US credit-rating outlook is cut to negative by Moody’s. Why should you care?

As US fiscal deficits widen, the yield on longer duration US Treasury debt rises as the Fed doesn't provide any accommodation. With growing interest expenses and debt burden, what happens next?

«The 2-minute version »

Overview: On Friday November 10, Moody’s lowered its outlook on US credit-rating from stable to negative. The ratings agency stated that as US fiscal deficits widen, it poses increasing risk to the country’s fiscal strength.

In case you don’t know: A sovereign credit rating is an assessment of the creditworthiness of the sovereign entity, which investors use to assess the riskiness of a particular country’s bond. Think of it like your personal credit score, now extrapolated at a national level.

Background: The US federal deficit is projected to grow from 6% to 10% of GDP by 2053 as per Congressional Budget Office. Meanwhile, the US economy is projected to grow between 1.5-1.8% in real terms. At the same time, interest rates and the 10Y US Treasury bond yield is expected to remain elevated.

Zoom in: The US government sits on a record debt level of $32.6T. Last week, we saw the lowest demand in 30Y US Treasury auction in over 2 years. With the Fed not accommodating, the private sector demands higher yield on longer term US Treasury bonds, thus raising interest expense and the debt burden of the US government. Plus, higher 10Y yields also raises the cost of borrowing across all players in the economy and further squeezes bank lending.

Why you should care: While the US dollar is the world’s reserve currency and its network effects can’t be outcompeted, the future path of inflation and growth will determine US’s creditworthiness and how you should position your investments.

If inflation and growth continues at the pace that matches the Fed’s projections, US credit-rating should remain more or less stable. However, growth assets will continue to remain under pressure. Investors will gravitate towards gold, bitcoin, cash and companies with non-cyclical revenues with significant cash piles.

If inflation picks up from current levels, expect to see more foreign investors and institutions selling US bonds. This will cause the longer dated yields to spike and may risk further downgrade of US credit-rating. This is reminiscent of a stagflation and gold has proven history to protect investors’ wealth during these confusing times.

Should inflation decline from current levels, led by a surge in productivity growth, we may see yet another cycle of growth and prosperity for the US economy. As growth assets outperform in this phase, we may also see US regain its top-notch credit-rating once again.

!!!Welcome back everyone to The Pragmatic Optimist!!!

Many of you know that I took a week off from writing the past week. During this time, I went out for longer runs in Stanley Park to catch some of the remaining gorgeous foliage, cooked some comfort Indian food like dal (lentils) and curry, drank way too many cups of masala chai, got a much-needed haircut and celebrated Diwali.

I feel refreshed and re-energized and now I am ready to take us back on the journey journey to connect the dots in macroeconomics, investing and technology using data and intuitive frameworks in order to form the “big picture”, invest better and improve our financial and mental well-being.

Plus, this news below definitely gave me an extra energy boost. I got featured on Substack and I could not have done this without the support of each and everyone of you. And please know that I am forever grateful. If there is any way I can help you on your journey on substack, do not hesitate to reach out. 🙏🏽🙏🏽

Now, let’s get back to work 🥂🤝

Moody’s lowered its outlook on US credit rating citing risks to the US’s fiscal strength as its deficits widen.

Moody’s lowered its credit rating outlook on the US from stable to negative on Friday, November 10th. The ratings firm pointed to the rising risks to the US’s fiscal strength as the key driver behind the action. While Moody’s lowered its outlook on US credit, it still retained its top Aaa rating for US credit.

Moody’s said, “The downside risks to the US’ fiscal strength have increased and may no longer be fully offset by the sovereign’s unique credit strengths. In the context of higher interest rates, without effective fiscal policy measures to reduce government spending or increase revenues, Moody’s expects that the US’ fiscal deficits will remain very large, significantly weakening debt affordability.”

In August 2023, US’s credit-rating was cut from AAA to AA+ by Fitch Ratings. Fitch had cited alarm over the country’s deteriorating finances and expressed major doubts about the government’s ability to tackle the growing debt burden because of sharp political divisions.

So far, the US equity market has not negatively reacted to the news. In this post, we will cover the following topics that will enable you to understand the “big picture” behind Moody’s decision to lower their outlook on US credit-rating and why it matters to you as an individual and an investor.

What does a sovereign credit-rating mean?

Why is the private sector demanding higher yields on longer duration US Treasury bonds?

How large is the US fiscal deficit projected to expand by 2053? How will US economic growth fare at that point?

3 different ways how the future path of inflation and growth will determine US’s creditworthiness.

How will it affect your investment portfolio and what can you do to position accordingly?

Think of a sovereign credit rating like your personal credit score.

A sovereign credit rating is an assessment of the creditworthiness of a country or a sovereign entity. Investors use sovereign credit ratings as a way to assess the riskiness of a particular country’s bond.

Think of it like a credit score that rates your personal creditworthiness, based on your credit history, which includes information like your payment history, outstanding balances and other factors. Lenders use your credit score to evaluate your likelihood of repaying loans in a timely manner. If you have a higher credit score, it is easier for you to get approved for loans, rent an apartment or lower your insurance rate. If you have a lower credit score, you are going to have a harder time to get credit and may have to pay higher interest rates.

Sovereign countries and their credit rating works on the same principles as personal credit score. Moody’s considers a Baa3 or higher rating to be of investment grade and a rating of Ba1 and below to be speculative.

If you are curious to learn more about Moody’s rating scale and its rating definitions, you can click the link here.

The Private sector demands higher yield on longer term US Treasury bonds, thus raising interest expense and the debt burden of the US government.

The US government sits on a record debt level of $32.6T. During the October-December 2023 quarter, the US Treasury is expected to borrow $776B in net marketable debt. The borrowing estimate is $76B lower than what was announced in July 2023.

However, last week we witnessed the lowest demand for the 30Y US Treasury bond auction in over 2 years. This is driven by investors who are still not confident on peak inflation and interest rate narrative for the US economy and therefore, demand higher term premiums on longer-term maturities.

Plus, the Fed is not buying government bonds at the moment. Instead, it is still in the process of reducing its balance sheet size, which now stands at $7.8T (from a high of $8.9T in June 2022). When the Fed reduces its balance sheet size, it drains bank reserves and hence liquidity gets tighter. This means that not only does the private sector need to absorb all new US Treasury issuance, it has to do so in an environment of decreasing liquidity.

If you are curious to learn how the Fed creates and destroys money, I had written about it extensively in the post below.

Until the US and global economic indicators show convincing signs of a slowdown, the private sector will remain cautious about the long term picture of inflation and interest rates, and as a result demand higher yields from longer maturity US Treasury bonds.

Remember that higher long-term bond yields will result in the government's interest expense to rise faster than expected, which would mean that the government would need to issue even higher quantities of debt to finance their interest payments and the vicious debt cycle continues.

However, the longer interest rates remain high and the Fed continues to drain reserves in order to quell inflation, the higher the probability grows for a liquidity crisis in the repo market.

In the past cycle (post 2008 GFC), we had witnessed a repo market crisis in 2019, when the Fed was in the process of reducing its balance sheet size. When bank reserves reached $1.5T, Treasury yields suddenly spiked, which signaled that there was insufficient liquidity in the system to absorb the US Treasury bonds. The Fed immediately came to the rescue and started accommodating by purchasing government debt once again.

Today, the bank reserves sit at $3.14T, and while the overall liquidity picture is not sending any grave signal yet, it is an important indicator to monitor to predict the likelihood of a possible liquidity crisis in the future.

With the US federal deficit projected to grow from 6% to 10% of GDP by 2053, US economy would grow slowly at 1.5-1.8%. Sounds like a stagflation?

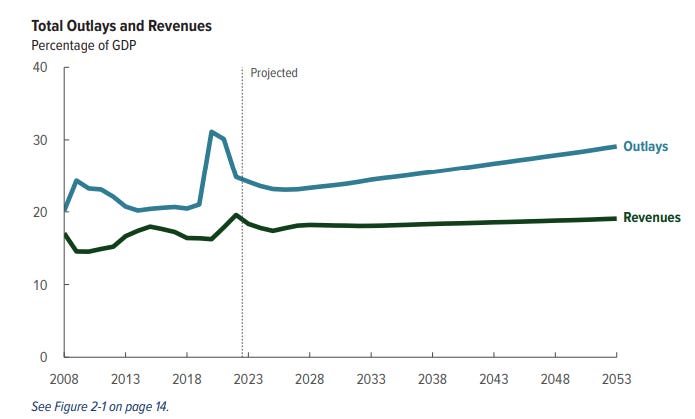

The US faces a challenging fiscal outlook. If current laws generally remain unchanged, budget deficits and federal debt would grow in relation to GDP (gross domestic product). As per CBO’s projections, federal deficits increase from 6% of GDP in 2023 to 10% of GDP in 2053. Meanwhile government debt as a percentage of GDP is projected to reach 181% of GDP by 2053.

The growing federal deficit is driven by spending on interest payment and healthcare programs that are projected to increase faster than revenues. Rising interest rates and mounting debt cause net outlays for interest payment on debt to grow from 2.5% of GDP in 2023 to 6.7% of GDP in 2053. Outlays for major healthcare programs rise from 5.8% of GDP in 2023 to 8.6% of GDP by 2053, as the average age of the population increases and health care costs grow.

Meanwhile, total revenues grow by about 1% of GDP between 2023 and 2053. Individual income taxes account for nearly all of that growth.

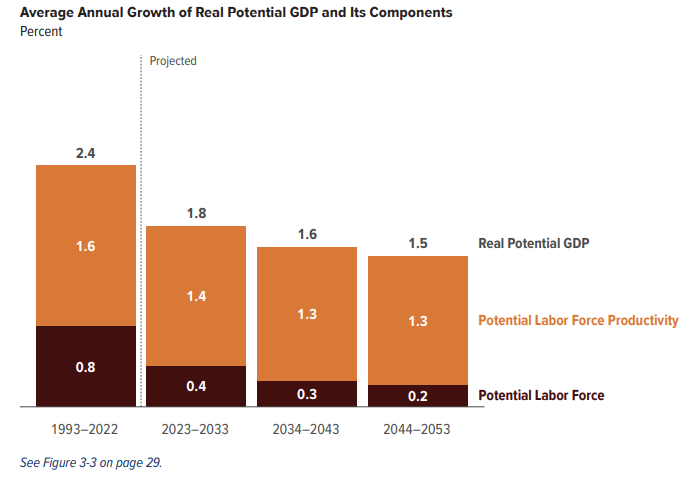

The state of the US economy will also affect the federal government’s budget deficit. As per Congressional Budget Office, Real potential GDP grows more slowly through 2023 to 2053 at an average pace of 1.8-1.5%. This is also in line with FOMC’s projection for long term GDP growth that they laid out during their September 2023 meeting .

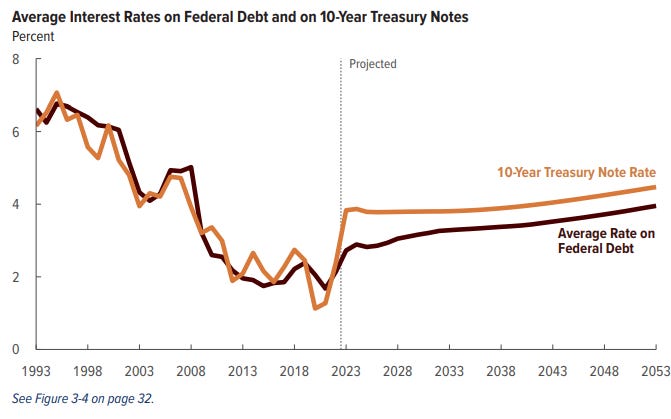

Finally, average interest rates on federal debt and on the 10Y US Treasury bond are expected to remain higher than they were in the post 2008 Great Financial Crisis period. Remember that government deficit is inherently inflationary as government spending creates “real economy money”. Therefore as government debt continues to grow in a high interest-rate environment, we are in for a period where inflation and interest-rates are expected to remain elevated, despite the US economy growing at a slower pace. Sounds stagflationary? 🤔

It’s not doomsday, at least as per Goldman Sachs.

The first time US credit-rating got cut was in 2011. At that time, the US took it pretty badly. The markets slumped and President Obama addressed the downgrade in a news conference and angrily denounced the decision as flawed.

This time, the market reaction has been more muted. A key reason is that the deterioration of US’s finances, the growing debt burden and the erosion of governance are now widely known.

Goldman Sachs put it bluntly when Fitch had downgraded US credit-rating in August 2023: "The downgrade contains no new fiscal information. The downgrade should have little direct impact on financial markets as it is unlikely there are major holders of Treasury securities who would be forced to sell based on the ratings change."

But there is still an impact, and what it means for your investments

Losing the AAA status in August 2023 means that the US is no longer part of an elite group of countries that maintain a top-notch credit-rating from all the 3 major ratings agencies. This is reputational damage.

Plus the Federal debt held by foreign and institutional investors have declined since its peak in Q4 2021. Should the US economy once outgrow its peers and successfully quell inflation, the foreign demand for US Treasuries will likely pick up in the future. However, when federal debt is projected to increase at the pace it is today, there are major risks that face the US.

These are 3 main ways it can play out below. 👇🏽

🎯If inflation and growth plays out as per the Fed’s projection

Should the inflation and growth for the US remain anchored at current levels, foreign demand for US Treasuries will most likely remain stable.

Assuming that the Fed would not accommodate as inflation continues to remain higher than the Fed’s long-term target, the yield on the 10Y Treasury bond will most likely remain elevated too.

In this environment, I would assume that the US government debt issuance would continue according to plan and bank lending in the private sector would continue to further tighten.

In this scenario, risk assets will remain under pressure and investors will gravitate towards cash 💵, gold 🥇, bitcoin ₿ and companies with non-cyclical revenues with existing cash piles, while remaining cautious on long-term bonds.

📉If inflation picks up from current levels, US credit-rating may come under further question

If inflation starts to pick up from here, the credit-rating of the US may once again come front and center. Foreign demand for US treasuries will decline.

Assuming the Fed doesn’t accommodate, the 10Y yields are most certainly going to rise as the private sector has to absorb new debt issuance.

Given higher inflation and possibly higher interest rates, government debt may continue to grow faster than expected as they now have to pay higher interest payments than was previously forecasted. Bank lending will be squeezed further.

This scenario is not positive for equities as the cost of borrowing will continue to go up. In my opinion, we are quite likely to experience liquidity events in the market, where the Fed will ultimately have to accommodate through Quantitative Easing.

However, it is unclear how the market will perceive the action of the Fed to perform Quantitative Easing, when inflation is still above target. In this environment, the safest asset class is gold 🥇. We may see strength in bitcoin too, should this scenario emerge.

📈A surge in productivity will bring an era of growth and prosperity, where the US regains its top-notch credit rating once again

Finally, should inflation go down from its current levels, driven by a surge in productivity, that would be the ideal “goldilocks” scenario. It is also possible that we enter this phase after a period of prolonged recession. However, in an era of higher than expected productivity and low inflation, foreign demand for US Treasuries will pick up.

The US may very well get the perfect credit-rating score once again from all 3 ratings agencies.

This scenario is positive for growth assets as cost of borrowing would go down. In the meantime, the demand for cash and gold will likely go down.

Do you think the US credit-rating will come under further pressure in the future or will the US get back its perfect score from all 3 ratings agencies soon? Please let me know in the comments section below.

Have a great week.

Amrita 👋🏻👋🏻

So sick of government mismanaging our tax dollars. Which party worse?

1. TAX & SPEND DEMS

2. BORROW & SPEND GOP

Answer: 2..! THE DAMN GOP BORROWERS

-- They lie shamelessly on their spending habits. Spend like drunk sailors when we’ve a GOP POTUS, then pretend they care about debt and deficits when POTUS is a Dem. WTF. They think we’re stupid. Are we?

-- They wouldn’t manage their household debt so irresponsibly. Ahem, they don’t need to because their corrupt “pay to play” shenanigans with corporate lobbyists (example: NRA) keep them in the black whilst they legislate in direct opposition to electorate’s interests. Apartheid rule in America.

-- They spend on top 2%, gaslighting us with their “trickle-down” BS. FYI dummies, it’s “trickle up” and “trickle out” that creates best societal outcomes - most people participating in healthy societal work/spend cycle, less criminality, better levels of education, happiness, healthiness.

***PRESCRIPTION for upcoming ‘24 cycle:

Need continued centrist bipartisan approach and knocking back of both L & R extremes to the far margins where they belong.

BLUENAMI..!!!!

Congrats on getting Substack Featured! Well deserved!!!