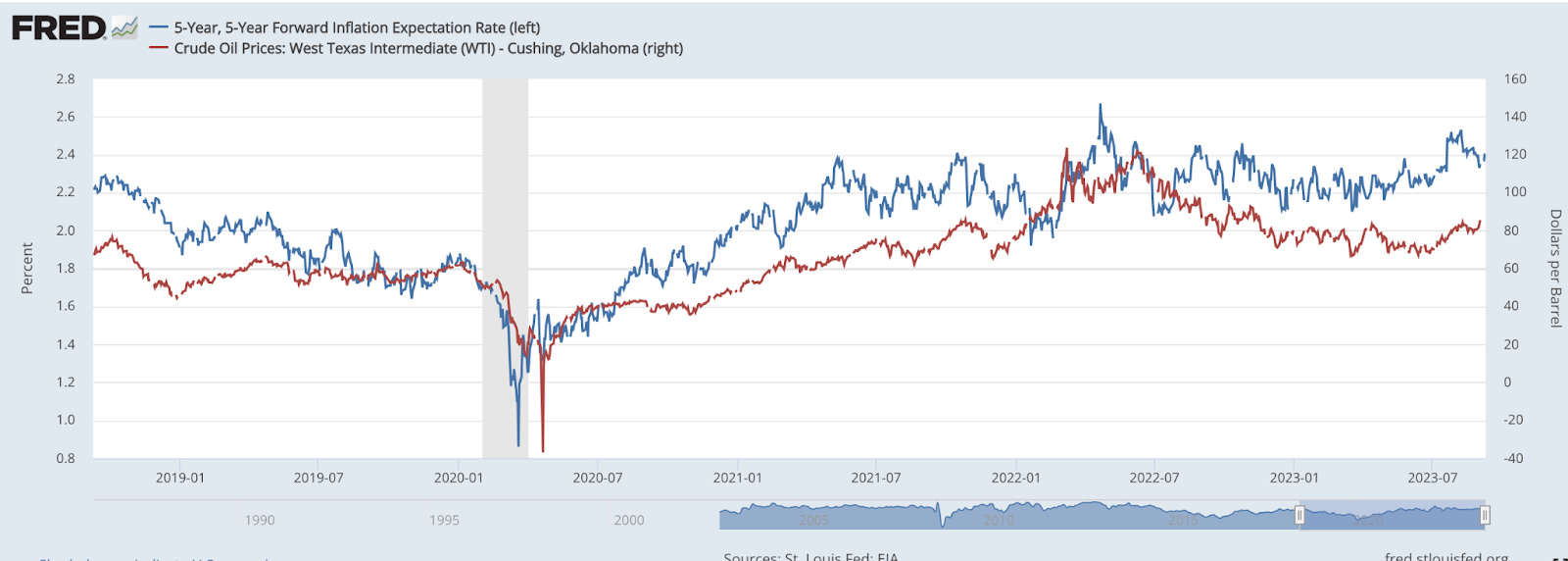

In fact, the direction of Crude oil prices have a positive relationship with 5 year forward inflation expectation, as shown below.

In other words, as crude oil prices climb, long term inflation expectation for the US economy starts to climb as well.

And we all know that Fed Chair Powell is stubborn about his 2.2% long term inflation target.

In other words, if the long term inflation expectation starts to accelerate beyond 2.2%, he will be forced to raise rates or move his inflation target.

This is not good for financial markets in the short term.

4. One more perspective

Finally, Ryan Lemand illustrated the following perspective:

Inflation started with goods prices on the back of the pandemic, supply chain disruptions and accommodative monetary and fiscal policies that allowed Americans to accumulate massive savings, hence spending power.

Services inflation came later, once the economy fully opened and Americans demanded more services.

Since the tightening cycle began, we have seen both Headline and Core CPI come down. But, Headline CPI has come down much faster than Core CPI, since Services Inflation continues to remain at an elevated level.

In other words, the decline in overall CPI since last year is mostly attributed to falling prices in commodities, durable and non-durable goods.

Therefore, given current levels of inflation (that is higher than Fed’s 2023 projection and long term target), an uptick in oil prices will have a direct and indirect effect on consumer prices.

5. Connecting all the dots together

Federal Reserve Chair Jerome Powell mentioned in his semiannual testimony before the U.S. Senate Banking Committee in March 2022 that, as a rule of thumb, every $10 per barrel increase in the price of crude oil raises inflation by 0.2% and sets back economic growth 0.1%.

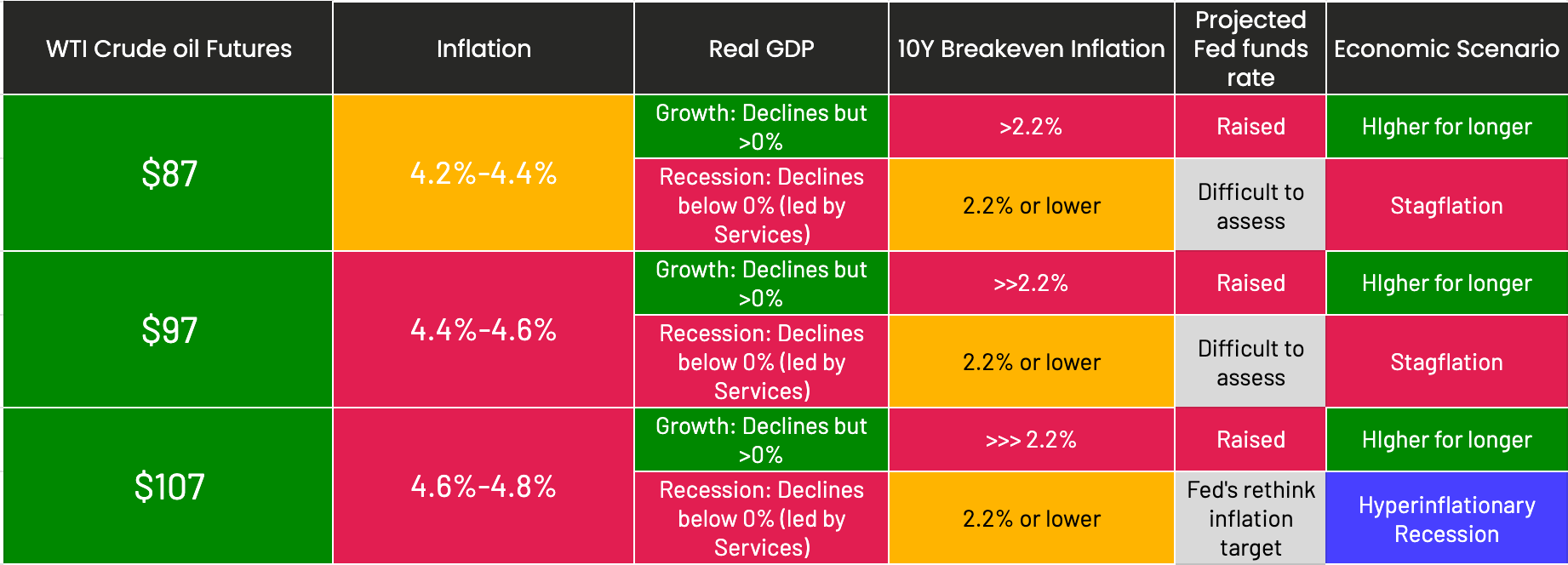

Last week, I presented you with the Economic Scenario Map. In the Scenario Map, I built in 6 key scenarios that are likely to play out in the US given the direction of Real GDP and Inflation.

So, using that framework, let’s understand how the rise in oil prices is going to shape the probabilities of the key economic scenarios for the US.

Key Takeaways

Given where Headline and Core Inflation is at the current Fed funds rate of 5.25-5.5%, an uptick in oil prices will inevitably lead to higher overall inflation.

This will give rise to 2 possible paths for economic growth.

Economy grows, albeit slowly from current levels.

Economy falls into a recession, i.e. Real GDP < 0%

Given the resilience of the US consumers and businesses, in the face of higher inflation and rates, will determine how the spending across goods and services evolve. That will dictate whether the US economy grows or falls into a recession.

If the economy grows, the Fed will be able to raise rates.

If the economy falls into a recession, with inflation at high levels, it is difficult to assess Fed’s moves at this point.

As a result, we have 2 possible scenarios with the highest probability at this point playing out for the US economy next. Higher for longer or Stagflation.

I hope you enjoyed this post. If you like to connect dots to form frameworks in macroeconomics, technology and culture that drive investment decisions, please subscribe below.

Have a great week!!!!

Amrita